For investors looking for steady income, a methodical screening process is necessary. One useful technique is to find companies that provide a good dividend now and also have the fundamental financial soundness to maintain and possibly increase those payments in the future. This requires examining more than just the current yield to evaluate earnings, which supply the dividend, and balance sheet strength, which guarantees the company can manage economic difficulties without reducing its payout. A stock that performs favorably in these three areas, dividend quality, earnings, and balance sheet strength, makes a strong argument for a portfolio focused on dividends.

Hormel Foods Corp (NYSE:HRL) appears as a candidate for more detailed study with this multi-part method. The packaged food company, recognized for brands such as SPAM, Skippy, and Applegate, functions in a generally stable industry, supplying goods that stay necessary even in times of economic stress. This trait creates a firm base for a steady dividend.

Dividend Appeal: A High Yield with a Reliable History

The main draw for income investors is HRL's dividend characteristics, which join a high present yield with a lengthy history of dependability.

- High Yield: Hormel presently gives a dividend yield near 4.84%. This is much greater than the average yield of the S&P 500 (near 1.82%) and the average for similar companies in the Food Products industry (about 2.30%). For an investor looking for income, this offers a good beginning.

- Established History: Dependability is vital in dividend investing. Hormel has built a steady history, having paid and, critically, not lowered its dividend for at least the last ten years. This shows management's dedication to giving capital back to shareholders across different market periods.

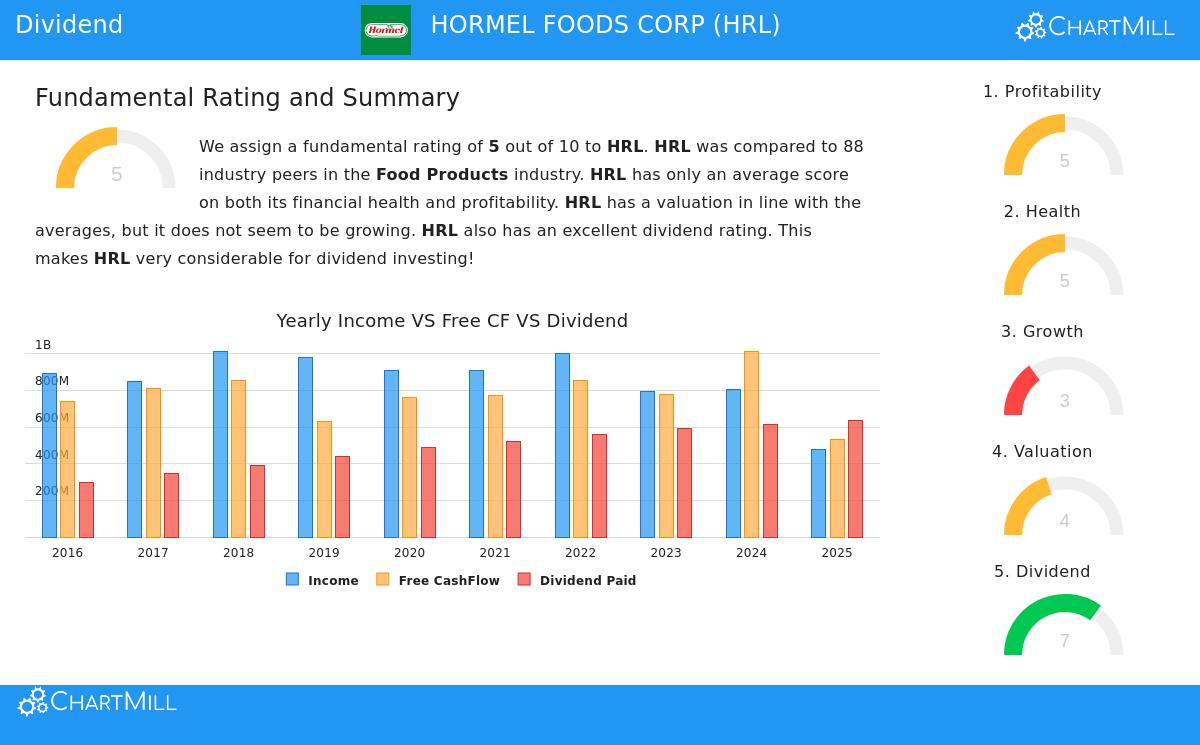

- Continued Growth? The dividend has increased at a yearly rate near 4.9% over the last five years, which is small but good. Analysts think earnings will increase at a comparable rate in the next few years, implying this speed of dividend growth might continue. But, a point of care comes from the payout ratio, which is now above 130% of earnings. This shows the company is distributing more than it makes, which is usually not maintainable over a very long period without using cash savings or borrowing. Investors ought to watch this measure for change.

Supporting Pillars: Earnings and Balance Sheet Strength

A high dividend is only as sound as the company behind it. Hormel's results in earnings and balance sheet strength give background for its dividend score.

Earnings Supply the Funds A company must earn money to fund payments to shareholders. Hormel's earnings score is average, showing a varied situation. Positively, the company has been regularly profitable and produces positive cash flow. Its profit margin and operating margin are also superior to many in its industry. Negatively, these margins have faced pressure and have fallen in recent years, a pattern management will need to address to firm up the base for future dividend raises.

Balance Sheet Strength Gives Safety Balance sheet strength is the buffer that guards the dividend in hard periods. Hormel's strength score is also average, constructed on a good foundation with some points of attention. The company's liquidity is sound, with a current ratio showing no issue meeting immediate needs. Its debt measures, like a fair debt-to-equity ratio and a sound Altman-Z score, indicate a low close-term chance of financial trouble. However, the report states that the company's return on invested capital is now under its cost of capital, meaning it is not generating extra value from its investments, and its count of shares has risen, which can lessen value for current shareholders.

Valuation and Growth Setting

From a price standpoint, Hormel seems fairly valued. Its Price-to-Earnings (P/E) ratio is lower than the wider market and much of its industry, suggesting the stock is not priced too high. The growth prospect, however, is limited. The company is predicted to achieve only low single-digit growth in both sales and earnings soon. This matches its place in a developed industry and backs the view of it mainly as an income choice instead of a fast-growth investment.

Is HRL a Fit for a Dividend Portfolio?

For an investor using a screen that emphasizes a high dividend score backed by acceptable earnings and strength, Hormel Foods offers a detailed case. It firmly satisfies the dividend needs with its high yield and very good payment history. It partly satisfies the supporting needs, displaying sufficient but not outstanding earnings and strength, with some measures needing careful watching. The high payout ratio is the main warning, needing focus to make sure future earnings can support the dividend.

This analysis shows why the screening standards matter: the dividend score emphasizes the income possibility, the earnings check makes certain the money exists to pay it, and the strength evaluation judges the company's capacity to keep doing so during tests. A complete summary of these scores for HRL is available in its detailed fundamental analysis report.

Hormel Foods might be a candidate for the income-focused part of a portfolio, especially for investors who appreciate the stable quality of the consumer staples industry and a long dividend record. As is standard, it should be viewed as part of a varied plan.

Interested in reviewing other stocks that meet a comparable dividend-focused screen? You can see the complete list of candidates by going to the Best Dividend Stocks screener.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or a bid to buy or sell any securities. The information given is from supplied data and should not be the only reason for any investment choice. Investors must do their own separate study and talk with a qualified financial advisor before making any investment choices. Past results do not guarantee future outcomes.