For investors looking for chances where the market price may not completely show a company's actual value, a disciplined screening method can be a helpful first step. One method is to look for companies that seem operationally good but are priced low. This means selecting for stocks with good valuation marks, indicating they are inexpensive compared to earnings, cash flow, or assets, while also making certain they keep acceptable marks in profitability, financial condition, and growth. This mix tries to find possible "value" cases: businesses that are operationally stable and expanding, but whose shares are selling at appealing prices, perhaps because of wider market feeling or industry inattention.

Expand Energy Corp (NASDAQ:EXE), an independent energy company concentrated on natural gas, oil, and natural gas liquids, comes from such a screen. The company, with activities in important U.S. shale areas like the Haynesville and Appalachia basins, shows a profile that calls for more examination from a value point of view. According to ChartMill's fundamental analysis report, EXE gets an overall fundamental rating of 6 out of 10, but its part scores show the particular positives that match a value-focused filter.

Valuation: The Center of the Chance

The main attraction of EXE here is its valuation. The stock gets a firm Valuation rating of 7, which is the main requirement for a value screen. This mark implies the company's shares are priced modestly relative to its financial results and future outlook.

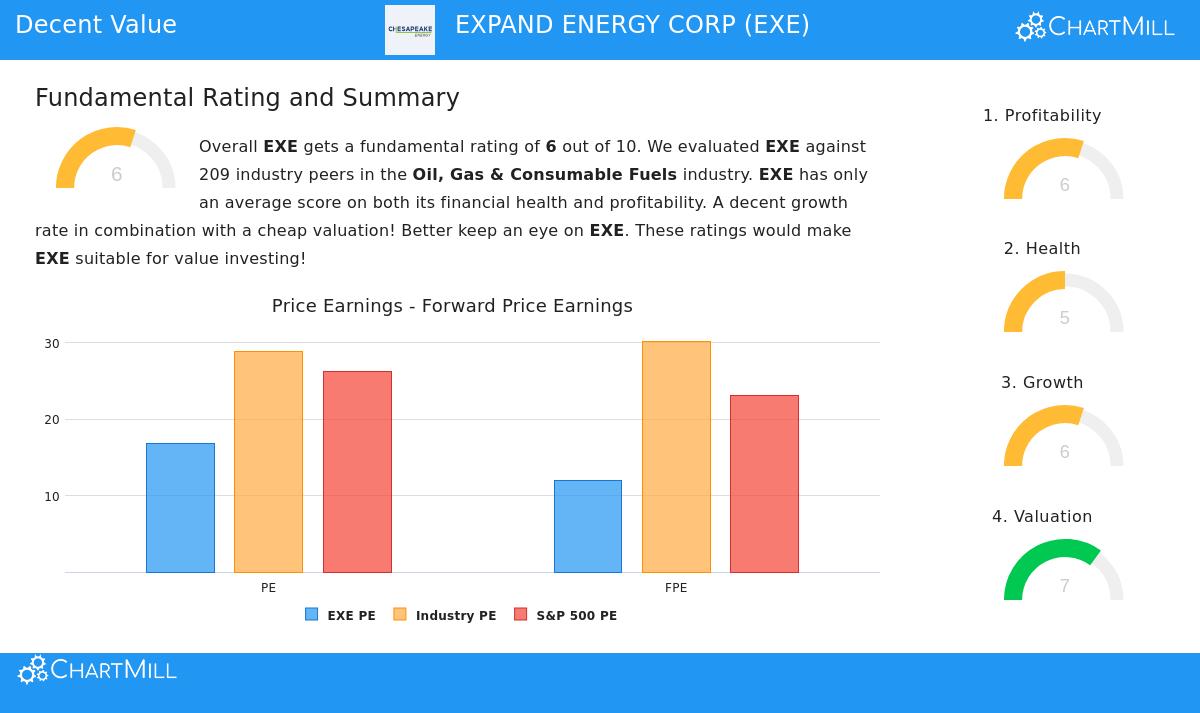

- Appealing Earnings Multiples: EXE's Price-to-Earnings (P/E) ratio of 16.74 is seen as fair on its own and is less expensive than 62% of similar companies in the Oil, Gas & Consumable Fuels industry. More interesting is its forward P/E ratio of 11.91, which is lower than over 80% of industry rivals and rests notably below the present S&P 500 average.

