For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method provides a sensible middle path. This method tries to find companies that are increasing their earnings and revenue at a rate above the average, but whose stock prices are not at very high levels. It steers clear of the speculative edges of pure momentum investing while still focusing on businesses with good forward progress. One way to find these opportunities is through systematic filtering, searching for stocks that display good growth foundations, sound financial condition, high profitability, and a fair price. A recent filter for "Affordable Growth" stocks has identified INTUIT INC (NASDAQ:INTU) as a company that fits these requirements.

Growth Path and Progress

The central idea of any GARP method is, expectedly, growth. A company must show a clear ability to increase in size and have the outlook to keep doing so. Intuit’s fundamental report shows a good history and positive future estimates, which are important for investors who want growth that is supported by financial performance.

- Past Results: Over the last year, Intuit increased its Earnings Per Share (EPS) by a notable 23.74%. Over a longer period, the company has maintained an average yearly EPS growth of 20.77% and revenue growth of 19.65% over recent years. This steady, double-digit increase in both revenue and profit is a sign of a company performing well in its field.

- Future Outlook: While past performance does not assure future results, analysts forecast a continued good growth path. Intuit is expected to grow its EPS by about 12.48% each year in the near future, with revenue predicted to rise by about 12.00% per year. Although these forward estimates show a slowing from the higher past rates, they still indicate a quite strong growth outlook that is faster than many established software companies.

This mix of very good historical growth and a reliable projected path is exactly what a GARP filter aims to find, companies where growth is a lasting feature, not a temporary event.

Price Evaluation

If growth were the only factor, investors might pursue the fastest-increasing companies without regard for cost. The "reasonable price" part is what shapes the GARP approach and helps limit risk. Intuit’s price measurements suggest the market is not assigning an overly hopeful or unmaintainable growth price, making it seem "affordable" compared to its industry.

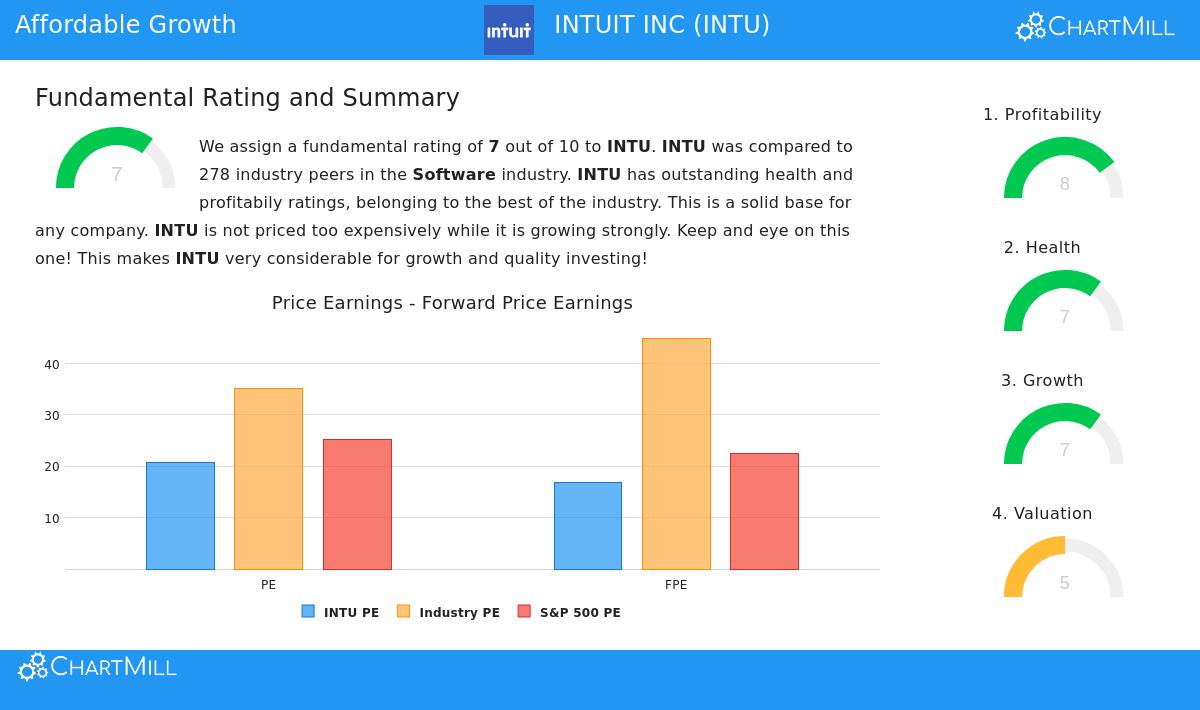

- Industry Comparison: Intuit sells at a Price/Earnings (P/E) ratio of 20.81. While this may seem high by itself, it is important to compare it to its industry. Almost 70% of the companies in the software industry have a higher price than Intuit based on this common measurement. More forward-looking measurements are even more positive: its Price/Forward Earnings ratio of 16.91 is lower than over 71% of its industry competitors.

- Cash Flow and EBITDA: The price narrative becomes stronger when examining cash generation. Intuit’s Price/Free Cash Flow and Enterprise Value to EBITDA ratios are lower than about 75% and 73% of the industry, in that order. This shows the market is pricing its good cash flows at a relative value.

- Market Comparison: Compared to the wider S&P 500, which has an average forward P/E above 22, Intuit’s price also seems fair. When considering its expected growth rate, resulting in a PEG ratio that suggests a fair price, the argument for it being a reasonably priced growth stock is supported.

Foundations of Profitability and Financial Condition

A company can grow fast and seem inexpensive, but if it loses money or is financially weak, it carries notable risk. The GARP method inherently needs a base of quality, which Intuit shows through high profitability grades and good financial health.

- Profitability Quality: Intuit receives a very good profitability rating, led by top-tier margins and returns. Its Operating Margin of 27.09% and Return on Invested Capital (ROIC) of 17.51% are better than over 90% of its software industry competitors. High profitability like this offers protection during economic slowdowns and supports more reinvestment for growth, making the company's expansion more maintainable.

- Financial Strength: The company’s financial health rating is good, supported by a strong balance sheet. Important stability metrics are sound: an Altman-Z score of 7.00 indicates no bankruptcy danger, and a low Debt-to-Free Cash Flow ratio of 0.90 means it could pay off all its debt in under a year using its cash flow. This financial stability lowers the risk linked to its growth path and allows for strategic spending or returns to shareholders.

Summary and Additional Study

Intuit Inc. shows a profile that matches closely with the goals of an affordable growth investment method. It combines a history and expectation of strong, double-digit growth with a price that is fair, even appealing, compared to its successful software peers. This growth is supported by very high profitability and a very strong financial base, addressing important risk points for investors. While the wider market displays a negative long-term direction, finding companies with these fundamental traits can be a way to look for stability and potential.

It is necessary to perform complete personal research. Investors can examine the full, detailed fundamental analysis for INTU here.

For those wanting to find other companies that match this "Affordable Growth" profile, you can inspect the predefined filter and its present results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for any investment decision. Investing involves risk, including the potential loss of principal. Always conduct your own research and consider consulting with a qualified financial advisor before making any investment decisions.