For investors looking to find opportunities where a company's market price may not match its actual value, a systematic, fundamental method is necessary. One approach is to filter for stocks that show a good valuation picture, trading below their estimated worth, while also holding acceptable results in other important categories such as financial condition, earnings, and expansion. This technique seeks to find possibly underpriced securities that are not weak businesses, but instead operationally solid firms currently overlooked by the market. The reasoning is simple: an inexpensive stock is only a worthwhile investment if the firm is fiscally secure, able to produce earnings, and set for some future expansion.

A recent filter using this approach has identified GLOBANT SA (NYSE:GLOB), a worldwide digital and cognitive transformation firm. Based on a detailed fundamental review, GLOB displays an interesting picture that matches the central ideas of this value-focused technique.

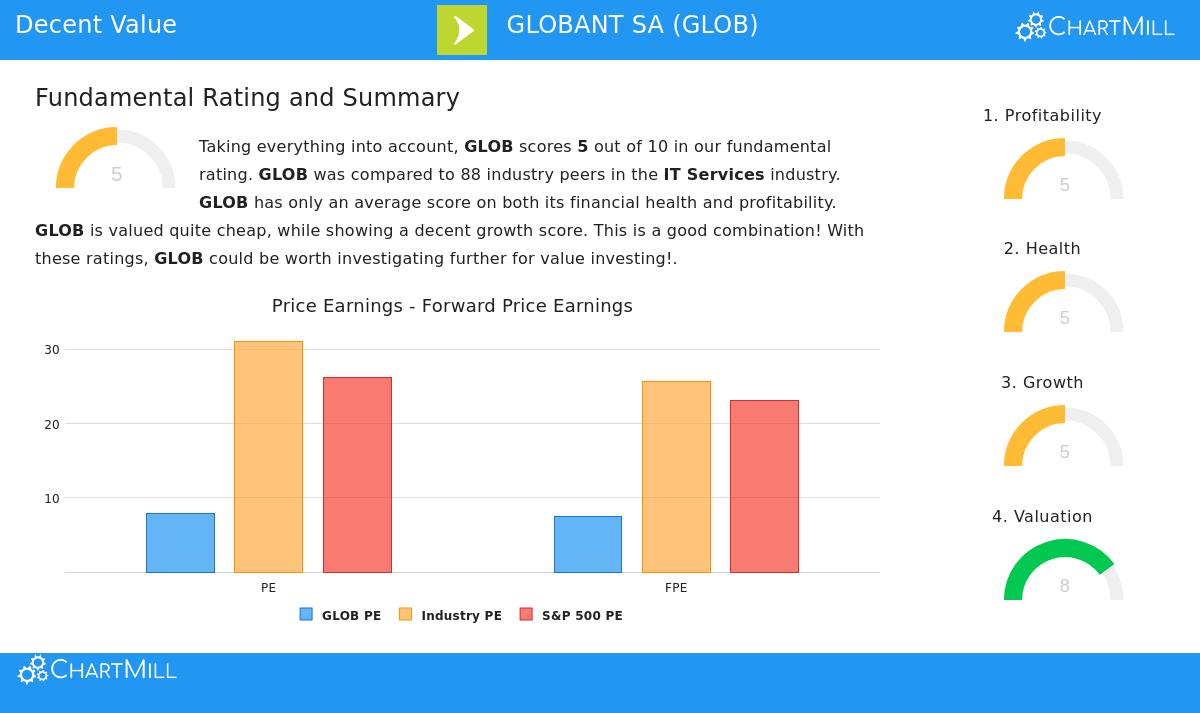

A Notable Valuation Picture

The most noticeable aspect of GLOB's fundamental report is its valuation score of 8 out of 10. This result suggests the stock is trading at prices viewed as very appealing compared to both its sector and the wider market. For an investor focused on value, this is the main sign that encourages more examination.

- Price-to-Earnings (P/E) Ratio: At 7.84, GLOB's P/E ratio is labeled "very inexpensive." It is lower than 92% of similar firms in the IT Services sector and stands significantly under the S&P 500 average of about 26.2.

- Forward P/E Ratio: The view stays the same looking forward, with a forward P/E of 7.51. This implies the market's low pricing continues even when accounting for expected future earnings.

- Other Measures: The firm's Enterprise Value to EBITDA and Price to Free Cash Flow ratios also indicate underpricing, rating lower than 91% and 83% of sector rivals, in turn.

This grouped data on valuation measures is important because it spots a possible difference between GLOB's market price and its estimated real value, the basic idea of value investing.

Balanced Fundamentals Bolster the Idea

A low price by itself is insufficient; it needs to be backed by acceptable core business operations to steer clear of weak investment situations. GLOB's report displays even, medium-level results in the other main categories, pointing to a steady operational foundation.

Financial Condition (Score: 5/10) The firm's financial condition score of 5 shows a middle, steady stance. Important details consist of:

- A firm balance sheet with a good Debt-to-Equity ratio of 0.20.

- A strong Debt-to-Free Cash Flow ratio of 2.24, indicating it would need just over two years of present cash flow to clear all debt, a measure that beats 70% of its sector.

- Sufficient liquidity, with Current and Quick Ratios of 1.64, hinting at no near-term payment issues.

For a value investor, an acceptable condition score is essential. It offers the "margin of safety" by confirming the firm is not carrying too much debt and can survive economic challenges while the market may reassess its value.

Earnings (Score: 5/10) GLOB's earnings are also scored a middle 5. The firm is reliably profitable with positive income and cash flow over the last five years. Its margins are typically similar to or above sector norms:

- An Operating Margin of 10.29% is better than 72% of similar firms.

- Return on Invested Capital (ROIC) of 7.15% exceeds 67% of the sector.

While not extraordinarily high, these measures show the firm's capacity to turn sales into profit, a central element in finally creating shareholder value and supporting a higher price over time.

Expansion (Score: 5/10) The expansion story for GLOB is one of a solid past performance moving to more restrained short-term projections.

- Past Expansion: The firm has demonstrated very strong past expansion, with Sales rising at an average yearly rate of 24.7% over recent years.

- Current & Future View: Recent sales expansion has decreased to 1.62%, and future EPS and Sales are projected to increase at a more moderate rate of about 7-8% and 6%, in turn.

This change is probably a major reason for the stock's low price. For a value investor, this situation can be a chance: the market may be too negative about the slowdown, pricing the stock as if no expansion will resume, while the operations indicate a still-sound, though more established, business.

Summary: A Prospect for Value-Focused Holdings

GLOBANT SA presents a situation that fits well with a systematic value-investing filter. It is a firm trading at a notable discount to the market and its industry, as shown by its high valuation score. Significantly, this low price is not combined with financial weakness or an absence of earnings; instead, it is bolstered by middle scores in condition and earnings that signal a stable, ongoing business. The expansion outlook, while slowing from past high rates, stays positive. This mix, a very low price along with acceptable operations, makes GLOB a stock deserving of more detailed research for investors looking for underpriced prospects.

If you want to examine other stocks that match this "acceptable value" picture, you can see more outcomes by using this pre-set stock filter.

Disclaimer: This article is for information only and is not financial guidance, an endorsement, or an offer to buy or sell any security. Investing holds risk, including the possible loss of capital. You should perform your own investigation and talk with a certified financial consultant before making any investment choices.