- Cash Flow and EBITDA Valuation: The study shows EXE is valued as less expensive than 83% of the industry based on its Enterprise Value to EBITDA ratio, and less expensive than 71% based on its Price-to-Free Cash Flow ratio.

- Growth Adjustment: The stock's low PEG ratio, which modifies the P/E for anticipated growth, more indicates a possibly low valuation. This is key for value investing, as it implies investors are not paying too much for the company's future growth possibility.

For a value investor, these measures are the base. They look for a notable difference between price and inherent value, and EXE's valuation marks point out several standard measures where such a difference may be present.

Financial Condition and Profitability: Evaluating the Base

An inexpensive stock is only a good investment if the company is operationally stable. This is why screens for value stocks must also look at financial condition and profitability, to steer clear of "value traps" where a low price just shows a weakening business. EXE shows steadiness here, with both Health and Profitability ratings of 5 and 6, in that order.

Financial Condition (Rating: 5) The report mentions an average financial condition score, but important stability measures are good:

- The company keeps a sound Debt-to-Equity ratio of 0.27, which is more favorable than almost 68% of similar companies, showing a careful balance sheet setup.

- Its Debt-to-Free Cash Flow ratio of 3.05 is positive, suggesting it could pay off all its debt in just over three years from its cash flow, a mark of high stability.

- Liquidity measures like the Current and Quick Ratios are near 1.01, considered enough to meet near-term responsibilities.

Profitability (Rating: 6) Operational effectiveness is adequate, with several margins doing better than industry averages:

- EXE has a strong Gross Margin of 73.71%, doing better than 85% of the industry.

- Its Return on Invested Capital (ROIC) of 8.09% is more favorable than 75% of similar companies, showing good use of capital to create earnings.

- While the Profit Margin has dropped lately, it stays at a sound 14.92%, and the Operating Margin has shown good expansion.

These points are vital for the value argument. A positive balance sheet lowers failure risk and gives steadiness, while steady profitability confirms the business model is functional, supporting the idea that the present low valuation may be short-term or not justified.

Growth: The Driver for New Valuation

Value investing is not only about fixed low price; it often includes finding companies where growth can work as a driver for market re-rating. EXE's Growth rating of 6 shows a varied but hopeful view.

- Positive Recent Results: The company reported very strong expansion in the last year, with Revenue up 190.5% and Earnings Per Share increasing 375.8%.

- Good Historical Pattern: On average, Revenue has expanded by over 18% in recent years.

- Future Projections: Analysts think EPS expansion will continue at a rate of 8.6% each year, with Revenue expansion estimated near 7.4%.

This growth outline is significant because it gives a possible way for the market to acknowledge the company's value. If EXE can keep delivering growth while maintaining its profitability and financial condition, the present valuation multiples may increase, leading to share price gains.

Conclusion and More Study

Expand Energy Corp presents a case that fits with several ideas of value investing: it seems priced at a lower level based on normal valuation multiples, yet it functions with adequate profitability, a firm financial base, and a clear growth path. The mix of a high valuation score with acceptable scores in other fundamental areas implies the market may be pricing the company's steady operational results and its place in the energy industry too low.

It is, however, necessary to think about the wider situation. The company functions in the changing energy industry, which is affected by commodity prices. The report itself mentions a slowing in expected revenue expansion. Any complete study should balance these industry-specific risks against the clear valuation chance.

For investors curious about examining similar possible value chances, more stocks that pass this "Decent Value" screen, selecting for good valuation along with acceptable profitability, condition, and growth, can be found via this link.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.