For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish solid dividend payers from risky high-yield stocks. A frequent method uses criteria to find companies that provide a good dividend and also have the fundamental financial capacity to maintain and possibly increase those payments. This usually involves searching for stocks with high dividend ratings, which generally assess yield, growth, and sustainability, while also confirming the company holds satisfactory scores in profitability and financial soundness. This measured method aids in finding businesses that can provide returns to shareholders reliably, across different economic periods.

East West Bancorp Inc. (NASDAQ:EWBC), the parent company of East West Bank, appears as a result from this kind of screening method. The bank, based in Pasadena, California, works in consumer, business, and commercial banking areas, with a specific emphasis on connecting the U.S. and Asia markets. Its choice comes from a fundamental report that notes a good dividend profile backed by sufficient profitability and a firm balance sheet.

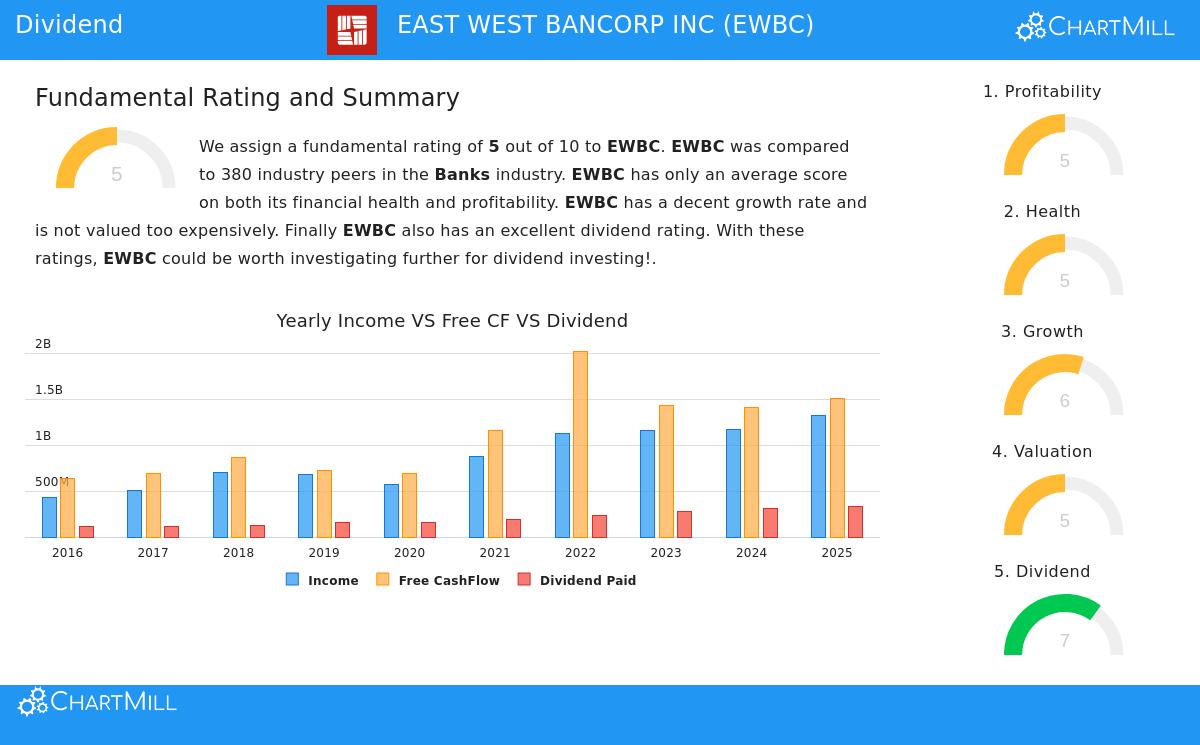

Dividend Profile: A Mix of Yield, Growth, and Dependability

The main attraction for income investors is in EWBC's dividend traits, which receive a rating of 7 out of 10. This rating combines a few important elements that dividend-oriented methods value.

- Good and Maintainable Yield: The stock provides a yearly dividend yield of 3.04%. This is higher than the present S&P 500 average yield of about 1.90% and matches the wider banking industry average. Significantly, the payout ratio is at a low 25.21% of income. This modest ratio is a key sign of sustainability, as it shows the company keeps most of its earnings to fund the business and protect against future slowdowns, lowering the chance of a dividend reduction.

- Strong Growth Record: EWBC has shown a firm dedication to giving more cash to shareholders over time. The dividend has increased at an average yearly rate of 17.11% over the last five years, a pace that greatly exceeds inflation and improves an investor's actual income. Also, the company has paid and, importantly, has not reduced its dividend for at least ten years. This long, dependable history is what builds investor trust in the board's dedication to shareholder returns.

- A Point on Sustainability: The fundamental report does note one area to watch: while the dividend has been increasing quickly, recent earnings growth has been more modest. This difference indicates the present high dividend growth pace might not be maintainable forever without a return to faster profit growth. This highlights why the screen's extra filters for profitability and soundness are important, they help confirm the company has the basic capacity to manage this situation.

Supporting Fundamentals: Profitability and Financial Soundness

A high dividend rating by itself can be incomplete if the company is not on firm footing. This is why the screening rules also demanded minimum ratings for profitability and financial soundness, both areas where EWBC scores a 5.

- Sufficient Profitability: The bank's profitability rating shows a varied but fundamentally acceptable situation. Key positives involve an outstanding Return on Equity (ROE) of 14.89%, which puts it in the best group of its banking competitors, showing efficient use of shareholder capital. Its Profit Margin of 45.20% is also very good for the industry. These numbers indicate that EWBC is a competent earner, producing the profits required to support its dividend.

- Firm Financial Soundness: The soundness rating of 5 indicates a stable balance sheet, essential for a financial institution. A notable metric is the Debt to Free Cash Flow ratio of 0.02, which is very good and shows it would take a minimal time for the company's cash flow to repay all its debts. Also, it holds no debt on an equity basis (Debt/Equity ratio of 0.00), making it much less reliant on debt financing than many competitors. This good solvency position gives a key safety margin, ensuring the company can fulfill its duties and keep its dividend even in a difficult economic setting.

Valuation and Growth Setting

From a valuation viewpoint, EWBC seems fairly priced, which strengthens the investment argument. With a Price/Earnings (P/E) ratio of 11.16 and a Forward P/E of 10.12, the stock is valued lower than the wider S&P 500 and matches its industry. This suggests the market is not overvaluing its earnings or dividend stream. Regarding growth, the company has a good recent history, with EPS growing over 19% on average each year in recent times. While future EPS growth is predicted to slow, revenue growth is forecast to stay acceptable at almost 11%, giving a stable base.

For a complete summary of all these metrics, you can examine the full ChartMill Fundamental Analysis Report for EWBC.

Conclusion

East West Bancorp Inc. offers a strong argument for dividend investors using a measured screening method. It provides a yield that is good compared to the market, supported by a ten-year history of dependable and fast-growing payments. The sustainability of this dividend is backed by a low payout ratio and, importantly, by the company's acceptable profitability and very good, low-debt balance sheet. While investors should note the possibility for dividend growth to match earnings growth more closely going forward, the basic requirements of satisfactory soundness and profitability give important confidence.

This review of EWBC came from a methodical screen for quality dividend payers. If you want to examine other companies that fit similar standards of high dividend ratings along with satisfactory financial soundness and profitability, you can use the "Best Dividend Stocks" screen yourself here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data and ratings provided by ChartMill, which evaluates past and current fundamentals. Investors should conduct their own thorough research and consider their individual financial situation and risk tolerance before making any investment decisions. Past performance is not indicative of future results.