Fortuna Mining Corp (NYSE:FSM) has surfaced as a potential candidate for investors following the Peter Lynch approach to stock selection, a strategy that seeks growing companies trading at reasonable valuations. In his book One Up on Wall Street, Lynch advocated for a long-term, buy-and-hold strategy focused on fundamentally sound businesses with sustainable earnings growth, low debt, and strong profitability. The idea is to avoid chasing high-flying stocks with unsustainable momentum and instead find companies that offer a blend of growth and value, often referred to as GARP (Growth at a Reasonable Price). The screen used here applies Lynch’s core criteria: EPS growth between 15% and 30% over five years, a PEG ratio below 1, a debt-to-equity ratio under 0.6, a current ratio above 1, and return on equity exceeding 15%.

Recent Performance and Growth Metrics

Fortuna Mining Corp (FSM) shows a growth profile that fits well with Lynch’s philosophy of sustainable expansion. The company has delivered an impressive 28.47% average annual EPS growth over the past five years, which falls within the sweet spot of 15% to 30% that Lynch identified as ideal. This rate avoids the dangerously high growth levels that often prove unsustainable. Revenue growth over the same period has averaged 27.69% annually, further indicating a business that has been scaling effectively.

Looking ahead, analysts project EPS growth of 39.50% annually over the next few years, while revenue growth is expected to slow to around 2.98% per year. This suggests that the company is becoming more profitable as it matures, which is a positive signal for long-term investors. The PEG ratio based on past five-year earnings is 0.63, well below Lynch’s threshold of 1. This metric compensates for growth, meaning investors are paying a reasonable price relative to the company’s historical earnings expansion—a key aspect of Lynch’s GARP approach.

Valuation Metrics

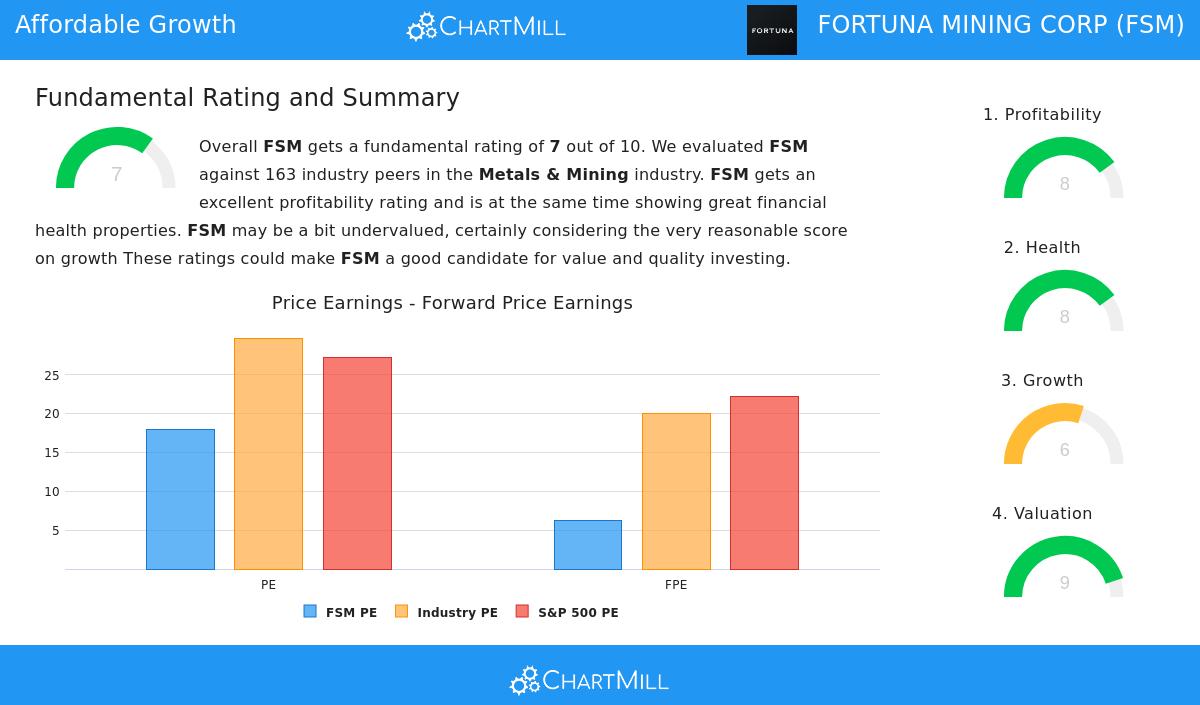

FSM’s valuation picture is attractive. The trailing P/E ratio of 17.98 is slightly above the industry average, but the forward P/E ratio of just 6.24 suggests that future earnings growth is not yet fully priced in. When compared to the S&P 500’s forward P/E of roughly 22, FSM appears much cheaper. The enterprise value to EBITDA ratio is also low relative to industry peers—FSM is cheaper than 95.71% of companies in the metals and mining sector. Similarly, the price-to-free-cash-flow ratio ranks among the most attractive in its peer group. These multiples indicate that the market may not be fully recognizing the company’s earnings potential, which is exactly the kind of mispricing Lynch encouraged investors to exploit.

Financial Health and Profitability

Lynch placed heavy emphasis on financial strength, and FSM delivers on that front. The debt-to-equity ratio is just 0.11, well below the 0.6 maximum set by the screen (and even below Lynch’s personal preference of 0.25). This low leverage means the company funds its operations primarily through equity, reducing financial risk. The current ratio of 2.98—far above the required 1.0—shows that FSM has ample liquidity to cover short-term obligations. Meanwhile, return on equity (ROE) is 17.14%, exceeding the 15% threshold and signaling efficient use of shareholder capital.

Beyond these screen criteria, FSM scores strongly on other measures of profitability. Its profit margin of 27.58% and operating margin of 37.15% rank among the best in the metals and mining industry. Return on assets (ROA) and return on invested capital (ROIC) also outperform at least 82% of peers. The company’s Altman-Z score of 4.24 indicates a very low risk of bankruptcy, while the debt-to-free-cash-flow ratio of 0.73 suggests it could pay off all its debts in less than a year. These factors provide a solid foundation for long-term growth.

Fundamental Report Summary

Our detailed fundamental analysis assigns Fortuna Mining Corp a rating of 7 out of 10, placing it in strong standing among its industry peers. The highest marks come from valuation (9/10) and profitability (8/10), with health also scoring an 8/10. Growth scores a respectable 6/10, reflecting solid past performance and strong future expectations. The full breakdown of these ratings, including detailed comparisons to industry peers, can be explored in the fundamental report.

Analyst Views and Concluding Thoughts

The combination of low leverage, high profitability, reasonable valuation multiples, and sustainable growth rates makes Fortuna Mining Corp a textbook GARP candidate. Peter Lynch famously advised investors to look for companies that were "boring" and underfollowed—businesses with solid fundamentals that had yet to catch Wall Street’s attention. While FSM operates in the metals and mining sector, which has its own cycles, the company’s financial discipline and growth trajectory align closely with Lynch’s principles.

If this screen has piqued your interest, click here to explore more stocks that meet the Peter Lynch criteria and build your own long-term portfolio.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always conduct your own research before making any investment decisions.