For investors aiming to create a portfolio centered on producing regular income, a systematic selection method is important. One useful technique includes looking for companies that provide a good dividend now and also have the fundamental financial soundness to maintain and possibly raise those payments in the future. This method chooses quality and durability over only pursuing the biggest yield. A realistic tactic is to apply a filter that finds stocks with a strong dividend score, while also demanding a basic standard of earnings and financial condition. This makes certain the companies selected are not only good distributors, but are also fundamentally healthy and able to endure different economic periods.

Lear Corp (NYSE:LEA), a worldwide automotive technology supplier, appears as a selection from this type of filtering process. The company's basic financial picture indicates it might be a noteworthy option for dividend-oriented investors who appreciate a mix of yield, fair price, and operational steadiness.

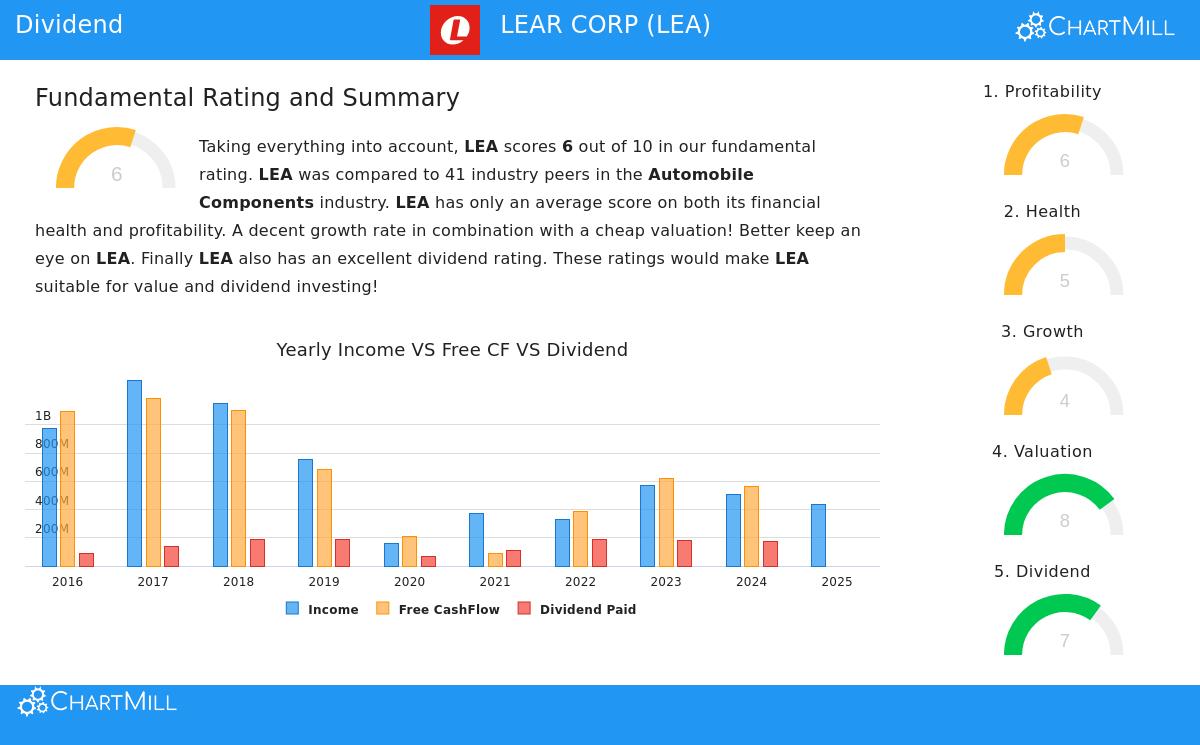

Dividend Profile: A Steady Distributor with Potential for Increase

The central attraction for dividend investors is found in Lear's consistent and maintainable distribution policy. The company's dividend traits show a mix of present income and careful financial planning.

- Good and Competitive Yield: Lear presently gives a dividend yield of 2.25%. This is higher than the typical yield of similar companies in the automobile parts sector (0.58%) and is also more than the present S&P 500 average of about 1.85%. This delivers a clear income benefit.

- Established History: Consistency is vital in dividend investing. Lear has maintained a reliable record, distributing dividends without interruption for over ten years. This lasting dedication to giving capital back to shareholders is a good sign.

- Maintainable Payout Ratio: Possibly most critical, the dividend seems firmly backed by profits. Lear's payout ratio—the part of net income given as dividends—is at a low 37.81%. This modest ratio shows the company keeps a large amount of its earnings to fund business operations, reduce obligations, or finance future dividend raises, all while presenting little danger to the existing dividend.

- Increase Possibility: While the past yearly dividend growth rate is small at 0.74%, the fundamental report states that profits are rising more quickly. This difference implies the company has the ability to raise its dividend more substantially later without pressuring its finances, matching a plan that prefers maintainable increase over large but uncertain jumps.

Supporting Basics: Earnings and Financial Condition

A big dividend yield can occasionally signal trouble if it comes from a falling stock price because of basic business problems. Lear's filter results, which asked for minimum scores for earnings and financial condition, help reduce this concern. The company's grades in these fields, while not exceptional, offer a firm base.

Earnings are sufficient, with a ChartMill Profitability Rating of 6. Important measures like Return on Equity (8.66%) and Return on Invested Capital (8.12%) are better than most industry rivals. This shows the company is creating acceptable returns on the money it uses. The profit margin, although small in this competitive field, has gotten better in recent periods.

Financial Condition gets a middle rating of 5, satisfying the filter's "acceptable" level. The balance sheet displays a workable debt amount, with a Debt-to-Equity ratio of 0.55 and a good Debt-to-Free-Cash-Flow ratio of 3.80, indicating it could eliminate all its debt in less than four years using its existing cash generation. Liquidity measures are acceptable, though they are not as strong as some industry counterparts. Importantly, the company has been lowering its number of shares over time, which is an action favorable to shareholders that can improve profits and dividend per share in the long run.

Valuation: A Low-Priced Income Source?

Apart from the dividend, Lear shows what seems to be a fairly priced chance. The stock sells at a Price-to-Earnings (P/E) ratio of 10.48 and a Forward P/E of 9.42. These numbers are not only inexpensive compared to the wider S&P 500 but are also less than about 85-90% of its industry peers. For cost-aware dividend investors, this implies the market might be setting too low a price on the company's profits and its connected income source.

A Measured Option for Income Portfolios

Lear Corp illustrates a balanced example of dividend investing. It is not a tale of fast increase or a very high-yield danger. Rather, it supplies a competitive and steady yield supported by a ten-year payment history, a highly maintainable payout ratio, and the profit growth possibility to back future raises. Its success in passing a filter needing acceptable earnings and financial condition gives extra assurance that the dividend is not facing immediate danger from operational or balance sheet problems. Combined with a seemingly low stock price, Lear offers a strong case for investors looking to include a stable, income-producing industrial business in their portfolio.

For investors wanting to examine other companies that fit similar standards of good dividend traits paired with sound basics, the pre-set "Best Dividend Stocks" filter can act as a solid beginning for more study.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investors should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. All investments involve risk, including the potential loss of principal.