The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, focuses on finding high-quality growth companies trading at reasonable prices. Often described as a Growth at a Reasonable Price (GARP) method, Lynch’s strategy looks for businesses with strong, sustainable earnings growth, excellent profitability, a sound financial foundation, and a valuation that does not overpay for that future potential. It is a disciplined system for long-term investors aiming to build a diversified collection of companies that can increase wealth over decades.

A recent filter based on Lynch's main criteria has identified Lululemon Athletica Inc. (NASDAQ:LULU) as a possible candidate. The athletic apparel retailer seems to match several important parts of the strategy, making a case for more examination by investors focused on lasting growth.

Match with Peter Lynch's Main Criteria

Lynch’s filter stresses a balance between growth, value, and financial soundness. Lululemon’s present measurements show a good fit in these areas.

- Sustainable Earnings Growth: Lynch preferred companies with steady, but not extreme, earnings growth, usually between 15% and 30% each year over five years. Growth outside that range was often viewed as hard to maintain. Lululemon’s five-year Earnings Per Share (EPS) growth rate of 24.37% sits within this target area, pointing to a firm and consistent historical rise in profitability.

- Reasonable Valuation (The PEG Ratio): Maybe the most important Lynch measurement is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that may be priced low compared to their growth rate. A PEG ratio at or under 1.0 is seen as interesting. Lululemon’s PEG ratio, based on its past five-year growth, is 0.47. This indicates the market may be pricing the company’s shares at a notable discount to its historical growth path, a main sign for value-aware growth investors.

- Exceptional Profitability (Return on Equity): Lynch searched for companies that effectively create profits from shareholder equity. A high Return on Equity (ROE) is a sign of a well-run business with a lasting competitive edge. Lululemon’s ROE of 38.67% is outstanding, well above Lynch’s common limit of 15% and showing superior capital use.

- Sound Financial Health: The strategy needs companies to have a firm balance sheet to handle economic changes. Two filters are especially important:

- Debt/Equity Ratio: Lynch liked very little debt, often looking for a ratio under 0.6. Lululemon does very well here with a Debt/Equity ratio of 0.0, meaning it functions with no interest-bearing debt, giving great financial room and low risk.

- Current Ratio: This checks a company’s ability to meet short-term bills. A ratio above 1.0 is needed, and Lululemon’s 2.13 shows a very secure liquidity state.

Fundamental Soundness and Valuation Summary

A wider view of Lululemon’s fundamental profile supports the image shown by the Lynch filter. The company receives a high total fundamental score, led by excellent marks in profitability and financial health.

- Profitability Leader: The company’s margins are best in its industry. Its operating margin of 22.05% and profit margin of 15.72% are in the highest group of its competitors. The high returns on assets (21.88%) and invested capital (28.30%) further prove the efficiency and profitability of its business model.

- Firm Balance Sheet: Besides having zero debt, Lululemon has a high Altman-Z score of 6.83, meaning very low bankruptcy risk. The company has also been lowering its share count through buybacks, a action Lynch saw as positive because it raises the ownership stake of remaining shareholders.

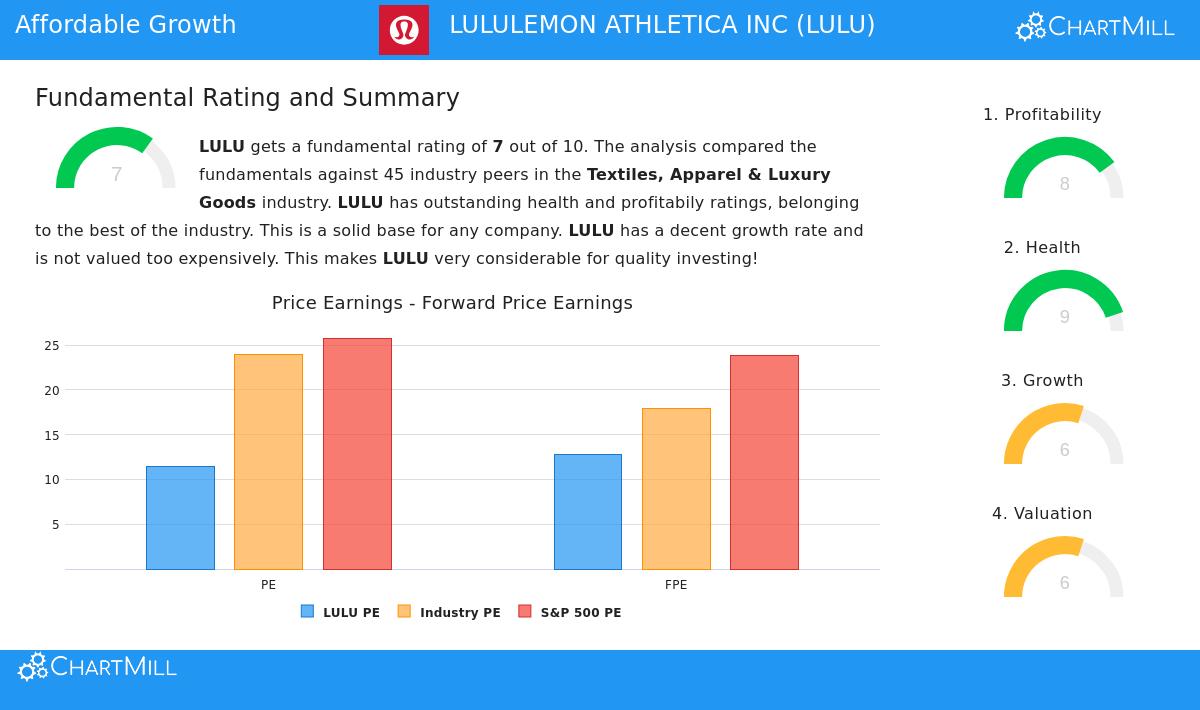

- Interesting Relative Valuation: Despite its premium brand, Lululemon’s valuation seems reasonable in comparison. Its Price/Earnings (P/E) ratio of 11.45 is not only lower than the wider S&P 500 average but also below most of its industry peers. This valuation, combined with its high growth and profitability, forms the heart of its GARP interest.

For a complete look at these measurements, you can see the full fundamental analysis report for LULU.

Points for the Long-Term Investor

While the Lynch filter shows strengths, long-term investors must also think about the path forward. Analysts expect a slowing in Lululemon’s growth, with future EPS and revenue growth forecasts clearly lower than the outstanding rates of the past five years. This expected slowdown is a key point for examination, as the investment idea depends on the company’s ability to keep above-average profitability and find new paths for growth in a competitive market. Also, the company does not pay a dividend, sending all capital toward growth projects and share buybacks.

Locating Comparable Investment Candidates

Lululemon Athletica works as a real example of how Peter Lynch's ideas can find companies mixing growth with reasonable valuation. Investors curious about finding other stocks that meet this disciplined set of filters can use the Peter Lynch Strategy stock screener for more possible ideas.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, an endorsement, or a recommendation to buy, sell, or hold any security. The analysis is based on historical data and specific investment criteria, which may not be suitable for all investors. You should conduct your own thorough research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.