When searching for long-term investments, the goal is often to find companies that can grow their earnings consistently without paying a premium for that growth. This approach, sometimes called Growth at a Reasonable Price (GARP), sits between pure growth investing and strict value investing. One well-known framework for this style comes from legendary fund manager Peter Lynch, who famously averaged a 29.2% annual return running the Magellan Fund. His strategy focuses on companies with sustainable earnings growth, strong profitability, and reasonable valuations, a combination that can be hard to find in today’s market.

Hamilton Lane Inc - Class A (NASDAQ:HLNE) is a company that appears to check many of the boxes Lynch looked for. The firm provides private markets investment solutions, including private equity, private credit, real estate, and infrastructure. The business model is straightforward and understandable, which Lynch considered a major advantage for retail investors. The company went public in 2017 and has since built a track record that aligns well with the criteria from the Peter Lynch screen.

Meeting the Core Criteria

The Peter Lynch screen used to find HLNE applies several key filters designed to identify growing companies that are financially healthy and reasonably priced. Let’s look at how Hamilton Lane measures up against the most important rules.

-

Earnings Growth Between 15% and 30%: Lynch insisted that growth should be strong but not unsustainable. HLNE has delivered an EPS growth rate of 20.18% over the past five years. This lands right in Lynch’s sweet spot, fast enough to show real momentum, but not so hot that it signals a bubble or unsustainably rapid expansion.

-

PEG Ratio Below 1.0: The PEG ratio adjusts the price-to-earnings ratio for growth, helping investors see whether they are overpaying for future earnings. Lynch wanted a PEG below 1.0 to ensure the stock was not priced too richly. HLNE’s PEG (based on past five-year growth) stands at 0.84, meaning the market is valuing its growth at a discount relative to the earnings expansion rate.

-

Debt-to-Equity Below 0.6: A healthy balance sheet was crucial for Lynch, who preferred companies funded more by equity than debt. HLNE’s debt-to-equity ratio is 0.32, well under the 0.6 threshold and even below Lynch’s personal preference of 0.25. This indicates the company is not overly leveraged and can weather economic downturns more comfortably.

-

Current Ratio Above 1.0: Short-term financial health is measured by the current ratio, which compares current assets to current liabilities. HLNE reports a current ratio of 1.20, meeting the minimum requirement and showing it has enough liquidity to cover near-term obligations.

-

Return on Equity Above 15%: Profitability is a non-negotiable for Lynch. HLNE’s return on equity is 26.61%, far exceeding the 15% threshold. This suggests the company is efficient at generating profits from shareholders’ equity.

A Closer Look at the Fundamentals

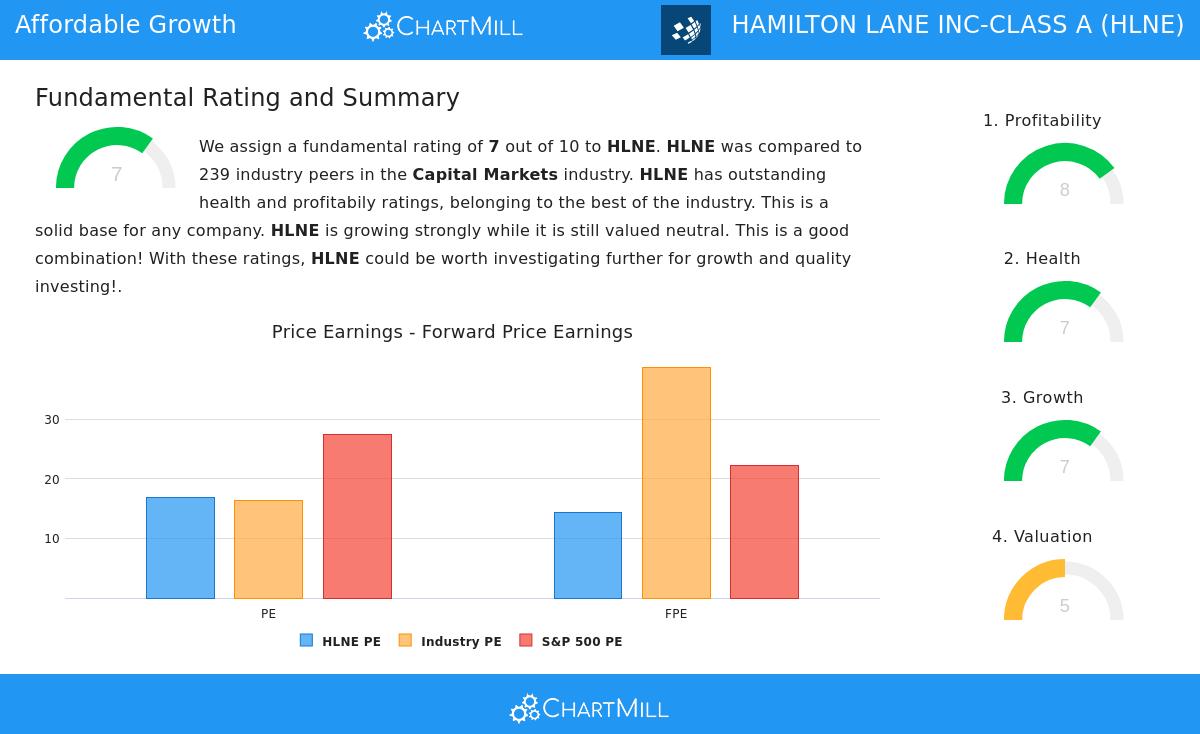

Beyond the screen criteria, a deeper analysis reinforces the quality of this company. The fundamental report gives HLNE an overall rating of 7 out of 10, driven by standout scores in profitability and health.

-

Profitability (Score: 8/10): The company performs strongly across the board. Return on assets is 10.76%, return on invested capital is 16.05%, and the profit margin sits at 30.59%. All three metrics rank among the top quartile of companies in the Capital Markets industry.

-

Health (Score: 7/10): The Altman-Z score of 3.72 indicates very low bankruptcy risk, and the debt-to-FCF ratio of 0.79 means the company could theoretically pay off all its debt in less than a year using free cash flow. Liquidity ratios are adequate and in line with industry peers.

-

Valuation (Score: 5/10): The P/E ratio of 16.91 is reasonable compared to the S&P 500 average of 27.42. The enterprise value-to-EBITDA ratio also suggests the stock is cheaper than about 73% of its industry peers. While not screamingly cheap, the valuation is fair given the growth rate.

-

Growth (Score: 7/10): Past revenue growth has averaged 21.08% annually, and future EPS growth is expected to come in around 16.88% per year. This consistency is exactly what Lynch looked for, steady, predictable expansion without sudden spikes or drops.

Final Thoughts and Next Steps

Hamilton Lane appears to embody the GARP philosophy that Peter Lynch championed, a growing, profitable company with a reasonable valuation and a solid balance sheet. For investors looking to build a long-term, buy-and-hold portfolio, this kind of profile offers a strong foundation.

If you are interested in finding other stocks that fit this same disciplined framework, you can explore more results from the Peter Lynch screen to see what other opportunities might be hiding in plain sight.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own research before making any investment decisions.