For investors looking to balance opportunity with care, the "Growth at a Reasonable Price" (GARP) method offers a sensible middle path. This method tries to find companies showing strong and lasting growth, but whose shares are not trading at very high prices. It avoids the high-risk attraction of speculative growth stocks while also avoiding the potential problems that can come with very low-priced companies. By concentrating on firms with good fundamentals, including healthy earnings and a stable financial position, together with good growth prospects, the GARP method tries to build a portfolio set for consistent, long-term increase in value.

Jabil Inc (NYSE:JBL), a worldwide manufacturing solutions provider, recently appeared in an "Affordable Growth" stock scan made to find such GARP possibilities. The scan looks for stocks with a high growth score (above 7 out of 10), along with acceptable scores in earnings, financial strength, and price (all above 5). This multi-part review is important; strong growth loses its attraction if it comes from a financially weak company, and even the best fundamentals are not a good deal if the price is too high. Jabil's presence suggests it deserves more examination for investors using this careful method.

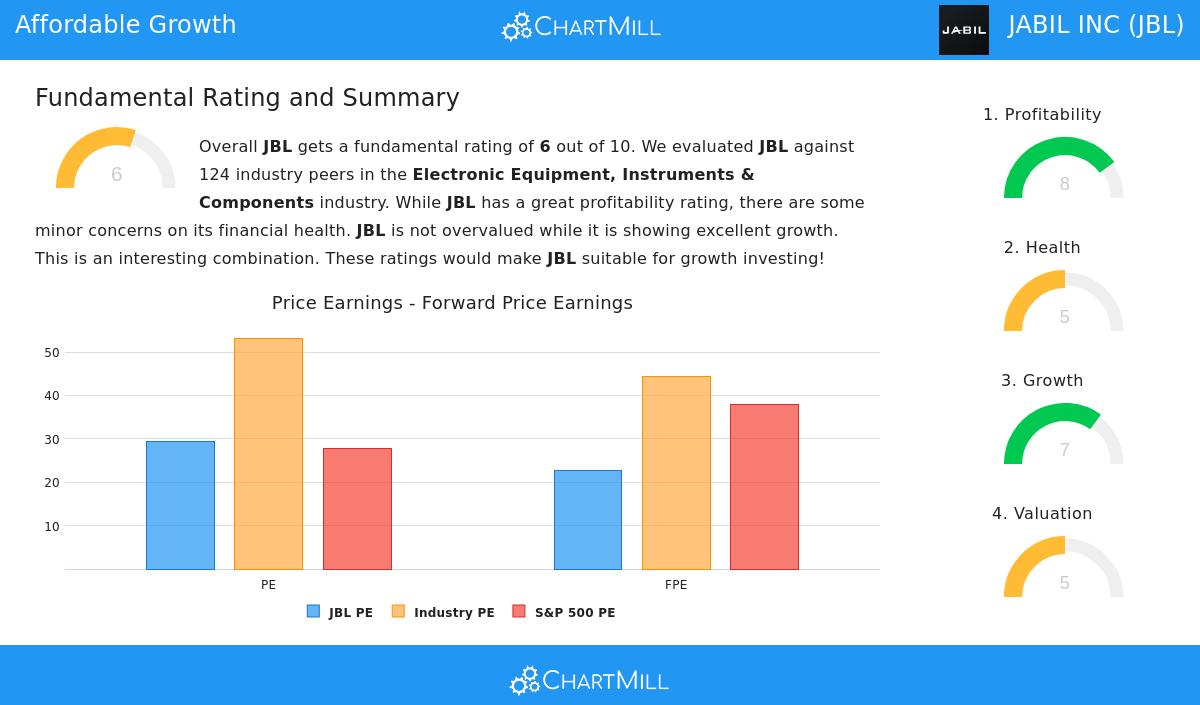

A Detailed Examination of Growth and Price

The center of the GARP argument for Jabil depends on the meeting point of its growth path and its present market valuation. The company's fundamental report shows a strong story on both points.

Growth Measures:

- Recent Results: Jabil has reported notable bottom-line growth, with Earnings Per Share (EPS) rising by 39.98% over the last year. This is part of a longer pattern, with EPS increasing at an average yearly rate of 27.52% over recent years.

- Future View: Analyst predictions indicate this pace is not temporary. EPS is projected to grow by an average of 20.49% each year in the next few years, while Revenue is expected to rise by 11.37% per year.

Price Evaluation:

- Comparative Value: While Jabil's own Price-to-Earnings (P/E) ratio of 29.32 may seem high, perspective matters. Compared to other companies in its industry in the Electronic Equipment, Instruments & Components sector, Jabil is priced lower than about 72% of firms. Its Forward P/E ratio of 22.66 is also under the industry average.

- Growth Adjustment: The PEG ratio, which modifies the P/E for projected earnings growth, shows the stock is fairly priced considering its growth outlook. The report states that Jabil's excellent earnings ability may further support its current price multiple.

This pairing, solid past and expected growth combined with a price that is sensible compared to its industry, is exactly what the affordable growth scan and the wider GARP method aim to find.

Supporting Basics: Earnings and Financial Strength

For growth to be lasting and the price to be a true "reasonable price," the core business must be stable. Jabil's scores in earnings and financial strength give important support for the investment thesis.

Earnings Power: Jabil receives a high earnings score of 8/10. Important advantages include:

- Steady Earnings and Cash Generation: The company has been profitable and produced positive operating cash flow in each of the last five years.

- Effective Capital Use: Its Return on Invested Capital (ROIC) of 21.25% is very good, doing better than almost 98% of industry competitors and well above its cost of capital, meaning it is building real value for shareholders.

- Getting Better Margins: Both Operating Margin and Profit Margin have shown good movement in recent years, showing better operational performance.

Financial Strength Points: With a strength score of 5/10, the view is more balanced but generally steady. Good points include a stable Altman-Z score pointing to low short-term risk of failure and an acceptable Debt-to-Free-Cash-Flow ratio. However, investors should be aware of the company's fairly high debt-to-equity ratio and lower liquidity measures (Current and Quick Ratios) compared to industry norms. These items are not immediate warnings but are topics for continued attention, as they show the company's use of outside financing and closer management of working capital.

Summary and Next Steps

Jabil Inc shows an example of the kind of company sought by affordable growth scans. It shows the effective pairing of solid, predicted earnings growth and a price that does not seem high within its industry. Supported by high-level earnings measures and sufficient, though not excellent, financial strength, it fits the GARP idea of looking for quality growth without paying too much.

Naturally, no single scan or report gives a full investment view. Broader economic conditions, industry-specific changes, and company performance risks all have an effect. Jabil's work across different areas like automotive, healthcare, and cloud infrastructure links its success to wider economic conditions.

For investors wanting to look at other companies that match this "Affordable Growth" outline, you can see the full scan details and findings here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.