For investors aiming to assemble a collection of lasting, high-standard businesses, the ideas of quality investing present a useful structure. This method centers on finding companies with durable competitive strengths, sound financial condition, and the capacity to produce steady, high returns on capital over many years. One organized way to discover these companies is the "Caviar Cruise" stock screen, which selects for firms with better past revenue and profit increases, high returns on invested capital, strong free cash flow production, and acceptable debt amounts. The aim is not to locate temporary discounts, but to identify businesses of such fundamental quality that an investor would be at ease holding them for a long time.

A recent use of this screen has identified FactSet Research Systems Inc. (NYSE:FDS) as a possible candidate for more detailed review by investors focused on quality. The financial data and analytics provider seems to satisfy many of the strategy's central quantitative standards, pointing to a business established on a base of economic soundness.

Satisfying the Central Quality Standards

The Caviar Cruise method establishes demanding targets across many financial measures. FactSet's reported numbers show it meets these targets comfortably in several important areas.

- Better Profitability and Capital Use: A central idea of quality investing is a high Return on Invested Capital (ROIC), which gauges how well a company produces profits from its capital foundation. FactSet's ROIC (leaving out cash, goodwill, and intangibles) is a notable 241.1%, greatly above the screen's lowest limit of 15%. This shows a business model needing little capital that creates very large profits compared to the capital needed to operate it, a clear marker of a wide economic moat.

- Solid and Gaining Operational Growth: The screen demands both 5-year revenue and EBIT (earnings before interest and taxes) growth to be above 5%. FactSet exceeds this, with a revenue CAGR of 5.3% and a stronger EBIT CAGR of 11.2%. Importantly, EBIT growth rising faster than revenue growth, as seen here, shows gains in operational effectiveness and possible pricing strength, as the company changes more of each extra dollar of sales into profit.

- Notable Cash Flow and Financial Condition: Quality companies transform accounting profits into actual cash. FactSet's average Profit Quality over five years is 117.8%, meaning its free cash flow has been greater than its net income. This extra cash gives significant strategic freedom. Also, its Debt-to-Free Cash Flow ratio of about 2.0 is much lower than the screen's maximum of 5, showing it could clear all its debt with only two years of present cash flow, indicating a very sound balance sheet.

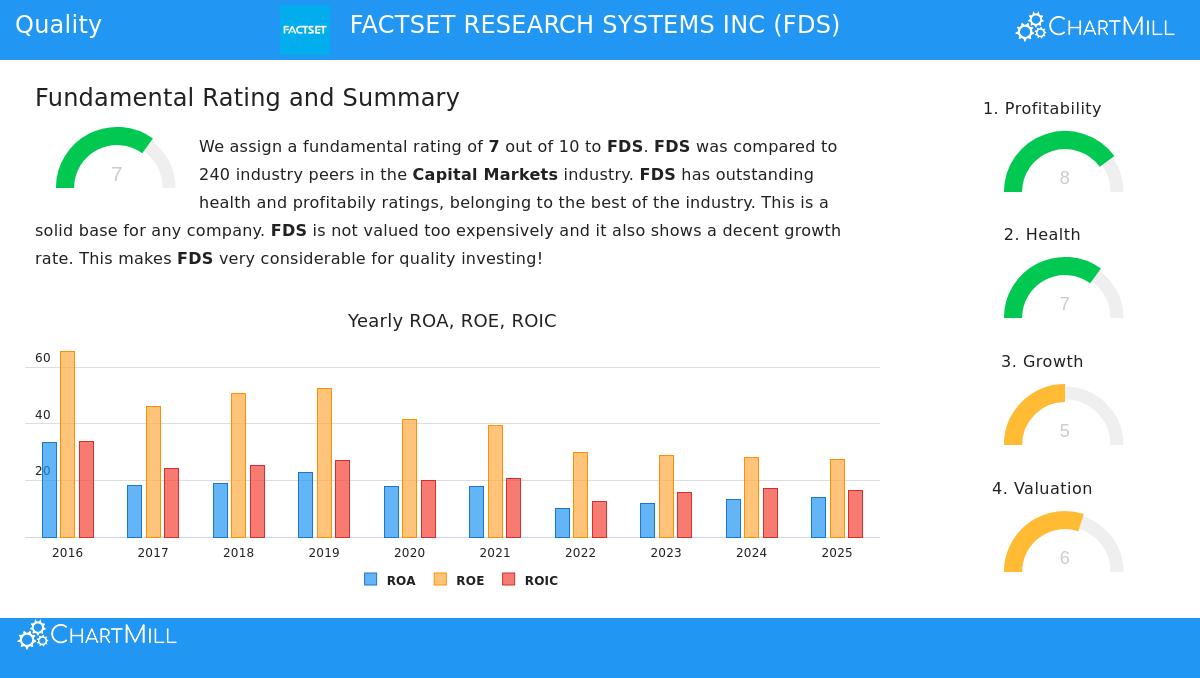

A Broad Fundamental Viewpoint

An examination of FactSet's wider fundamental analysis report supports the image created by the screen-specific measures. The company receives an overall fundamental rating of 7 out of 10, with specific soundness in profitability (score of 8) and financial condition (score of 7).

- Profitability Leader: FactSet's profitability measures are regularly high-grade within the Capital Markets industry. Its Return on Equity of 27.6% and Operating Margin of 31.2% do better than a large portion of its competitors. The report observes that both its Operating Margin and ROIC have displayed upward trends in recent years.

- Stable Financial Base: The company's solvency is strong, with an Altman-Z score showing low bankruptcy danger and a Debt-to-FCF ratio that is higher than 84% of industry rivals. Its record of steady share buybacks further highlights management's dedication to effective capital use.

- Fair Valuation Considered: While not the main concern of strict quality investing, valuation remains relevant. FactSet trades at a Price-to-Earnings ratio of 13.4, which is seen as a fair valuation compared to its own past and is lower than the wider S&P 500 average. Its forward P/E and Enterprise Value/EBITDA ratios are considered low compared to its industry peers, possibly giving a sensible entry price for a business of this standard.

You can examine the complete specifics of this analysis through the detailed fundamental report for FDS.

Why These Standards Are Important for the Long-Term Investor

The particular filters of the Caviar Cruise screen are not random; they are made to separate businesses able to increase value over many years. A very high ROIC indicates a lasting competitive edge that is hard for competitors to weaken. Steady revenue growth combined with widening profit margins shows a needed product in a developing market and capable management. Finally, excellent free cash flow conversion and little debt supply the means for ongoing innovation, strategic purchases, and shareholder rewards through dividends and buybacks, all without depending on uncertain outside funding. FactSet's results across these measures suggest it has this kind of stable, self-supporting business model.

For investors wanting to investigate other companies that satisfy similar strict quality tests, the Caviar Cruise screen can be a useful beginning for more study. You can see the present screen standards and outcomes by going to the Caviar Cruise stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The data presented is based on publicly available information and specific screening methodologies. Investors should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.