For investors looking to find possible opportunities in the market, a methodical process often includes searching for companies that seem fundamentally good but are priced low. One such tactic is the "Decent Value" screen, which tries to select stocks with a good valuation rating, indicating they might be priced below worth, while also holding acceptable scores in profitability, financial condition, and expansion. This process fits with central value investing ideas, where the aim is to discover good businesses selling for less than their true worth, offering a possible buffer for the patient investor.

Oshkosh Corp (NYSE:OSK) is an industrial maker of specialized vehicles and equipment, working in areas centered on access equipment, defense, and work vehicles. A recent review using the ChartMill fundamental report, which can be seen here, indicates the company shows a picture that could be notable for investors using this value-focused tactic.

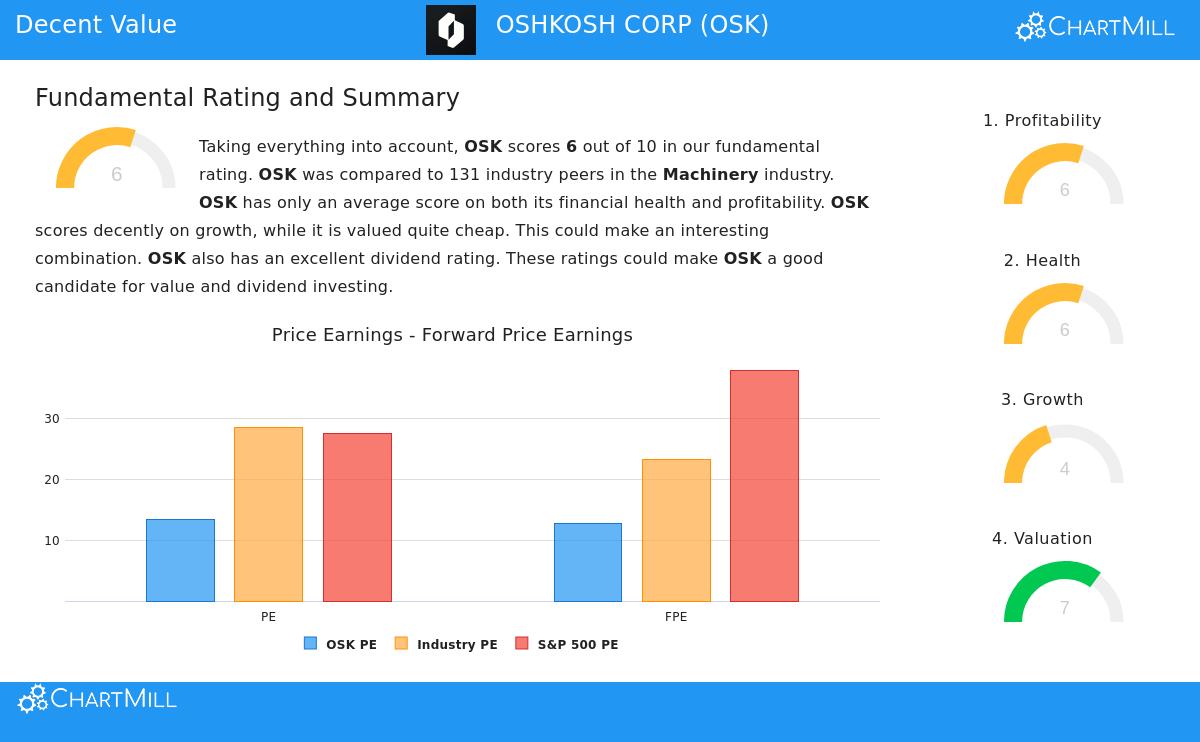

Valuation: The Central Part of the Idea

The main attraction of Oshkosh for a value screen is in its valuation numbers. The company's ChartMill Valuation Rating of 7 out of 10 signals it could be trading at a good price compared to its basics. This rating is backed by several important numbers that look good next to both its industry and the wider market.

- Price-to-Earnings (P/E) Ratio: At 13.33, OSK's P/E ratio is much lower than the S&P 500 average of 27.53. More notably, it is less expensive than about 92% of similar companies in the machinery industry.

- Forward P/E Ratio: The future-looking number of 12.68 shows a similar situation, being lower than over 92% of industry rivals and notably below the S&P 500 average.

- Enterprise Value to EBITDA & Price/Free Cash Flow: These other valuation measures support the point, with OSK trading at a lower cost than 94% and 85% of its industry, in turn, based on these calculations.

For a value investor, these numbers are important. They form the numerical beginning for spotting a possible difference between a company's market price and its true worth, which is the main idea of the tactic described at the start.

Financial Condition and Profitability: Reviewing the Base

A low-priced stock is only an interesting chance if the company is stable. Oshkosh's financial condition and profitability ratings, both at 6 out of 10, point to a steady, ordinary base, a main filter in the "Decent Value" screen to steer clear of "value traps."

- Financial Condition (Rating: 6): The company shows a strong balance sheet with a good Debt-to-Equity ratio of 0.24, doing better than 68% of its industry. Its Altman-Z score of 3.30 signals no short-term bankruptcy danger. A notable point is its good Debt to Free Cash Flow ratio of 1.93, meaning it could pay off all debt in less than two years from its cash flow, a number that is in the best 20% of its field.

- Profitability (Rating: 6): Oshkosh has been regularly profitable with positive earnings and operating cash flow over the last five years. Its Return on Equity (14.28%) and Return on Invested Capital (9.14%) are both in the best 30% of its industry, showing efficient use of shareholder money. While its gross margin is under the industry average, both its operating and profit margins have shown good movement in recent years.

These parts are necessary for the value tactic because they help confirm the company has the operational soundness and financial strength to handle market changes and finally achieve its possible worth.

Expansion and Dividend: Future Outlook and Shareholder Gains

While strict value choices may not show fast expansion, the screening rules need "acceptable" expansion to give a reason for future price increase. Oshkosh's Expansion Rating of 4 shows a varied but sensible view.

- The company has a good past record, with Revenue increasing at an average yearly rate of 8.73% and EPS at 16.91% over previous years.

- Recent results have slowed, with small drops in the last year's revenue and EPS, which moderates the rating.

- Looking ahead, analysts anticipate a return to expansion, with EPS forecast to rise by an average of 11.12% each year.

Also, Oshkosh has a very good Dividend Rating of 7. It has raised its dividend for at least ten straight years, with an average yearly growth rate of over 11%, and keeps a manageable payout ratio. For value investors, a dependable and increasing dividend can give income while waiting for the market to see the basic worth, improving total return possibility.

Conclusion

Oshkosh Corp shows an example of the kind of chance a structured "Decent Value" screen tries to reveal. It trades at valuation measures that are heavily reduced compared to the market and its industry, meeting the central value requirement. This lower price exists together with ordinary-to-good scores in financial condition and profitability, suggesting the low cost is not a sign of a failing business but possibly a market mistake. When joined with a dependable dividend and forecasts for renewed earnings expansion, the picture fits with a steady value investment method.

Investors curious about finding other companies that match similar standards of sound basics combined with good valuations can use the Decent Value Stocks screen to discover more possible selections.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or a bid to buy or sell any securities. The information shown is from supplied data and should not be the only ground for any investment choice. Investors should do their own review and talk with a qualified financial advisor before making any investment choices.