For investors using a classic value strategy, the goal is to find companies trading below their intrinsic worth. This involves a disciplined search for stocks with good underlying fundamentals, like healthy finances and consistent profitability, that are priced at a discount by the market. A "Decent Value" screen puts this into practice by filtering for companies with a high valuation rating, meaning they are inexpensive relative to their financials and peers, while also keeping acceptable scores in growth, financial health, and profitability. This method aims to avoid "value traps" by confirming the low price is connected to a fundamentally sound business. One stock currently meeting this screen is ON Semiconductor (NASDAQ:ON), a provider of intelligent power and sensing solutions.

Valuation: The Center of the Opportunity

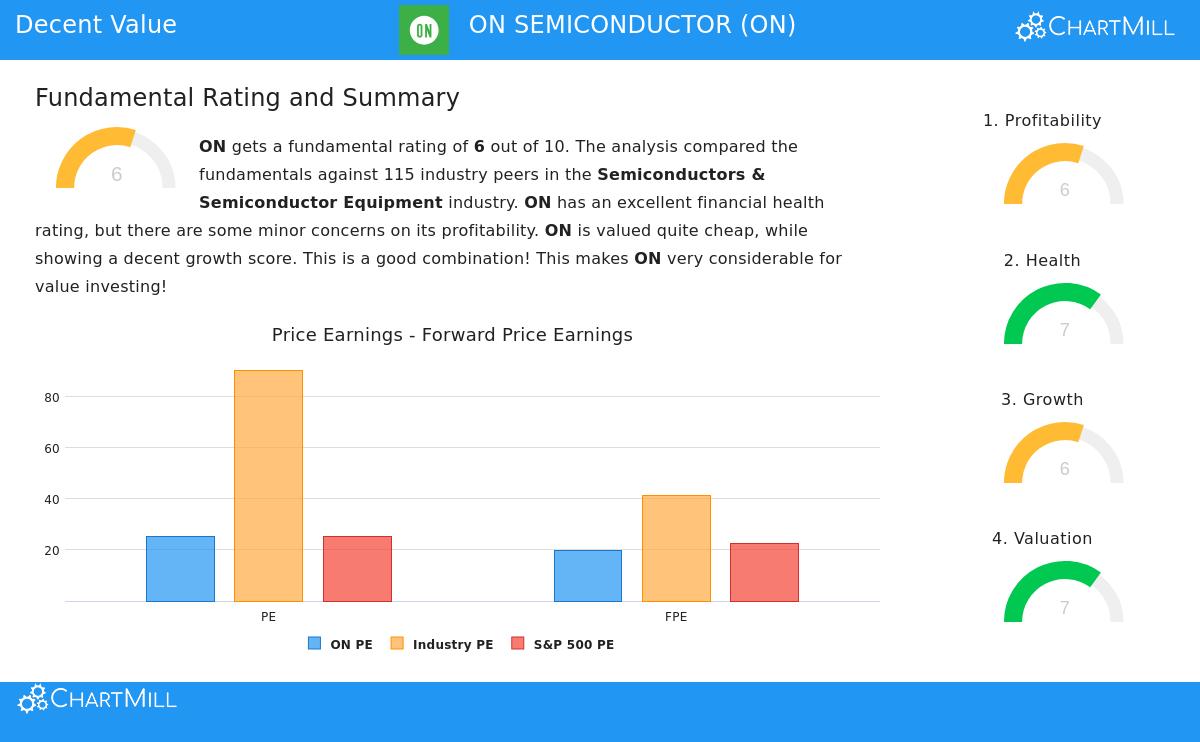

The main attraction for a value investor is a stock's price relative to its financial reality. ON Semiconductor's valuation metrics present a notable picture of possible undervaluation inside its high-performing sector.

