For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method provides a sensible middle path. This method tries to find companies with good and lasting growth, but whose shares are not valued at the extreme levels common to high-momentum stocks. By also looking for sound financial condition and earnings, the method aims to sidestep companies that grow without regard to cost, concentrating on those with a firm operational base. One stock that recently appeared from this kind of filter is Kiniksa Pharmaceuticals International Plc (NASDAQ:KNSA), a commercial-stage biopharmaceutical company.

A Detailed View of Growth Path

The central idea of any reasonable-price growth method is, expectedly, growth. Kiniksa’s fundamental picture displays notable force here, receiving a high Growth Rating. The company is moving from a clinical-stage business to a commercial one, a change clearly seen in its financial statements.

- Strong Revenue Increase: In the last year, Kiniksa’s revenue rose by more than 60%, propelled by the commercial launch of its main product, ARCALYST, for recurrent pericarditis. The company’s average yearly revenue growth in recent years is a notable 45.45%.

- Earnings Trend: While the long-term average earnings per share (EPS) has been negative, a typical situation for companies in heavy investment periods, the latest year shows a sharp positive shift. EPS increased by 221.31% compared to the year before, marking a possible turning point toward consistent earnings.

- Solid Future Projections: Analyst forecasts support this positive view, predicting average yearly EPS growth of about 45% and revenue growth of more than 17% in the next few years. This expected future growth is a vital part for GARP investors, as it implies the company’s present expansion is likely to persist.

Valuation Considered

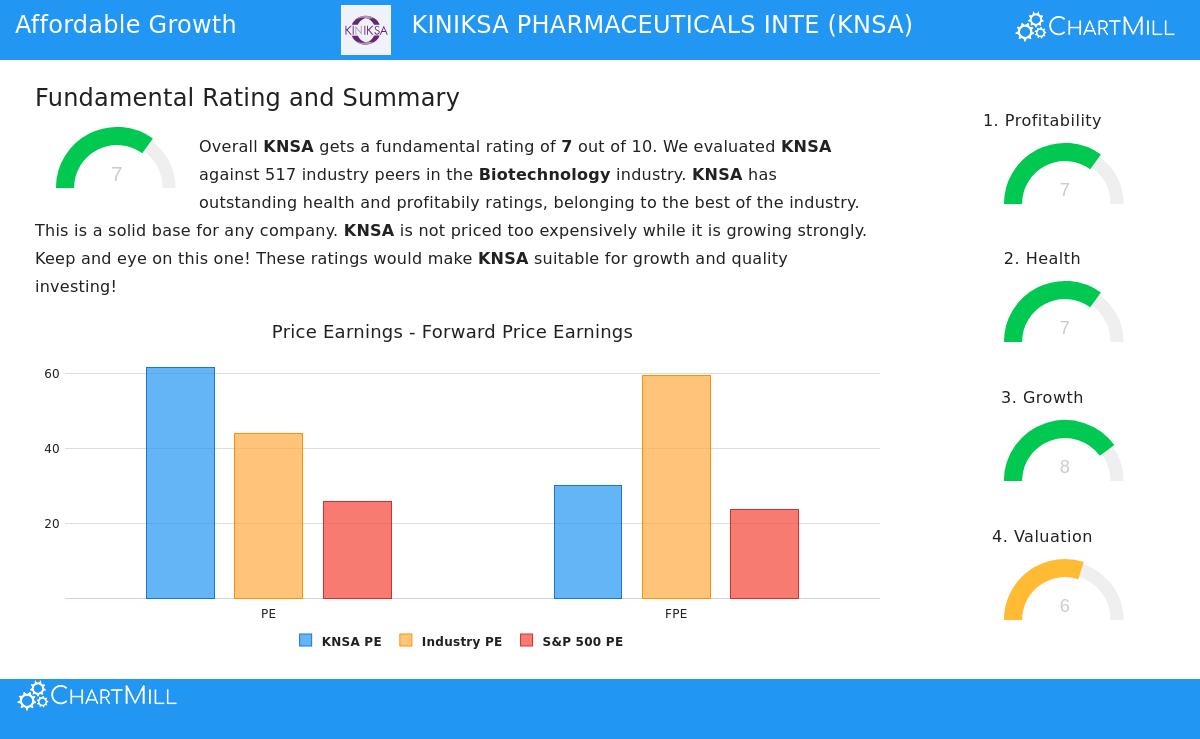

A stock with good growth can still be a bad investment if bought at an excessive cost. This is where the "reasonable price" part of the method is important. Kiniksa’s Valuation Rating points to a varied but finally positive image when measured against its industry, not the wider market.

- Absolute and Relative Measures: On a standalone basis, measures like a Price-to-Earnings (P/E) ratio over 60 and a Forward P/E close to 30 seem costly, particularly next to the S&P 500 average. This shows why filtering inside an industry setting is important.

- Industry Comparison: Compared to other biotechnology companies, Kiniksa’s valuation presents a different narrative. Its P/E and Forward P/E ratios are lower than about 90% and 92% of the industry, in turn. Also, its Enterprise Value-to-EBITDA and Price-to-Free Cash Flow ratios are more appealing than most of its rivals.

- Growth Consideration: The valuation is also viewed alongside the company’s growth picture. A small Price/Earnings-to-Growth (PEG) ratio implies the market may not completely account for the predicted earnings increase. The good earnings and high projected growth rates offer a reason that can support its present multiples for investors focused on growth.

The Supporting Basics: Condition and Earnings

A reasonable-price growth filter sensibly considers more than only growth and price. Needing acceptable scores in financial condition and earnings helps confirm the company’s growth is on a steady base and is producing actual returns, a check against "growth without purpose."

- Good Earnings Measures: Kiniksa receives a very good Profitability Rating. Its Return on Assets (7.73%), Return on Equity (10.40%), and Return on Invested Capital (8.21%) all place in the top 10% of the biotechnology industry. Also, it has high gross margins near 88.5% and an operating margin of 11.4%, showing efficient activities and product pricing strength.

- Sound Financial Condition: The company’s Health Rating is also good. A particularly clear strength is its financial position: Kiniksa has no debt, removing default risk and offering major financial room to maneuver. Its Altman-Z score of 11.67 signals a very small chance of near-term bankruptcy, and its current and quick ratios reveal sufficient cash to cover short-term needs.

Summary

Kiniksa Pharmaceuticals displays a picture that matches the goals of a reasonable-price growth investor. The company is in a strong growth period, driven by successful product launches and promising clinical programs, with analysts predicting this trend will keep going. While its valuation seems high in isolation, it is clearly moderate within the high-growth, often high-priced biotechnology field. This comparative value is supported by excellent earnings measures and a very strong, debt-free financial position. For investors, this mix indicates a company whose growth story is backed by fundamental soundness, not just theory.

A full fundamental analysis report for Kiniksa Pharmaceuticals is ready for more examination here.

Investors curious about finding other companies that match this "Affordable Growth" picture can see more filter outcomes through this link: View Affordable Growth Screen Results.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.