In the search for investment chances, many investors use the ideas of value investing, a method created by Benjamin Graham and famously used by Warren Buffett. Its foundation is finding companies whose stock price is lower than their calculated real worth. The aim is to find good businesses that the market has incorrectly priced for now, giving a possible "margin of safety" for the investor. One organized way to use this thinking is by looking for stocks that show good fundamental condition and earnings, but are selling at good prices. This method tries to steer clear of "value traps," cheap stocks of failing businesses, by making sure the company is financially stable.

A recent search using this method has pointed to Pediatrix Medical Group Inc. (NYSE:MD) as a possible choice. The company, a national provider of physician services focused on newborn, maternal-fetal, and pediatric critical care, seems to join acceptable business soundness with a very low stock price compared to its earnings and cash flow.

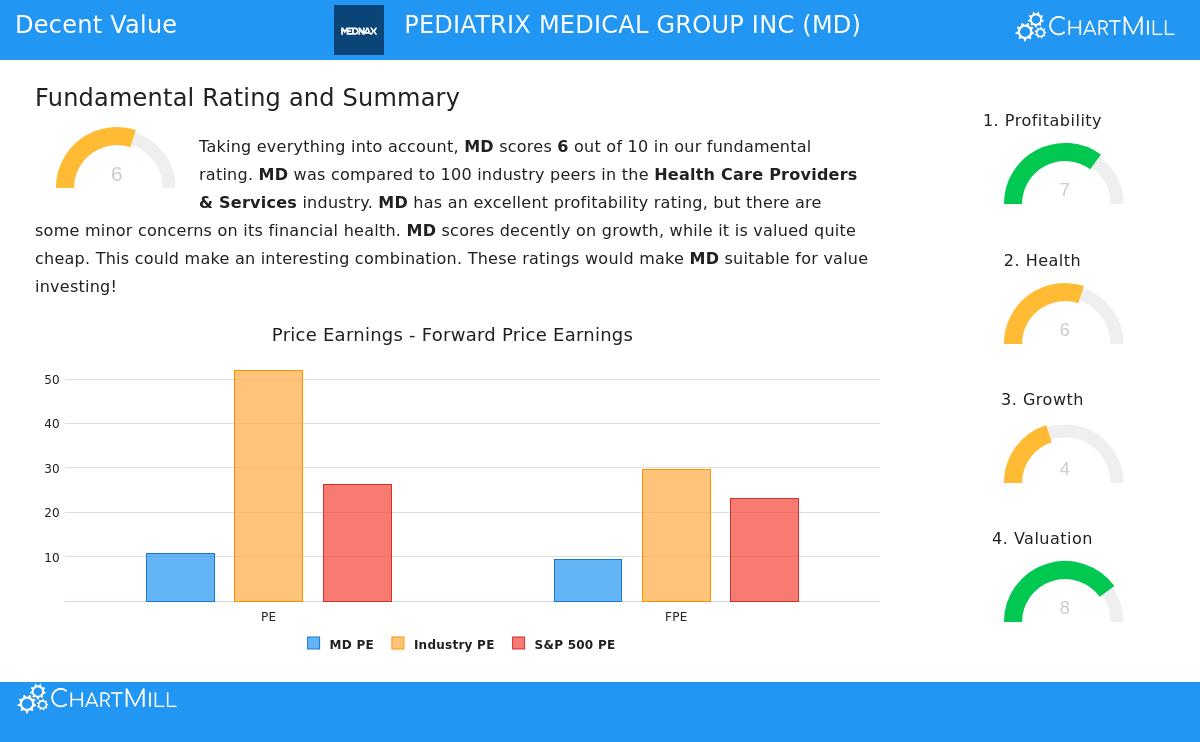

A Closer Look at Valuation

The most interesting part of Pediatrix is its price, which gets an 8 out of 10 in ChartMill's fundamental study. The numbers indicate the stock is priced low, particularly inside its field.

- Price-to-Earnings (P/E) Ratio: At 10.71, MD's P/E ratio is much lower than both the field average of 52.04 and the S&P 500's average of 26.21. This makes it less expensive than 92% of similar companies in the Health Care Providers & Services field.

- Forward P/E Ratio: The future-looking number is even better at 9.45, showing analysts think earnings will continue. This is less expensive than 93% of field rivals.

- Cash Flow and EBITDA Multiples: The stock also seems low-priced based on cash creation. Its Price/Free Cash Flow and Enterprise Value/EBITDA ratios are lower than 90% and 87% of field peers, in that order.

For a value investor, these numbers are the beginning. A low price compared to earnings and cash flow suggests the market might be setting too low a value on the company's consistent earnings, possibly giving that important margin of safety.

Checking Financial Condition and Earnings

A low-priced stock is only a sound investment if the company is steady. This is where Pediatrix's fair scores in financial condition (6/10) and good earnings (7/10) become important, speaking to a main idea of value investing: steering clear of value traps.

The company's earnings numbers are a specific positive point:

- It has a good Return on Equity (ROE) of 19.10% and a sound Return on Invested Capital (ROIC) of 9.88%, both doing better than most of its field.

- Its Profit Margin of 8.64% and Operating Margin of 12.07% are not only good but have gotten better in recent years, showing capable management.

Financially, the company seems on firm footing. Its Debt-to-Free Cash Flow ratio of 2.36 is sound, suggesting it could pay its debt in a little more than two years from its cash flow, a sign of acceptable solvency. While its Altman-Z score and Debt/Equity ratio are average for the field, the acceptable cash flow coverage of debt lessens worry. This general financial steadiness gives trust that the business is not in trouble, supporting the thought that its low price might be a chance instead of a warning.

Growth Points

Growth is often the absent part in a standard value story. Pediatrix's growth score is a more average 4/10, which helps explain its low price. The past year had a small drop in income, though the long-term average is still positive. More positively, Earnings Per Share (EPS) increased by over 36% in the last year and has a sound 10% average yearly growth rate over recent years.

Looking forward, analyst predictions are for slow but steady growth in both income and EPS. For a value investor, this picture can be fine. The method does not always look for fast growth; it looks for a sound business at a very good price. Pediatrix's shown earnings and financial condition, joined with its very low earnings multiple, suggest the market might be too negative about its future, pricing it as if no growth will happen.

Conclusion: A Value Case in Healthcare

Pediatrix Medical Group shows an example in used value searching. It is not a fast-rising growth stock, but a settled participant in the necessary healthcare services field selling at a large discount to the market and its own field. Its good earnings and acceptable financial condition point to operational quality, while its low price numbers give the possible downside protection value investors look for. The average growth predictions are likely already included in its single-digit P/E ratio, leaving space for gain if the company just keeps its present path.

Interested in finding more stocks that match this "acceptable value" description? You can use the same search used to find Pediatrix and find other possible chances here.

For a complete look at all the fundamental parts behind these scores, you can see the full ChartMill Fundamental Analysis Report for MD.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of principal. Always do your own study and think about your financial position and risk tolerance before making any investment choices.