For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish truly lasting dividend payers from risky high-yield situations. One useful approach includes looking for companies that provide a good dividend and also have the basic financial soundness to keep and possibly increase those payments. This method favors stocks with a high ChartMill Dividend Rating, which assesses yield, growth, and sustainability, while also demanding a foundation of acceptable profitability and financial soundness. This two-part aim helps find companies where the dividend is backed by a solid business, instead of being a temporary sign of a low stock price.

Hormel Foods Corp. (NYSE:HRL), the Minnesota-based packaged food company known for brands like SPAM, Skippy, and Applegate, appears as a candidate from such a screen. Its fundamental profile presents a strong, though detailed, argument for dividend-focused investors, balancing a notable yield with aspects needing close examination.

A Notable Dividend Yield

The most direct appeal for income investors is Hormel's dividend yield, which is a major part of its high ChartMill Dividend Rating of 7.

- Good Current Yield: The stock provides a yearly dividend yield of 5.12%. This is over twice the industry average for food products (2.44%) and notably higher than the present S&P 500 average of about 1.88%.

- Dependable History: The company has built a long and steady dividend record, having paid and, significantly, not reduced its dividend for at least ten straight years. This steadiness is a sign of dividend dependability.

- Small but Consistent Growth: The dividend has increased at an annual rate of about 4.90% over the past five years. While not high, this consistent growth shows management's dedication to giving capital back to shareholders even in difficult times.

For the dividend-focused method, these points are key. A yield much higher than the market and sector averages delivers real income, while the long record of payments and raises indicates a corporate priority on shareholders.

