The investment philosophy of Peter Lynch, the legendary manager of Fidelity's Magellan Fund, focuses on finding well-run companies with solid growth prospects that are trading at reasonable prices. This "Growth at a Reasonable Price" (GARP) method avoids the extremes of pure speculation and deep-value traps, instead looking for businesses that an investor can understand and keep for the long term. A key tool for finding such opportunities is a stock screener based on Lynch's main financial criteria: sustainable earnings growth, strong profitability, a healthy balance sheet, and an attractive valuation when growth is considered.

One company that recently appeared from such a screen is JOYY Inc. (NASDAQ:JOYY), a global social entertainment platform operator known for Bigo Live, Likee, and Hago. For investors following Lynch's principles, JOYY presents an interesting case study in balancing growth, financial health, and valuation.

Meeting the Lynch Criteria

A Peter Lynch-inspired screen usually filters for companies with a specific financial profile. JOYY's current metrics show a strong match with several of these important rules.

- Sustainable Earnings Growth: Lynch preferred companies growing earnings per share (EPS) between 15% and 30% annually, as growth outside this range was often unsustainable. JOYY's five-year average EPS growth rate of 16.5% fits well within this target area, indicating a history of steady, consistent expansion.

- Attractive Valuation Relative to Growth: Perhaps the most important Lynch metric is the Price/Earnings to Growth (PEG) ratio, which aims to find stocks that may be undervalued given their growth rate. Lynch looked for a PEG ratio of 1 or less. JOYY's PEG ratio, based on its past five-year growth, is about 0.67, suggesting the market may be pricing the stock at a discount to its historical growth path.

- Strong Profitability: Return on Equity (ROE) measures how efficiently a company generates profits from shareholder equity. Lynch looked for strong profitability, often with an ROE above 15%. JOYY's ROE of 31.9% is much higher than this mark, pointing to very effective management and a possibly lasting competitive edge in its industry.

- Financial Health: A conservative balance sheet was very important to Lynch. He favored companies with very little debt and good liquidity to handle difficult periods.

- JOYY's Debt-to-Equity ratio is a very low ~0.002, showing it is funded almost completely by equity, not debt. This matches Lynch's liking for low leverage.

- The company's Current Ratio of 1.85 indicates it has more than enough short-term assets to cover its immediate debts, meeting Lynch's test for financial stability.

Fundamental Health Check

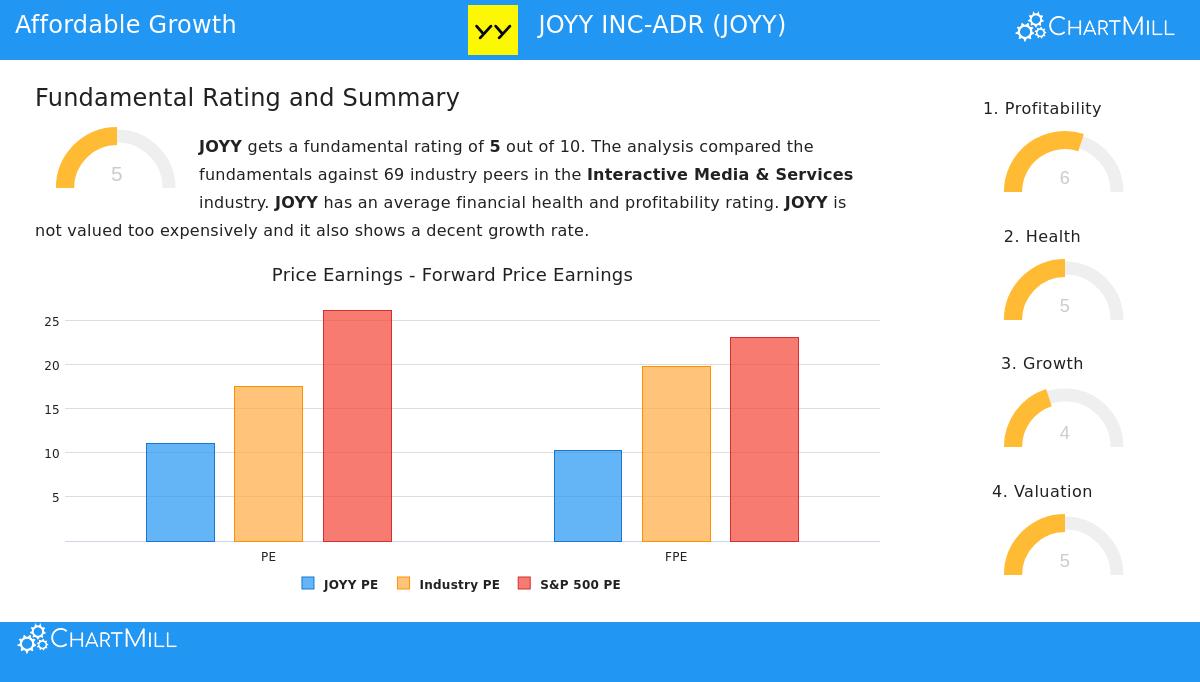

A wider view of JOYY's fundamental picture, as detailed in its full fundamental analysis report, shows a mixed but generally acceptable profile. The company receives an overall fundamental rating of 5 out of 10, indicating a neutral to fair position within the competitive Interactive Media & Services industry.

The analysis points out several positive points for a long-term investor:

- Valuation: JOYY trades at a P/E ratio of 11.02 and a Forward P/E of 10.23, which are seen as very reasonable and are lower than most of its industry peers and the wider S&P 500.

- Profitability & Dividends: The company has excellent profit and return on equity margins. Also, it provides a large dividend yield of 7.48%, which is higher than industry and market averages.

- Solvency: Its very clean balance sheet, with almost no debt and a healthy Altman-Z score, indicates very low bankruptcy risk.

However, the report also notes areas to examine, including a low Return on Invested Capital (ROIC), a recent year-over-year drop in revenue, and a gross margin that is behind many industry competitors. These factors add to the neutral overall score and highlight the need for more detailed research.

Is JOYY a Lynch-Style "GARP" Candidate?

For an investor using the GARP principles of Peter Lynch, JOYY presents a strong quantitative case. It shows a history of the sustainable earnings growth Lynch valued, along with excellent profitability and a very strong balance sheet that fits his focus on financial health. Most importantly, its low PEG ratio suggests the market may not be fully valuing this growth history, a typical Lynch buying signal.

The company works in the active and understandable area of social interaction and live streaming, a business model whose use can be seen worldwide. While the fundamental report shows areas where the business could better its operational efficiency, the main Lynch criteria of growth, valuation, profitability, and safety seem to be satisfied.

Interested in finding other companies that fit this disciplined method? You can run the Peter Lynch screen yourself and see the current results by clicking here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. The analysis is based on publicly available data and a specific investment strategy framework. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.