For investors looking for chances where the market price may not completely show a company's basic strength, a systematic screening process can help find possible candidates. One such method is to look for stocks that show an attractive valuation while keeping good fundamental condition, earnings, and expansion. This approach matches central value investing ideas, which concentrate on finding good businesses selling for less than their calculated worth. The aim is to steer clear of "value traps", cheap stocks for a cause, by making sure the company is financially stable and able to produce earnings.

FRONTDOOR INC (NASDAQ:FTDR) recently appeared from a "Decent Value" screen using this thinking. The screen selected for companies with a good valuation rating, along with satisfactory results in earnings, financial condition, and expansion. Frontdoor, the owner of home service plan brands such as American Home Shield, seems to match this description, justifying a more detailed examination of its finances.

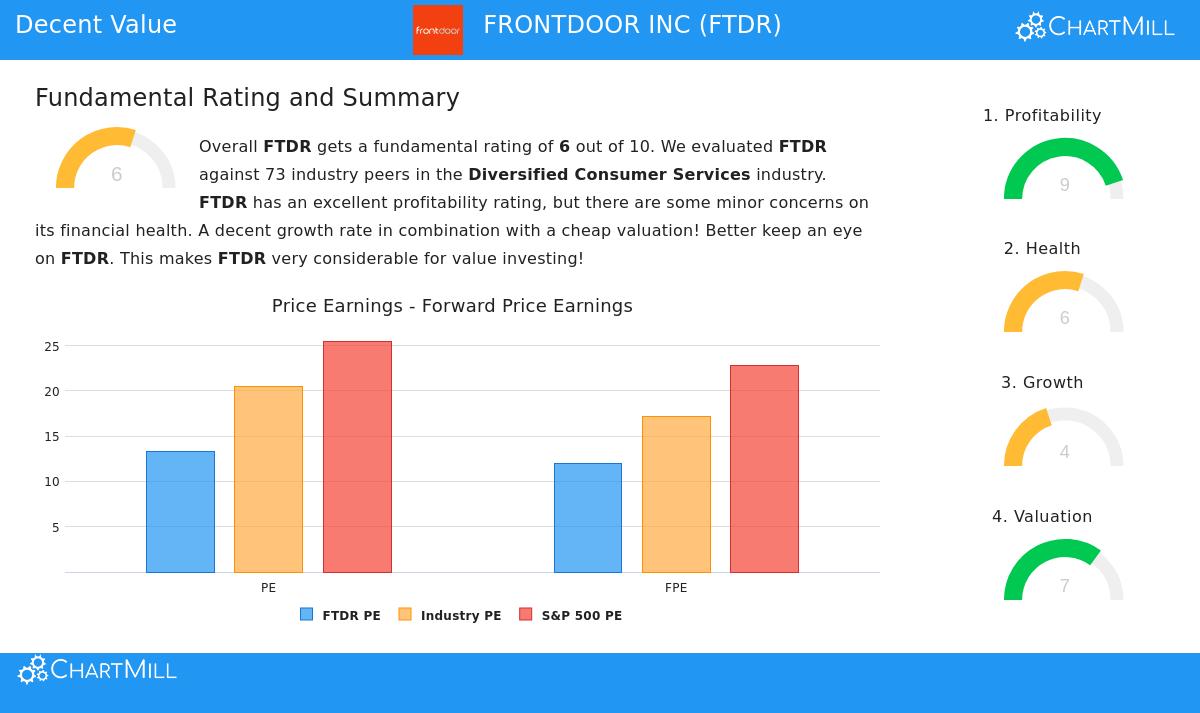

Valuation: Trading for Less

The most noticeable part of Frontdoor's present situation is its valuation, which gets a 7 out of 10 in ChartMill's study. In a market where the S&P 500 sells at an average Price-to-Earnings (P/E) ratio over 25, FTDR's P/E of 13.36 appears as much less expensive. This lower price is even more clear within its own field.