Assessing Profitability and Financial Soundness

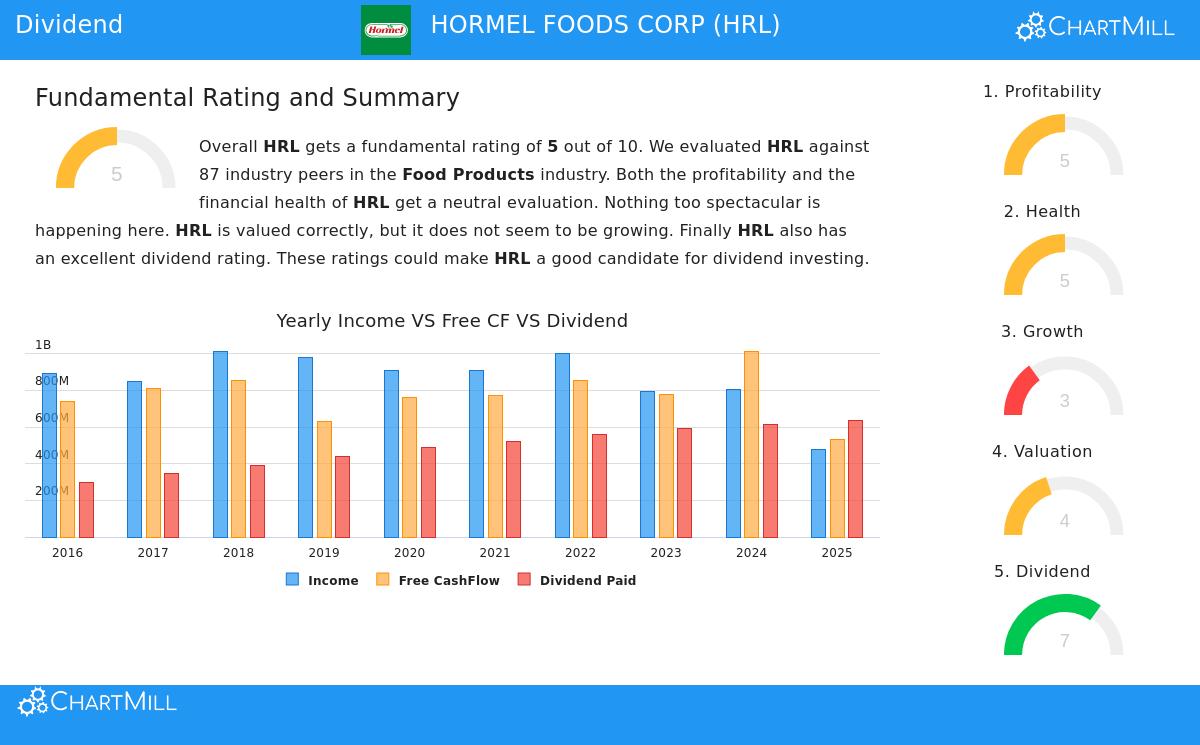

A high yield by itself is insufficient; it must be supported by a company that can pay for it. The screening rules of "acceptable profitability and soundness" (both scoring 5 in ChartMill's ratings) exist to confirm this. Hormel's report displays a varied but satisfactory view in these areas.

Profitability measures are neutral. The company is steadily profitable and produces positive cash flow. Important return figures like Return on Assets (3.68%) and Return on Equity (6.17%) are in the stronger part of its industry group. However, margins have experienced pressure in recent years, with drops seen in Gross, Operating, and Profit Margins. This shows the company is managing cost inflation and market pressures, which is a point for investors to watch.

Financial Soundness is similarly satisfactory. The company keeps a good liquidity position, with a Current Ratio of 2.66, showing no near-term solvency issues. Its Debt/Equity ratio of 0.36 is viewed as sound. However, the report notes that the company's Return on Invested Capital is now below its cost of capital, meaning it is not generating extra value from its investments currently. There has also been a rise in shares outstanding and a decline in the debt-to-assets ratio year-over-year.

This background is important for the dividend method. The acceptable soundness and profitability scores verify that, in spite of some challenges, Hormel is not in financial trouble. Its capacity to meet near-term obligations and handle its debt supports the idea that the present dividend is not at immediate risk from a weak balance sheet.

The Key Question of Sustainability

This brings us to the most important part of dividend study: sustainability. Here, Hormel shows a clear warning that investors must balance against its good yield. The company's payout ratio—the part of net income paid as dividends—is at 130.30%. This is above 100%, meaning Hormel is distributing more in dividends than it made over the last twelve months, a condition that cannot last forever.

This high payout ratio is probably a short-term outcome of the recent earnings pressure noted earlier. The fundamental report mentions a positive indicator: the dividend's growth rate matches expected earnings growth. If earnings improve as analysts forecast (with EPS predicted to grow about 5.7% each year), the payout ratio should return to normal, making the dividend growth more lasting. This situation clearly shows why the screening method looks past the yield to profitability and soundness; it helps find cases where a high yield may be a short-term chance instead of a permanent warning sign.

Valuation and Growth Background

From a valuation viewpoint, Hormel seems fairly priced. Its Price/Earnings ratio of 16.24 is lower than both the wider S&P 500 and most of its industry group. This indicates the market has already accounted for the present difficulties. The growth prospect is low, with small single-digit growth expected in both revenue and earnings, which is normal for an established consumer staples company.

A complete outline of Hormel's fundamental positives and negatives is available in its full ChartMill Fundamental Analysis Report.

Conclusion

Hormel Foods illustrates a standard case for the methodical dividend screening process. It provides a high, dependable yield supported by a well-known brand collection and a long company history, qualities highly valued by income investors. The screen effectively found it by focusing on a high dividend rating while filtering for sufficient financial soundness and profitability. These filters are what let an investor view a high payout ratio not as an automatic reason to avoid, but as a particular risk to be assessed within the setting of the company's overall steady operations and rebound possibility.

For investors at ease with an established, slow-growth business managing a difficult margin climate, Hormel's higher yield could be a good starting point, if they accept the company's ability to achieve an earnings rebound. As usual, this single idea is a beginning for more study.

This analysis came from a systematic screen for good dividend payers. You can review the present results of this "Best Dividend Stocks" screen and find other possible candidates here.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer or request to buy or sell any securities. The information shown is based on data supplied and should not be the only foundation for any investment choice. Investors should do their own study and talk with a qualified financial advisor before making any investment decisions. Past results do not guarantee future outcomes.