For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method presents a solid middle path. This method tries to find companies that are increasing their earnings and revenue faster than average, but whose shares are not valued at the high levels seen with more speculative growth stocks. By concentrating on firms with good basic foundations, like strong profit generation and a sound financial position, the method works to reduce risk while still gaining from corporate growth. One instrument for applying this is an "Affordable Growth" stock filter, which selects for companies with high growth ratings, good profit and financial strength scores, and a valuation that is not extreme.

NETFLIX INC (NASDAQ:NFLX) recently appeared from such a filter, offering an example of how a leading company in a contested field can match GARP ideas. The streaming company's basic report, available here, shows a varied but finally solid view.

Growth Path: A Main Strength

The base of any GARP choice is strong growth, and Netflix performs well in this group, receiving a ChartMill Growth Rating of 7 out of 10. The company shows a potent mix of past results and predicted future growth.

- Past Results: Over the last year, Netflix increased its Earnings Per Share (EPS) by a notable 27.43%, with a five-year average yearly EPS growth rate of almost 33%. Revenue has also grown well, up 15.85% last year.

- Future Predictions: Analysts forecast this progress to keep going, with estimated yearly EPS growth of 18.40% and revenue growth of 10.43% in the next years. While future EPS growth is predicted to slow from its unusual historical speed, it stays firmly in "quite strong" range, giving a stable-looking growth path.

This steady top- and bottom-line growth is important for the affordable growth idea, as it supplies the basic earnings ability that can support and possibly grow into the present stock valuation.

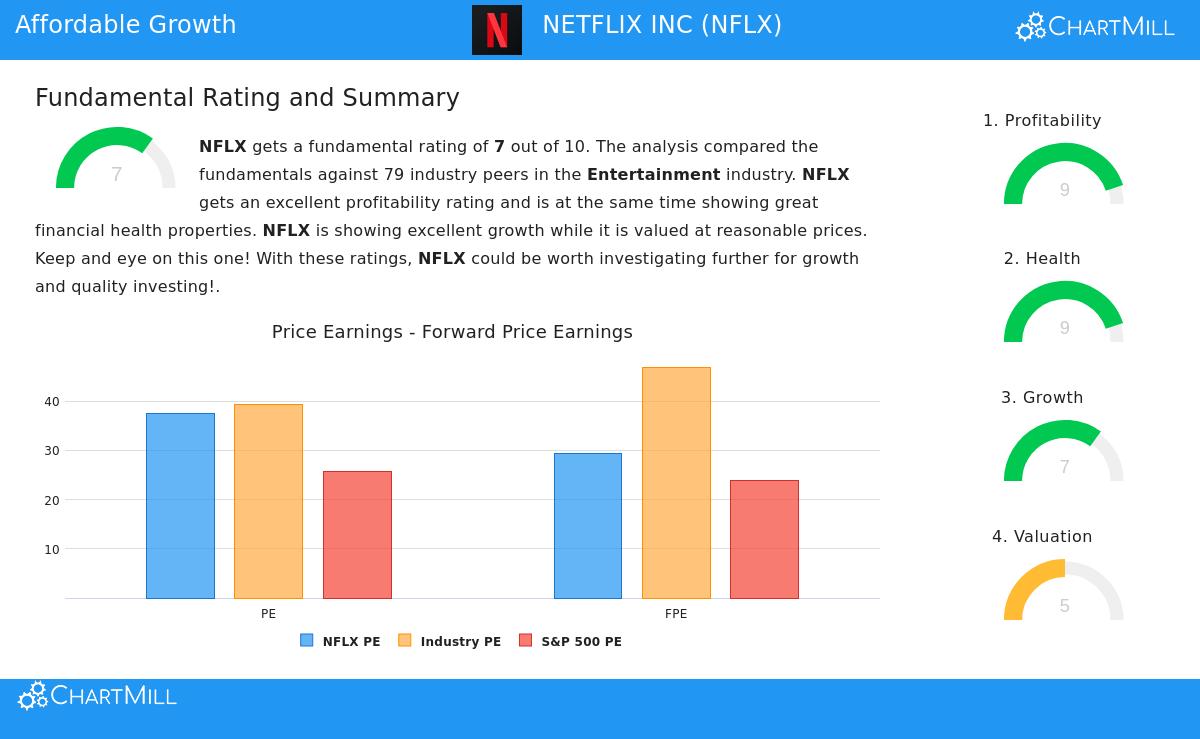

Valuation: The "Reasonable Price" Point

Valuation is where the "affordable" or "reasonable" part is examined. Netflix gets a neutral ChartMill Valuation Rating of 5. The view is detailed, showing a higher price for higher-quality results.

- Standard Measures: Based on a Price/Earnings (P/E) ratio of 37.4, Netflix seems costly, both compared to the S&P 500 average (25.8) and its own forward P/E of 29.4.

- Relative and Growth-Considered View: Yet, setting is important. About 78% of its entertainment industry group trades at a higher P/E ratio. More significantly, measures that include growth and cash flow give a different account. The PEG ratio, which changes the P/E for growth, points to a fair valuation. Also, the company's Enterprise Value/EBITDA and Price/Free Cash Flow ratios are more positive, placing it as less expensive than about 70-76% of its industry group.

For a GARP investor, this valuation review is central. While not "low-cost" in a pure sense, the valuation can be seen as reasonable when considered next to the company's unusual profit generation, industry place, and growth outlook. The filter's need for a valuation score above 5 works to sort out the most extremely high-priced names, which Netflix does not meet.

Supporting Basics: Profit Generation and Financial Strength

A main risk-reducing part of the GARP method is making sure that growth is set on a steady base. Netflix does very well here, having top-level ChartMill ratings of 9 for both Profit Generation and Financial Strength. These high scores give trust that the company's growth is high-quality and lasting.

- Unusual Profit Generation: The company's margins and returns on capital are excellent. With a Return on Invested Capital (ROIC) of 25.95%, Netflix does better than nearly 99% of its industry. Its operating margin of 29.5% is also with the best in the field. High profit generation supports a higher earnings multiple and suggests the company has a lasting competitive edge.

- Very Strong Financial Strength: An Altman-Z score of almost 11 shows almost no bankruptcy danger and puts Netflix in the top group of its industry for financial security. While its debt-to-equity ratio is average, its ability to create free cash flow is solid, with a low Debt-to-Free-Cash-Flow ratio of 1.5 years. This sound financial situation gives good room to handle competition, put money into new content and projects, and give capital back to shareholders through buybacks.

These supports of profit generation and strength are essential for a careful growth method. They make sure the company can pay for its own growth, manage economic drops, and avoid the problems of growth that is driven by too much debt or poor use of capital.

Conclusion

Netflix offers a standard GARP outline: a company with a shown and predicted solid growth path, trading at a valuation that, while not small, is reasonable compared to its quality, industry position, and future outlook. Its top-class profit generation and very strong balance sheet greatly lower the risk in the investment case, setting it apart from more speculative growth accounts. For investors searching for affordable growth, NFLX stands as a choice where high-quality basics help support a higher price.

Interested in reviewing other stocks that match this "Affordable Growth" outline? You can use the same filter applied to find Netflix to locate more possible choices. Click here to view the filter and see more results.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or a bid or request to buy or sell any securities. The review is based on data and ratings given by ChartMill, and investors should do their own study and talk with a qualified financial advisor before making any investment choices.