- Attractive Multiples: While the company's standard Price-to-Earnings (P/E) ratio of 25.22 is in line with the broader S&P 500, it seems much less expensive within the Semiconductors & Semiconductor Equipment industry, where the average P/E is above 90. More revealing are other metrics: its Price-to-Free Cash Flow and Enterprise Value-to-EBITDA ratios are lower than about 94% and 84% of its industry peers, in order.

- Future Earnings Discount: The forward-looking Price/Forward Earnings ratio of 19.74 is also below the industry average of 41.37 and a bit under the S&P 500 average, indicating the market may not be fully accounting for expected future profits.

- Growth Compensation: The low PEG ratio, which modifies the P/E for growth, signals the stock's valuation could be especially interesting when its growth prospects are factored in. This is important for value investing, as it helps separate a truly inexpensive stock from one that is just low-growth.

For a value strategy, these metrics are the beginning. They imply the market might be setting too low a value on ON's cash generation and earnings power compared to its sector, creating the needed gap between market price and perceived intrinsic value.

Financial Health: A Solid Base

An inexpensive valuation is not meaningful if the company's balance sheet is weak. Value investing needs a margin of safety, and a financially healthy company supplies that. ON Semiconductor's financial health rating of 7 out of 10 indicates a solid base.

- Strong Liquidity: The company shows very good short-term financial flexibility, with a Current Ratio of 4.52 and a Quick Ratio of 2.98. These numbers, which are better than most industry peers, show ON has sufficient resources to meet its short-term obligations without difficulty.

- Manageable Solvency: ON has a moderate amount of debt, with a Debt-to-Equity ratio of 0.39. More significantly, its Debt-to-Free Cash Flow ratio of 2.12 is good, meaning it could pay off all its debt with just over two years of current cash flow. An Altman-Z score of 4.92 clearly puts the company outside the bankruptcy risk area.

- Capital Efficiency: While the report mentions a recent weakening in the debt-to-assets ratio, the overall solvency picture stays firm. This financial steadiness lowers the risk for value investors, making sure the company can withstand economic cycles and keep investing in its business.

Profitability and Growth: The Mechanism for Value Realization

A stock can be inexpensive and healthy but still be a value trap if it cannot grow profits. ON's mixed but encouraging ratings in profitability and growth are central to understanding its potential.

- Firm Operational Performance: ON receives a profitability rating of 6. Its Operating Margin of 12.53% is higher than 70% of its industry, and this margin has gotten better. However, its Gross Margin of 33.09% is on the lower end for the sector, and the overall Profit Margin is only average among peers. The company has been reliably profitable and cash-flow positive for years, a requirement for many value investors.

- Past Softness, Future Strength: The growth story is one of change. The past year has been difficult, with large drops in both Revenue (-15.35%) and Earnings Per Share (-40.95%). This recent softness is probably a main reason for its discounted valuation. However, the long-term view and future outlook are different.

- Increasing Growth Forecasts: Importantly, analysts predict a strong recovery. Earnings Per Share are expected to increase almost 30% each year in the coming years, with Revenue growth rising to nearly 10% per year. For a value investor, this predicted increase from a low point is the event that could narrow the gap between the current market price and the company's higher intrinsic value.

Conclusion and Further Research

ON Semiconductor presents a case that fits core value investing principles: it trades at a discount to its industry based on cash flow and forward earnings, has a strong balance sheet that gives a margin of safety, and is predicted to return to solid growth after a cyclical slowdown. The mix of a high valuation rating (7) with acceptable scores in health (7), profitability (6), and growth (6) makes it a candidate deserving of more detailed examination for value-focused portfolios.

The recent decline in financial metrics must be studied closely to decide if it is a temporary industry cycle or a more basic problem. Still, the predicted growth recovery and the company's strategic place in automotive and industrial markets suggest a reasonable path for value to be recognized.

Interested in examining other stocks that match a similar "Decent Value" profile? You can run the screen yourself using our predefined Decent Value Stocks screener to find more possible opportunities.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data and ratings provided by ChartMill. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.