Value investors are constantly searching for companies whose stock price doesn't fully reflect their underlying business strength. The core idea, rooted in the principles of Benjamin Graham, is to buy a dollar’s worth of assets for 50 cents. One way to systematically find these opportunities is by using a "Decent Value" screen. This approach filters for stocks that score highly on valuation—typically a score of 7 or above on ChartMill’s 10-point scale—while maintaining acceptable ratings for profitability, financial health, and growth. The logic is straightforward: a low valuation alone can be a "value trap," but when combined with solid fundamentals, it often points to a genuine bargain. Using this methodology, Brinker International Inc ( NYSE:EAT ) has emerged as a candidate worth a closer look.

Valuation Metrics

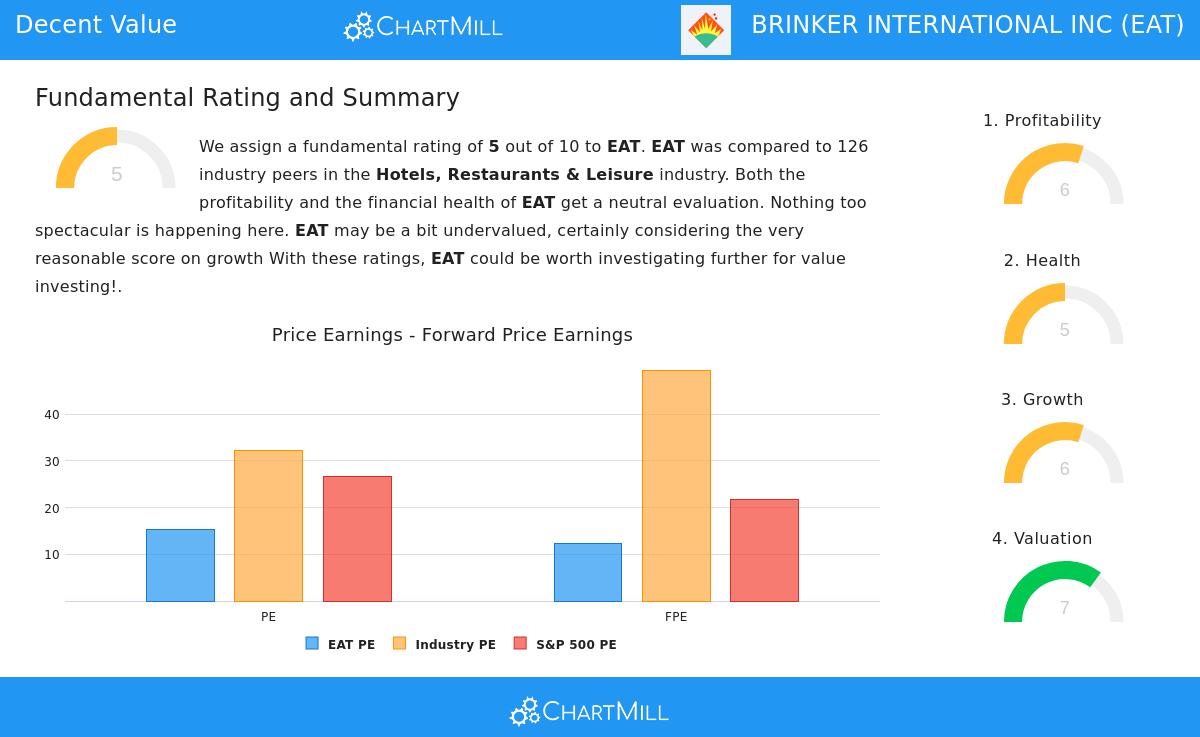

The most convincing argument for EAT as a value play lies in its valuation scores. According to the fundamental analysis report, the company earns a strong Valuation rating of 7 out of 10, which is the key filter in our value screen.

- Price/Earnings (P/E) Ratio: At 15.30, EAT's P/E is significantly cheaper than 79.37% of its industry peers in the Hotels, Restaurants & Leisure sector. It also trades well below the S&P 500 average P/E of 26.77.

- Price/Forward Earnings: Looking ahead, the forward P/E of 12.23 is even more attractive, making EAT cheaper than 84.13% of its industry peers.

- Price/Free Cash Flow: On a cash flow basis, 82.54% of companies in the same industry are more expensive than EAT. This is a critical metric for value investors, as free cash flow represents the money a company can actually reinvest or return to shareholders.

- PEG Ratio: The low PEG ratio (which accounts for expected earnings growth) further supports the idea that the market is not pricing in EAT's future potential.

For a value investor, these numbers suggest the market is assigning a discount to EAT, potentially overlooking its earnings capacity. The "Margin of Safety" concept is at play here: buying at these multiples provides a buffer against unforeseen economic headwinds or calculation errors.

Profitability and Health

A low valuation only matters if the company is financially sound. EAT’s fundamentals suggest it is, though with some caveats that warrant attention.

- Profitability Rating (6/10): The company demonstrates strong return metrics. EAT has a Return on Equity (ROE) of 88.25% and a Return on Invested Capital (ROIC) of 16.80%, outperforming over 85% of its industry peers. These high returns indicate the company is efficient at turning investor capital into profit. The profit margin of 7.83% is also above average for the industry. However, the report notes that margins have been declining recently, which is a trend value investors must monitor.

- Health Rating (5/10): The picture is mixed. On the positive side, EAT has a solid Altman-Z score of 3.79, indicating a very low risk of bankruptcy. Its Debt to Free Cash Flow ratio of 1.05 is excellent, meaning it could theoretically pay off all its debt in just over a year using its cash flow. The main concern is liquidity: the current ratio of 0.36 and quick ratio of 0.31 are low, signaling potential short-term obligation issues. However, for the long-term value investor, the strong cash flow generation and solvency profile often outweigh a tight current ratio.

Growth Prospects

For the "Decent Value" screen to work, a stock needs more than just a cheap price—it needs a catalyst. Growth is that catalyst.

- Growth Rating (6/10): EAT shows an outstanding near-term track record. Earnings Per Share (EPS) grew by an impressive 50.76% over the past year, while revenue surged by 65.25%. This growth is a primary reason why the company can maintain profitability despite its leverage.

- Future Expectations: Analysts expect EPS to grow at an average rate of 14.66% per year in the coming years. When you compare this growth rate to the current P/E of 15.30, the stock looks reasonably priced. The report also notes that revenue growth is expected to accelerate, which is a healthy sign for a restaurant chain in a competitive environment.

The combination of past momentum and forward-looking estimates suggests that EAT is not a stagnant value trap but a company that is actively growing its earnings base, which should eventually support a higher stock price.

Analyst Views

While we do not have specific analyst price targets in this report, the fundamental data itself provides a strong narrative. The fact that EAT scores a 7 on valuation but only a 5 on health indicates that the market is pricing in some risk related to its balance sheet liquidity. The key question for value investors is whether the strong cash flow and growth prospects adequately compensate for that risk. Given the high ROIC and low bankruptcy risk, many would argue that they do.

Finding More Value Opportunities

The "Decent Value" screen is an effective tool for cutting through the noise of the market. It systematically identifies companies like EAT that combine a cheap valuation with solid underlying business fundamentals. To find more stocks that fit this profile, you can run the same screen yourself.

Click here to access the live "Decent Value Stock" screen and see the latest results.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Investing in the stock market involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.