In the search for long-term investment opportunities, many investors turn to strategies that blend the pursuit of growth with a disciplined focus on valuation. One of the most celebrated approaches is that of Peter Lynch, the legendary manager of the Fidelity Magellan Fund. His philosophy, often categorized as Growth at a Reasonable Price (GARP), centers on identifying companies with strong, sustainable earnings growth that are not overvalued by the market. It is a method that prioritizes fundamental health, profitability, and a sensible price tag over speculative momentum. A screen based on Lynch's core criteria recently highlighted Mueller Water Products Inc-A (NYSE:MWA) as a potential candidate worthy of further research for investors aligned with this strategy.

Meeting the Lynch Criteria

Lynch's framework is built on several key financial filters designed to separate strong, growing businesses from the rest. Mueller Water Products appears to meet these critical benchmarks, which are foundational to the GARP approach.

- Sustainable Earnings Growth: Lynch sought companies with a consistent track record of growth, but he was wary of hyper-growth that could not be maintained. The screen requires a 5-year earnings per share (EPS) growth rate between 15% and 30%. MWA's EPS has grown at an average annual rate of 20.76% over the past five years, placing it firmly within this desirable range. This indicates a history of solid expansion without crossing into unsustainable territory.

- Reasonable Valuation (PEG Ratio): Perhaps the cornerstone of Lynch's strategy is the Price/Earnings to Growth (PEG) ratio, which adjusts the common P/E ratio for a company's growth rate. A PEG ratio of 1 or less suggests the stock may be reasonably priced relative to its growth trajectory. MWA's PEG ratio, based on its past five-year growth, is 0.96. This is a crucial metric for GARP investors, as it directly links what you pay to the growth you receive, and a figure below 1 often signals an attractive valuation opportunity.

- Strong Profitability (Return on Equity): Lynch favored companies that efficiently generate profits from shareholder equity. A minimum Return on Equity (ROE) of 15% was his benchmark. MWA's ROE stands at a solid 19.60%, suggesting the company is highly effective at converting its equity base into earnings. This is a sign of a well-managed business with a durable competitive advantage, a key trait for long-term holdings.

- Financial Health (Debt and Liquidity): To ensure resilience, Lynch emphasized strong balance sheets. His rules include a Debt-to-Equity ratio below 0.6 (with a personal preference for under 0.25) and a Current Ratio of at least 1. MWA exhibits conservative leverage with a Debt-to-Equity ratio of 0.44 and exceptional short-term liquidity with a Current Ratio of 4.02. These metrics indicate a company with ample financial flexibility to weather economic downturns and invest in future growth without over-reliance on debt.

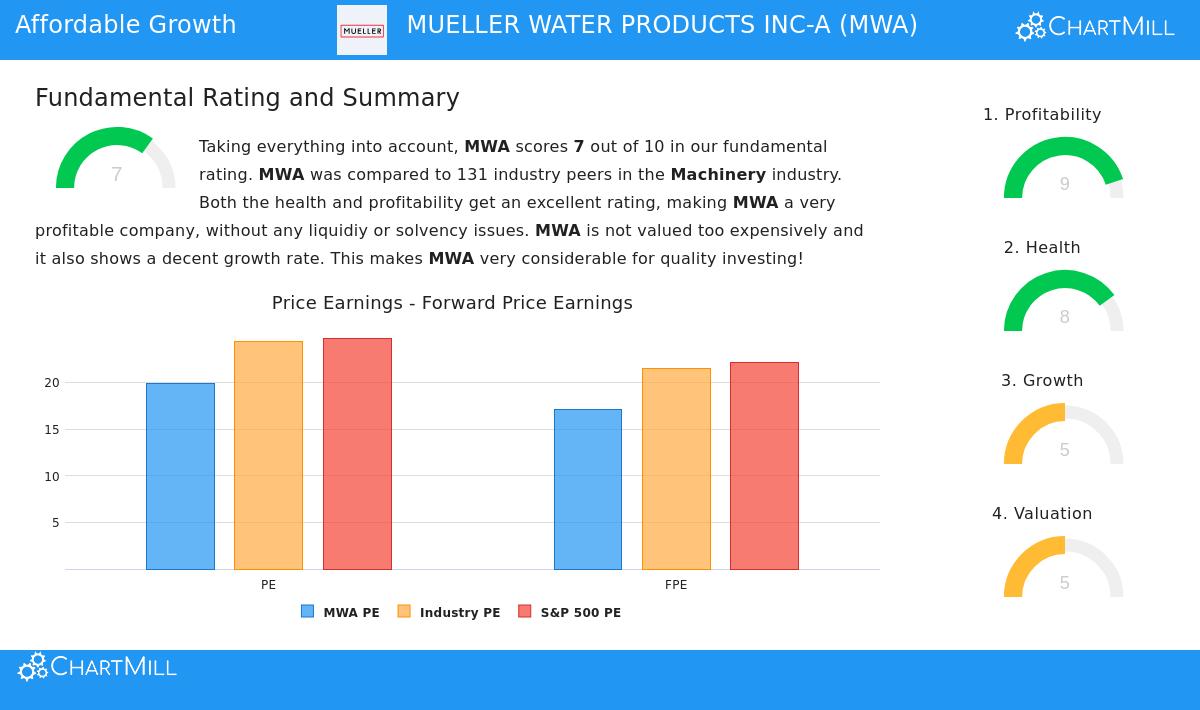

A High-Level Fundamental View

A broader look at Mueller Water Products' fundamental profile reinforces the picture painted by the Lynch screen. The company, which manufactures essential products for water transmission and distribution, earns a strong overall fundamental rating. Its profitability is rated as excellent, with industry-leading margins and returns on assets and invested capital. Financial health is also a standout, with top-tier liquidity ratios and a firm solvency position, including a healthy Altman-Z score that suggests a very low risk of financial distress.

While the company's valuation on a standard P/E basis may appear fair to slightly expensive compared to the broader market, the critical PEG ratio, which Lynch relied upon, tells a more nuanced story by factoring in its above-average growth. Analysts project a moderation in growth rates going forward, which is typical as companies mature, but the established track record of profitability and financial strength provides a stable foundation. You can explore the full, detailed fundamental analysis for MWA here.

Conclusion

For investors guided by the principles of Peter Lynch, Mueller Water Products presents an interesting case study. It demonstrates the characteristics he prized: a history of reliable, double-digit earnings growth, a valuation that appears reasonable when that growth is accounted for, high profitability, and a firm balance sheet. The company operates in the essential, if unglamorous, water infrastructure sector, exactly the type of "dull" business Lynch believed could offer outstanding opportunities. It serves as a clear example of how a disciplined screening process can find potential GARP candidates that warrant deeper due diligence.

The Peter Lynch strategy screen is designed to identify such companies systematically. If you are interested in exploring other stocks that currently pass this set of growth, value, and health filters, you can view the live screen results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.