Natural Grocers by Vitamin C (NYSE:NGVC) isn’t exactly a household name on Wall Street, but that’s often where the best opportunities hide. Running a stock screen based on the Peter Lynch strategy—a classic approach for long-term, growth-at-a-reasonable-price (GARP) investors—can help uncover companies that combine sustainable earnings growth with solid valuation and healthy finances. The core idea is to find businesses you can understand, that are expanding steadily but not at a breakneck pace, and that trade at a price which hasn’t gotten ahead of themselves.

The Peter Lynch method avoids speculative high-fliers and instead focuses on companies with an earnings-per-share (EPS) growth rate between 15% and 30% annually. Natural Grocers fits this bill nicely: over the last five years, its EPS has grown by an average of 17.84% per year—comfortably within that sweet spot. Lynch argued that growth above 30% is often unsustainable, while companies growing too slowly may not generate the returns long-term investors need. NGVC’s pace suggests a disciplined expansion tied to its core natural and organic grocery business, not a one-time surge.

Valuation is the other half of the GARP equation. Using Lynch’s preferred metric, the PEG ratio (price/earnings divided by growth), the ideal is a value of 1.0 or lower. For Natural Grocers, the 5-year PEG ratio comes in at 0.75—well below that threshold. This means the stock’s current price of 13.30 times earnings is more than justified by its historical growth rate. In other words, investors aren’t overpaying for the expansion that’s already in motion. Compared to the S&P 500’s average P/E of 27.4, that’s a significant discount.

Financial health is a cornerstone of Lynch’s strategy, since debt-laden companies can sink even good growth stories. Natural Grocers passes these tests with room to spare. Its return on equity (ROE) stands at 21.74%, well above the 15% minimum Lynch demanded—signaling efficient use of shareholder capital. Debt-to-equity ratio is a conservative 0.20 (the screen’s filter is 0.6 or less), meaning the company relies more on equity than borrowed money, which reduces risk in downturns. The current ratio is 1.07, just clearing the 1.0 hurdle, indicating adequate short-term liquidity.

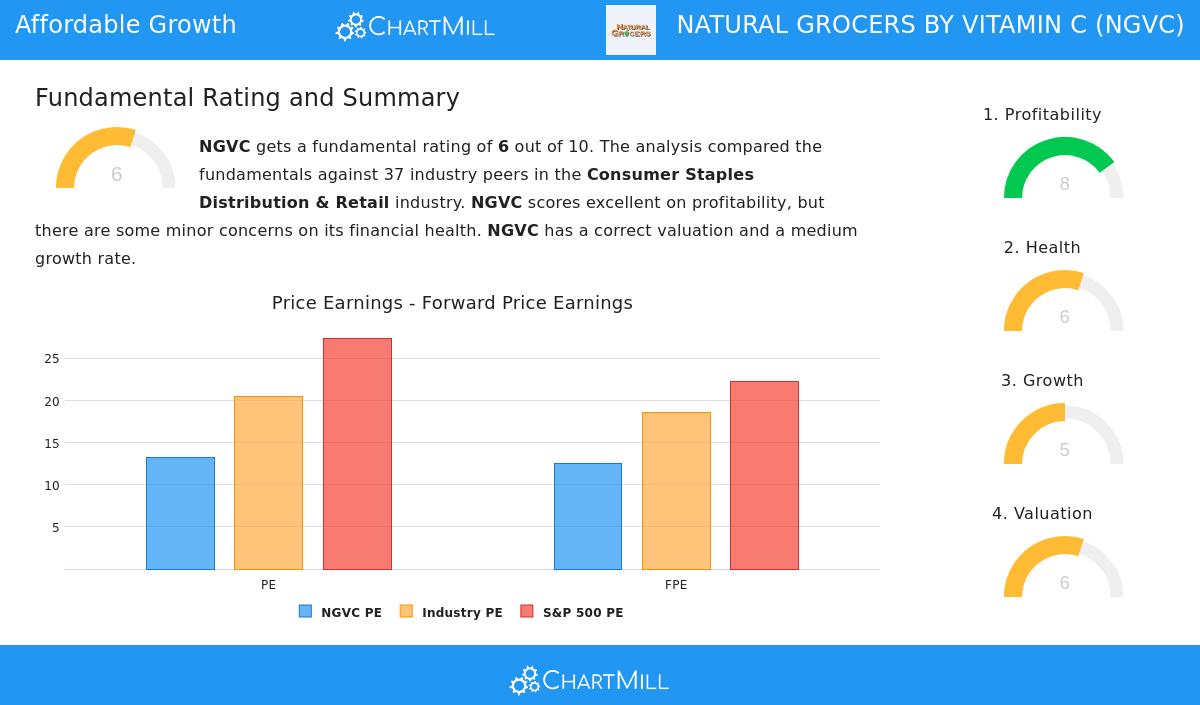

Looking at the broader fundamental report, Natural Grocers earns a rating of 6 out of 10 from its peer group in the Consumer Staples Distribution & Retail industry. While that may not sound spectacular, the score reflects a mixed but solid profile: strong profitability (8/10) with a profit margin of 3.58%, an operating margin of 4.74%, and a dividend yield of 2.19% that’s higher than 86% of its industry peers. Its health score is decent (6/10), driven by an Altman-Z score of 3.50, which signals low bankruptcy risk, and a low debt-to-free-cash-flow ratio of 1.12. The valuation score is also 6/10, but the P/E of 13.30 is cheaper than 84% of its industry rivals—a strong point for value-conscious GARP investors. For a deeper look at the numbers, you can check the full fundamental analysis report.

Finally, it’s worth noting that NGVC’s 168 stores across 21 states have grown revenue at a steady 5.12% annually, while its EPS growth has outpaced that through operational improvements. The company also pays a dividend yielding 2.19%—a rare bonus for a GARP candidate—which has grown at an average of 11.4% per year. While some metrics like the quick ratio and recent share dilution raise caution flags, the core Lynch criteria suggest a business that is profitable, reasonably priced, and growing at a sustainable rate.

If you’re looking for more stocks that pass the Peter Lynch screen—combining 5-year EPS growth between 15% and 30%, PEG under 1.0, ROE above 15%, and low debt—you can run the same screen here to see additional candidates for your own research.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own due diligence before making any investment decisions.