- P/E Ratio: At 13.36, FTDR is priced lower than about 77% of similar companies in the Diversified Consumer Services field.

- Forward P/E Ratio: Looking forward, the view stays positive. With a forward P/E of 11.94, the company is less expensive than around 85% of its field rivals and rests far below the S&P 500 average.

- Cash Flow & EBITDA: The value idea goes past earnings. FTDR's Price-to-Free Cash Flow and Enterprise Value-to-EBITDA ratios also point to a "rather inexpensive" valuation compared to most of its field peers.

For a value investor, these numbers imply the market might be pricing Frontdoor's earnings and cash flow creation too low. The company's very good earnings, covered next, further back the idea that its current price may not completely represent its financial results.

Profitability: A Central Positive

A low price is only interesting if the business is basically sound. This is where Frontdoor does very well, having a ChartMill Profitability rating of 9 out of 10. The company shows a notable skill to turn revenue into profit, a key element for continuing operations and supporting future expansion without too much debt.

- High Returns: The company provides better returns on capital. Its Return on Invested Capital (ROIC) of 18.6% and Return on Equity (ROE) of over 105% do better than more than 93% and 97% of field peers, in order. This shows very effective use of investor capital.

- Strong and Improving Margins: Frontdoor keeps good margins. An Operating Margin of 20.44% puts it in the top part of its field, and both its Operating and Gross Margins have shown upward movements in recent years.

This steady and high-level earnings provides a safety buffer. It suggests the business has a lasting competitive edge and price strength in the home warranty sector, lowering the chance that its low valuation signals a lasting drop.

Financial Health: A Varied but Acceptable View

Financial condition is the support that holds a company up during economic changes. Frontdoor gets a Health rating of 6, pointing to a mostly stable position with some points to watch. The study confirms the company is building value, as its ROIC is well above its cost of capital.

- Good Signs: The company has been lowering its share count, which can help per-share numbers, and its Altman-Z score of 3.49 suggests a small short-term chance of financial trouble. Its Debt-to-Free Cash Flow ratio of 3.01 is also seen as positive.

- Debt Point: The main point for care is a somewhat high Debt-to-Equity ratio of 4.73, which shows a large use of debt financing. Still, this is balanced by the company's good and steady cash flow from operations, which gives the ability to handle this debt. Liquidity ratios, like the Current and Quick ratios, are at satisfactory levels.

For value investors, a good health score helps remove companies weighed down by balance sheet dangers. While FTDR's debt level is high, its very good earnings and cash flow creation seem to handle this danger well for now.

Growth: A Satisfactory Past Performance

The Growth part, rated a 4, shows a detailed story. It stresses the need to look past one number to grasp a company's path.

- Past Results: Frontdoor has provided good past expansion, with Earnings Per Share (EPS) growing over 21% in the last year and on a yearly basis over several years. Revenue expansion has also been positive.

- Future Predictions: Analyst forecasts point to a possible reduction in pace. Estimates suggest a drop in EPS expansion and more limited revenue growth in the next years. This expected slowing is probably a main element in the stock's low valuation.

From a value view, the screen's need for "satisfactory" expansion is fulfilled by the company's shown past skill to grow profitably. The future estimates bring caution but do not cancel the company's set operational strength. The value case here may depend on the company's skill to match or beat these lowered expectations.

Final Thoughts and Next Steps

Frontdoor Inc. shows an example of the "decent value" screening method. It sells at prices much under both the wider market and its field, yet it is supported by excellent earnings numbers, acceptable financial condition, and a past of good expansion. This mix tries to meet a central rule of value investing: looking for a safety buffer by buying a competent business for less than it seems to be worth.

A full list of these fundamental ratings is found in the complete Frontdoor fundamental analysis report.

Investors curious about finding other companies that match this profile of good valuation combined with stable fundamentals can locate more possible candidates using the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or a deal or request to buy or sell any securities. The study is based on data and ratings from ChartMill, and investors should do their own research and talk with a qualified financial advisor before making any investment choices. Past results do not show future outcomes.