The search for quality companies that mix steady growth with an acceptable price is a foundation of many long-term investment methods. One highly regarded method is the strategy made famous by Peter Lynch, the noted manager of the Fidelity Magellan Fund. Lynch supported a "growth at a reasonable price" (GARP) style, concentrating on financially sound businesses with lasting, but not extreme, earnings growth that sell at prices which do not overvalue that future possibility. His method uses particular filters to find these companies, stressing a solid balance sheet, high profitability, and an attractive valuation when growth is considered.

A recent filter based on Lynch's main ideas has identified Lululemon Athletica Inc (NASDAQ:LULU) as a candidate for more examination by long-term investors. The apparel retailer seems to match several important parts of the GARP method, offering a case study in how Lynch's filters can find companies with positive fundamental traits.

Alignment with Peter Lynch Criteria

The Lynch filter uses several number-based tests to judge a company's health, profitability, growth, and value. Lululemon's present situation shows a good match across these measures:

- Sustainable Earnings Growth: Lynch preferred companies with a confirmed history of growth, but was cautious of rates that were too high. The filter seeks a 5-year earnings per share (EPS) growth rate between 15% and 30%. Lululemon's EPS has increased at a notable average yearly rate of 23.4% over this time, fitting within Lynch's desired range and showing a solid, yet possibly continued, growth path.

- Acceptable Valuation (PEG Ratio): Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to price a stock compared to its growth rate. A PEG ratio of 1 or less is seen as positive, implying the market is not overvaluing future earnings increase. With a PEG ratio of 0.54, Lululemon sells at a marked discount to its historical growth, a key part of the "reasonable price" element of GARP investing.

- Financial Health and Low Debt: Lynch valued companies with solid balance sheets to endure economic declines. The filter demands a Debt/Equity ratio below 0.6, with Lynch himself favoring a ratio under 0.25. Lululemon does very well here, reporting no outstanding debt (a Debt/Equity ratio of 0.0), putting it in a very strong financial state with little solvency danger.

- Solid Profitability (Return on Equity): Reliable high returns on shareholder equity indicate an efficient and well-run business. The filter requires a Return on Equity (ROE) above 15%. Lululemon greatly surpasses this, having an ROE of 31.8%, which shows it is producing significant profits from the capital provided by its shareholders.

- Short-Term Liquidity: To confirm a company can meet its immediate responsibilities, the filter looks for a Current Ratio (current assets divided by current liabilities) of at least 1. Lululemon's ratio of 2.26 indicates sufficient liquidity and a solid capacity to handle short-term debts.

Fundamental Health Check: A High-Level Summary

A wider fundamental review of Lululemon supports the image shown by the Lynch filter. The company gets high scores for its financial strength and operational quality.

- Profitability is a clear strong point, with top-level margins and returns on assets, equity, and invested capital. The company has been reliably profitable with positive cash flow for years.

- Financial health is very good. The lack of debt, a high Altman-Z score showing low bankruptcy danger, and a strong current ratio together point to a very secure balance sheet.

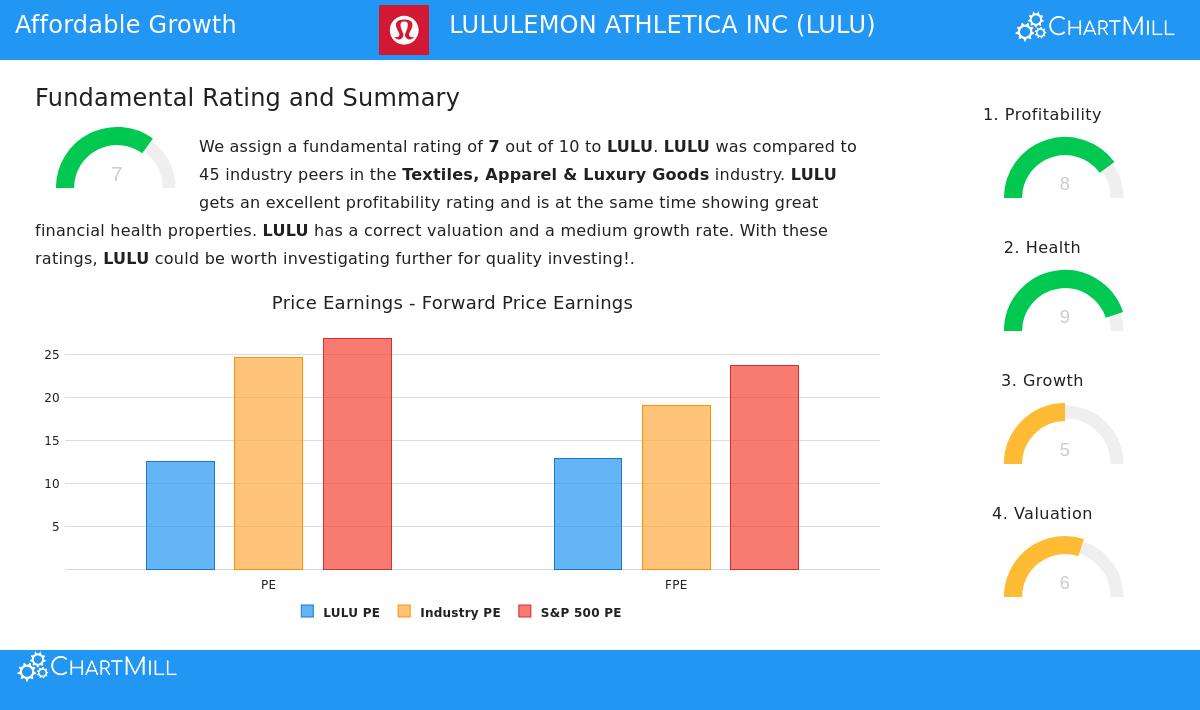

- Valuation seems acceptable, particularly in context. While its basic P/E ratio is neutral compared to its own history, it is less expensive than most of its competitors in the apparel and luxury goods industry and sells at a clear discount to the wider S&P 500 index. This, along with its high growth and profitability, supports the attractive PEG ratio.

- Growth presents a detailed story. The last five years have seen very strong revenue and EPS growth. However, recent periods show a slowdown, with a small decrease in EPS last year and forecasts for future growth to be good but at a more controlled speed than the high rates of the past. This shift is something Lynch would probably see as a move toward more lasting, long-term growth.

For a complete look at these fundamental ratings, you can see the full Lululemon Athletica Inc Fundamental Analysis Report.

Investor Considerations

For the long-term GARP investor, Lululemon offers an attractive profile: a leading brand in its field with a past of high growth, excellent profitability, and a very strong balance sheet, all available at a price that seems to allow for a more settled growth stage. The company’s match with Peter Lynch’s structured criteria suggests it has the fundamental attributes he wanted for a long-term investment. Investors should, as Lynch always recommended, do their own study to learn the business drivers, competitive environment, and possible risks to make sure it belongs in a varied portfolio.

Interested in finding other companies that pass the Peter Lynch filter? You can run the filter yourself and see the complete list of results here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data and a specific investment strategy model, past performance is not indicative of future results. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.