For investors looking for a steady flow of passive income, a disciplined screening method is needed to tell reliable payers from risky choices. One useful technique involves selecting for stocks that not only have a high dividend rating but also show good basic business condition and earnings. This method focuses on longevity, trying to find companies with the monetary ability to keep and possibly increase their payments over time, instead of just following the highest present yield. A stock that recently appeared from such a filter is Illinois Tool Works (NYSE:ITW), a varied industrial maker whose basic profile deserves more attention from dividend-oriented portfolios.

A Dividend Profile Made for Dependability

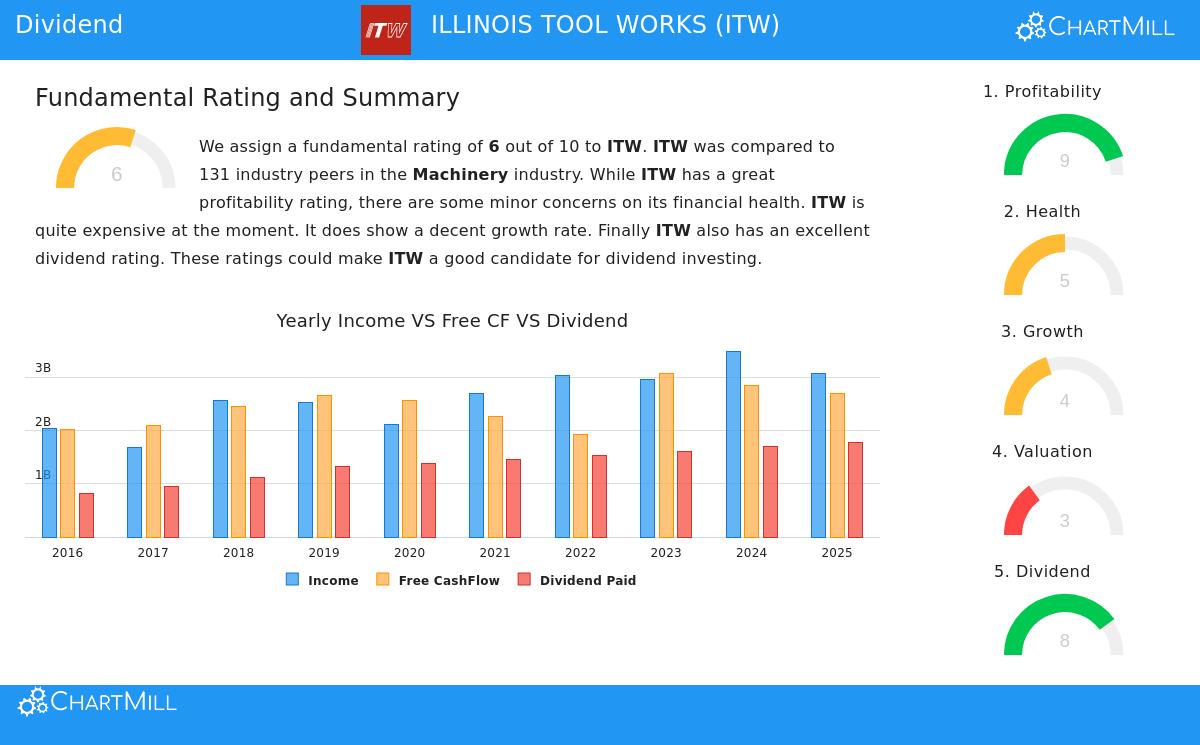

At the heart of any dividend investment idea is the payment itself, and ITW makes a strong argument based on the measures most important to income investors. The company receives a solid ChartMill Dividend Rating of 8 out of 10, a number that combines several important elements into one, practical measure.

- Yield and Growth: ITW provides a dividend yield near 2.46%. This yield is notably higher than the industry norm of 1.20% and a bit above the present S&P 500 average. Significantly, it is supported by a steady and dependable record. ITW has both paid and raised its dividend each year for at least ten years, reaching a good 5-year annualized dividend growth rate of 7.19%. This pairing of an above-normal yield and a promise of yearly increases is a sign of an established, shareholder-focused company.

- Payout Longevity: A high yield is only appealing if it can last. Here, ITW’s basic finances give confidence. The company’s payout ratio—the part of earnings given as dividends—is near 58%. This is a workable level that keeps a good part of profits for putting back into the business, lowering debt, or share repurchases. Importantly, analyst projections indicate that ITW’s earnings are predicted to rise at a rate that allows for the continued growth of its dividend, showing the present plan is on a firm base.

This emphasis on a strong dividend rating is key to the screening plan because it looks past a single yield number to judge the quality, growth, and staying power of the income flow, elements vital for long-term dividend investors.

The Earnings Machine Backing the Payment

A lasting dividend must be paid for by a profitable business. ITW’s outstanding earnings, shown in a ChartMill Profitability Rating of 9, supplies that needed support. The company works with industry-best efficiency and margin strength.

- Better Returns: ITW produces a Return on Equity (ROE) above 95% and a Return on Invested Capital (ROIC) close to 27%, numbers that greatly exceed most of its competitors in the machinery industry. This shows management’s excellent ability to create profits from the capital given to it.

- Strong Margins: The company’s finances are marked by good and improving margins. Its operating margin is a notable 26.3%, and its profit margin is over 19%, both placed in the top group of its field. High and steady margins are a main sign of competitive benefit and pricing ability, which then provide protection in economic slowdowns and make sure cash flow stays sufficient to pay for the dividend.

This earnings ability is essential for the screening method. A high dividend rating becomes less meaningful if the basic company is not regularly profitable. ITW’s top-level earnings measures imply the dividend is being paid from a place of real monetary ability, not from borrowed funds or asset liquidation.

Evaluating Financial Condition and Valuation Points

The screening method also requires a minimum level of financial soundness, a protection against too much risk. ITW’s ChartMill Health Rating of 5 shows a varied but acceptable situation. On the good side, the company’s Altman-Z score is very good, indicating a very small short-term chance of financial trouble. Still, investors should be aware that ITW holds a larger-than-normal debt amount, with a Debt-to-Equity ratio of 2.47, and its liquidity ratios (Current and Quick Ratio) are below industry norms. While the high earnings and strong cash flow help manage this debt, it is an area to watch over time.

From a valuation view, ITW sells at a high price. With a P/E ratio near 24.7, it is valued similarly to both the wider S&P 500 and its industry equals. This suggests the market has already accounted for its quality and dependable dividend, allowing less room for mistake. The valuation rating of 3 points out that investors are paying for quality, not a low price.

Conclusion

Illinois Tool Works comes from a strict dividend screen as a choice that mixes a wanted income flow with strong business basics. Its attraction exists in the connection between a dependable, growing dividend (Rating: 8) and the outstanding corporate earnings (Rating: 9) that support it. While its financial soundness displays some debt and its valuation is high, the total profile is of a high-quality industrial business with a firm dedication to giving capital back to shareholders. For an investor whose plan focuses on lasting income from monetarily sound companies, ITW presents a strong example. A closer look at its full fundamental analysis report is suggested for a full view.

The "Best Dividend Stocks" screen that found ITW is made to create a list of such ideas. You can review the present results and change the filters to fit your particular needs by going to the live screen here.

Disclaimer: This article is for informational and educational reasons only and does not form financial advice, a recommendation, or an offer or request to buy or sell any securities. The study is based on present data and past performance, which is not a guide to future outcomes. You should do your own research and talk with a qualified financial advisor before making any investment choices.