The investment philosophy of Peter Lynch, the famous manager of Fidelity's Magellan Fund, focuses on locating well-run, expanding companies that are available at sensible prices. His method, often called Growth at a Reasonable Price (GARP), highlights lasting business models instead of speculative trends. Lynch supported putting money into companies that are easy to understand, with good basics, profitability, sound finances, and controlled debt, that could be kept for many years. A primary instrument for locating these possibilities is a stock screener using his particular rules, which sorts for companies showing controlled expansion, good prices, and firm financial condition.

One company that recently appeared from a Peter Lynch-influenced screen is Mueller Water Products Inc-A (NYSE:MWA). The company makes many products for water movement, delivery, and measurement, working through its Water Flow Solutions and Water Management Solutions divisions. Its collection includes necessary infrastructure parts like valves, fire hydrants, and leak detection systems. This business, while not exciting, matches Lynch's liking for understandable companies in stable, necessary fields.

Alignment with Peter Lynch Criteria

The screen uses several number-based filters taken from Lynch's ideas. Mueller Water Products seems to satisfy these central needs, which are made to find companies with lasting expansion and a price buffer.

- Lasting Earnings Expansion: Lynch looked for companies increasing earnings per share (EPS) between 15% and 30% each year over five years, thinking expansion outside this area was often not lasting. MWA states a five-year EPS expansion rate of 20.76%, putting it directly within this goal area. This shows a record of steady, better-than-average profit growth.

- Sensible Price via PEG Ratio: To prevent paying too much for expansion, Lynch used the Price/Earnings to Growth (PEG) ratio, choosing a value of 1 or lower. MWA's PEG ratio, using its past five-year expansion, is about 0.99. This indicates the stock's price is mostly supported by its historical earnings expansion, a sign of the GARP method.

- Firm Profitability (ROE): A lowest Return on Equity (ROE) of 15% was a Lynch standard for judging management's skill in creating profits from owner money. MWA's ROE of 19.60% is well above this line, showing firm and good profitability.

- Good Financial Condition: Lynch highlighted a firm balance sheet. Two main filters are:

- Debt/Equity < 0.6: MWA's Debt/Equity ratio of 0.44 shows it is funded more by owner money than debt, giving it stability in weak economic times. Lynch liked even lower ratios, but this amount is still seen as good and careful.

- Current Ratio >= 1: This checks a company's ability to meet near-term bills. MWA's very high Current Ratio of 4.02 shows large cash availability and a very firm near-term financial state.

Basic Condition Review

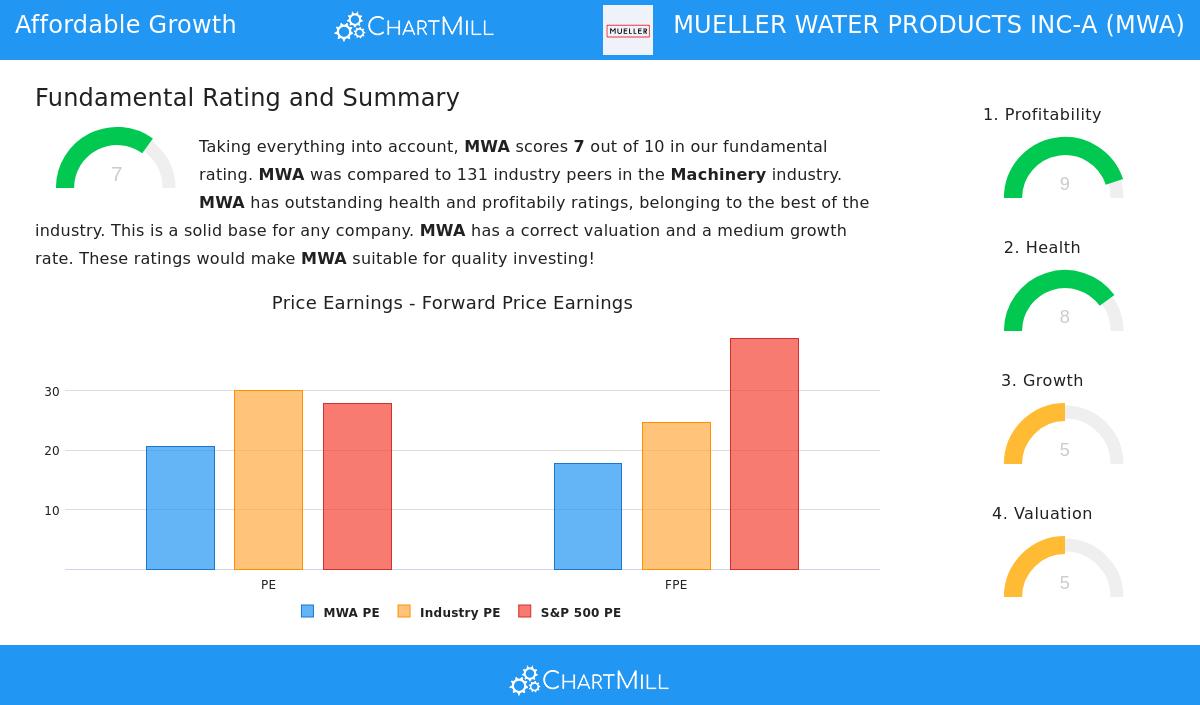

A wider basic review of Mueller Water Products supports the image shown by the Lynch screen. The company gets a firm total basic rating of 7 out of 10, with specific strong points in profitability and financial condition.

Profitability is a high point, with a rating of 9/10. The company has very good margins and returns, including an Operating Margin of 19.70% and an ROE of 19.60%, which place it with the best in its machinery industry group. Its Return on Invested Capital (ROIC) of 13.08% also shows good use of money.

Financial Condition gets a firm 8/10. The high Current and Quick ratios confirm better cash availability, while a workable Debt/Equity ratio and a good Altman-Z score of 4.84 point to a very steady balance sheet with little failure risk.

The Price image is mixed, scoring 5/10. While its P/E ratio of 20.59 is seen as high compared to its own history, it costs less than both the S&P 500 average and most of its industry group. The main worry noted is a high PEG ratio when using future expansion guesses, suggesting the market may be setting a price for slower expansion coming.

On Expansion, the company scores 5/10. Its past results are firm, with strong historical EPS expansion. However, experts predict a notable slowing in both sales and earnings expansion for the next few years. This future slowing is a key point for investors to study more, as it differs from the excellent historical expansion that first made it fit for the Lynch screen.

You can see the full basic review for Mueller Water Products here.

Is MWA a Lynch-Method Investment?

Mueller Water Products makes a strong case for investors following Peter Lynch's GARP philosophy. It works in the necessary, steady water infrastructure field, a "simple" business Lynch might like. Its historical numbers match almost exactly with the number-based rules of his plan: lasting past EPS expansion, a sensible PEG ratio, high profitability, and a very firm balance sheet. These things suggest a good company made for long-term keeping.

The main question for a possible investor, as Lynch would suggest, needs looking past the screen. The central matter is if the expected slowing in future expansion is a short-term stage or a new long-term fact. Investors must study the company's competitive place, market chances, and management's plan to decide if it can keep a higher expansion rate than now predicted. If it can, the current price may look good.

For investors wanting to look at other companies that pass similar controlled expansion and price filters, the Peter Lynch plan screen can be found here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any securities. The review uses given data and certain investment methods. Investors should do their own full study and think about their personal money situation before making any investment choices.