For investors looking to balance the search for growth with some caution, the "Growth at a Reasonable Price" (GARP) method offers a suitable middle path. This method tries to find companies that are increasing their earnings and revenue faster than average, but whose stock prices are not too high. The aim is to sidestep the high risk of paying too much for extreme growth while still joining a company's positive path. Filtering for stocks that show good growth numbers together with acceptable valuation, satisfactory profitability, and firm financial condition can help find these chances.

PACS Group Inc (NYSE:PACS) functions as a holding company that delivers post-acute healthcare services using a system of independently run skilled nursing and senior living facilities. With more than 300 facilities in 17 states, the company fills an important role in the healthcare system, looking after patients after they leave the hospital. As a fairly recent public company after its IPO in April 2024, PACS offers an interesting example for the affordable growth filter.

Growth Profile: A Main Positive

The main attraction of PACS within the GARP structure is its strong growth path, which gave it a ChartMill Growth Rating of 7 out of 10. The company is showing notable enlargement, a required condition for any growth-oriented method.

- Revenue Increase: PACS displays a very good increase in revenue, having risen by 29.32% over the last year. This speed is backed by a five-year average yearly revenue growth rate of almost 30%, showing a steady and sizable enlargement of its main business.

- Earnings Speed: Maybe more notably, the company's Earnings Per Share (EPS) increased by a very good 64.52% in the last year. This indicates the company is not only growing its revenue but is also changing that growth successfully into profit.

- Future Outlook: Experts think this positive pattern will carry on, with EPS predicted to grow by an average of 9.72% each year in the next few years. While the expected revenue growth rate is thought to slow, the continued earnings growth supports the investment idea.

This good growth profile is precisely what the affordable growth filter looks to find, as lasting enlargement is the force that can push future investor gains.

Valuation: Acceptable Even With Growth

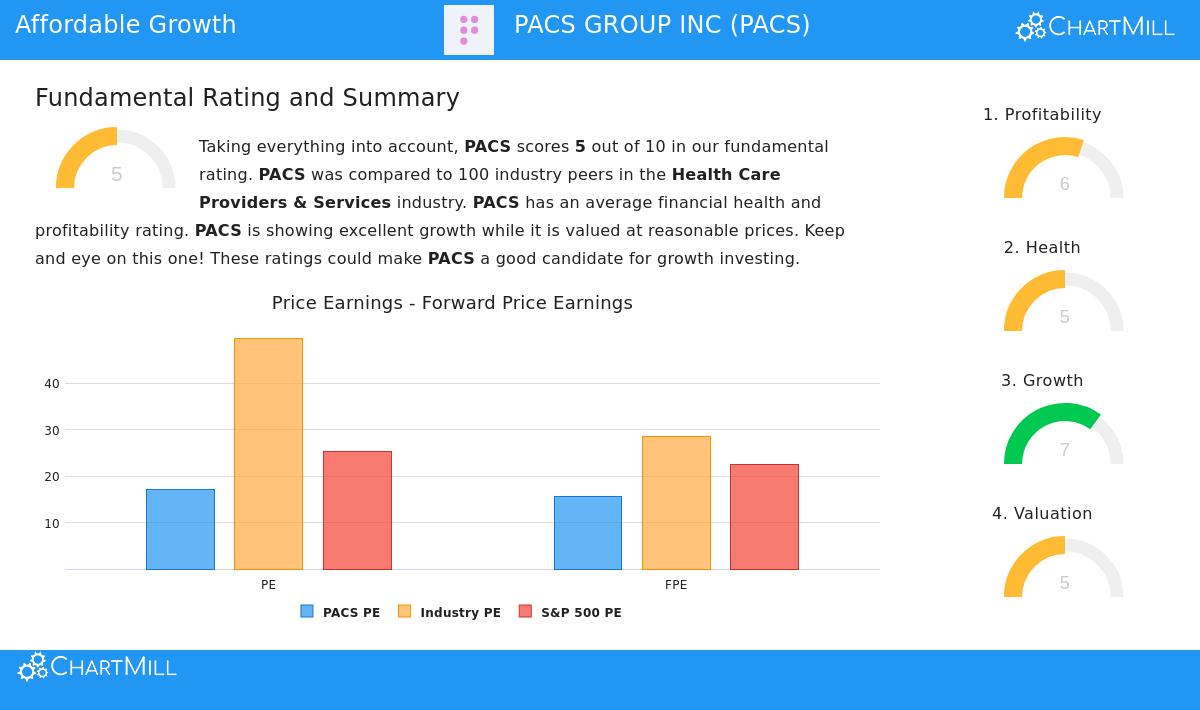

A main rule of the GARP method is making sure an investor is not paying too much for that growth. PACS's ChartMill Valuation Rating of 5 indicates a varied but mostly acceptable situation, which is the level the filter needs.

- Good Comparison Multiples: When measured against others in the Health Care Providers & Services field, PACS seems priced low. Its Price/Earnings (P/E) ratio of 17.11 costs less than 72% of field rivals, whose average P/E is about 50. In the same way, its forward P/E of 15.54 is better than 73% of the field.

- Wide Market Measurement: The valuation also looks acceptable next to the wider market. PACS sells for less than the S&P 500's current P/E of 25.23 and its forward P/E of 22.51.

- Growth Adjustment: The PEG ratio, which changes the P/E for expected growth, shows the stock is priced fairly. This is important for the method, as it means the market price suitably shows the company's growth possibilities without too much guesswork.

This acceptable valuation is the "affordable" part of the calculation, giving a buffer that pure speed growth stocks frequently do not have.

Supporting Basics: Profitability and Condition

For growth to be lasting, it must be based on a base of working efficiency and money steadiness. The affordable growth filter sorts for satisfactory scores here to reduce risk, and PACS meets this with a Profitability Rating of 6 and a Financial Health Rating of 5.

Profitability is satisfactory, with several good points:

- The company has a good Return on Equity of 20.23%, doing better than 88% of its field, which shows efficient use of investor money.

- Its profit margin of 3.62% and operating margin of 5.85% are in the better half of the field.

- A point to watch is that these margins have had some reduction in recent years, a part for investors to watch carefully.

Financial Health shows an even profile:

- The company displays high ability to pay debts, with a very good debt-to-free-cash-flow ratio of 1.69, meaning it could in theory pay all debt in under two years with its present cash flow.

- A workable Debt/Equity ratio of 0.50 suggests it is not too dependent on debt for money.

- Liquidity, as shown by the Current and Quick ratios near 1.07, is enough but not a main positive, putting it in the middle of its field.

These supporting ratings confirm that the company's growth is not being pushed by careless borrowing or happening even with bad operations, matching the filter's aim of finding balanced growth possibilities.

Conclusion

PACS Group Inc comes from the affordable growth filter as a suitable candidate that fits the GARP idea. It combines a clearly good growth force, especially in earnings, with a valuation that is acceptable both compared to its high-priced field and the wider market. While its profitability is firm and its financial health is satisfactory, investors should note the margin patterns and liquidity numbers. For those looking for contact with the necessary post-acute healthcare field through a company showing fast enlargement, PACS stands as a possible chance where the entry price does not seem to account for all future good results.

You can view the detailed fundamental analysis report for PACS Group Inc here.

To look at more stocks that match this "Affordable Growth" profile, you can run the filter yourself via this link: Find Affordable Growth Stocks.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer or request to buy or sell any securities. The information given is based on supplied data and should not be the only base for any investment choice. Investors should do their own review and talk with a qualified financial advisor before making any investment.