For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy offers a solid middle path. This method tries to find companies that are showing good and lasting expansion, but whose shares are not valued at extreme levels that assume all future success. It sidesteps the speculative rush of high-priced, unprofitable growth narratives while also avoiding stagnant value stocks. By looking for stocks with good growth measures, firm underlying profitability, sound finances, and a fair price, investors can create a portfolio ready to gain from business expansion without paying too much for it.

One stock that recently appeared through such a careful screening process is ExlService Holdings Inc (NASDAQ:EXLS). The operations management and analytics company provides data, AI-led, and digital operations services in areas like insurance, healthcare, and banking. A look at its basic profile indicates it fits well with the affordable growth idea.

A Base of Financial Health and Profitability

Before looking at growth and value, it is important to evaluate the company's foundational strength, its financial health and profitability. These are the bases that allow for lasting growth, making sure a company can fund its future without being weighed down by debt or operational problems. ExlService does very well in these areas, receiving high scores in its basic analysis.

-

Financial Health Rating: 9/10. The company shows a very strong balance sheet. Key positives include:

- A very high Altman-Z score of 7.07, showing very low bankruptcy risk and doing better than nearly 90% of its IT Services industry peers.

- A low Debt-to-Free Cash Flow ratio of 1.01, meaning it could pay off all its debt with just over a year's worth of cash flow, a sign of high solvency.

- Strong liquidity, with Current and Quick Ratios of 2.56, easily covering short-term needs.

-

Profitability Rating: 9/10. ExlService is not just growing; it is growing profitably and efficiently.

- Return measures are very good: a Return on Invested Capital (ROIC) of 17.72% and a Return on Equity (ROE) of 27.50% put it in the top group of its industry.

- Margins are sound and improving, with a Profit Margin of 12.02% and an Operating Margin of 15.03%, both showing positive movement over recent years.

This pairing of excellent health and high profitability gives a stable base from which the company can run its growth plan, a necessary condition for a lasting affordable growth candidate.

Showing Good and Steady Growth

The center of the affordable growth strategy is, expectedly, growth. The screen specifically searches for companies showing "good growth," and ExlService meets this with a Growth Rating of 7/10. The company's path is marked by good, steady expansion across important financial measures.

-

Past Performance:

- Revenue increased 13.56% over the last year and has averaged a notable 16.85% yearly growth over recent years.

- Earnings Per Share (EPS) growth is even stronger, up 17.47% in the last year with a very good 22.60% average yearly growth rate in the past.

-

Future Expectations:

- Analysts expect this momentum to keep going, with estimated average yearly EPS growth of 14.57% and revenue growth of 11.89% moving forward.

While the expected growth rates show a slowing from the very high pace of recent years, they remain "quite strong" for an established, profitable company. This shift toward a more lasting, yet still above-average, growth rate is common for maturing growth stories and is exactly what the affordable growth screen tries to find, companies moving from very high growth to steady growth.

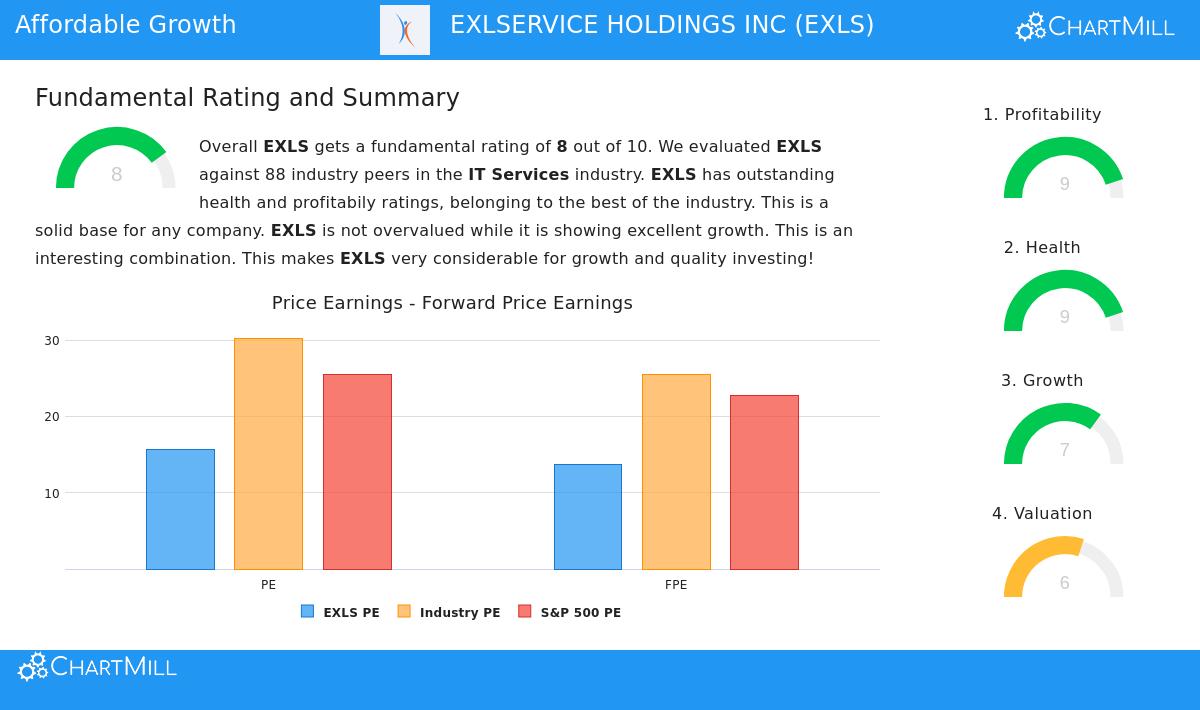

Valuation at a Fair Price

The last, essential part is valuation. A growth stock is only "affordable" if the market has not already accounted for many years of future success. This is where many good companies do not pass the screen. ExlService, however, gets a Valuation Rating of 6/10, showing it is priced at levels that do not seem too high compared to its basics.

-

Fair Multiples: The stock trades at a P/E ratio of 15.62 and a Forward P/E of 13.69.

- These numbers are below both the wider S&P 500 (P/E ~25.5) and the average of its IT Services industry peers (P/E ~30.3).

- Other valuation measures like Enterprise Value/EBITDA and Price/Free Cash Flow are also at levels lower than most industry competitors.

-

Growth Adjustment: The PEG ratio, which changes the P/E for expected earnings growth, suggests the stock is priced fairly. When paired with the company's very good profitability and strong financial health, the current valuation can be viewed as fair, if not appealing, for a business of this quality.

Conclusion

ExlService Holdings Inc presents a solid example for the affordable growth strategy. It is not a speculative wager on future possibility but an investment in a company that is already performing well. Its very good financial health and profitability give it stability, its history and outlook confirm good growth, and its current market price does not require flawless results. This match across all key screening points, growth, profitability, health, and value, makes EXLS a stock worth more study for investors looking for growth without overpaying.

For investors wanting to find other companies that match this careful "Affordable Growth" profile, you can see the full screening results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.