For investors looking for chances in the market, a disciplined method often produces the best outcomes. One method is value investing, a plan that involves finding companies trading for less than their real worth. The aim is to find stocks the market has missed or priced too low, offering a possible safety buffer and space for the price to rise as the difference between price and worth adjusts with time. A useful way to search for these chances is by using fundamental ratings that check important parts like valuation, financial condition, earnings, and expansion. A stock that rates well on valuation while keeping acceptable ratings in the other key parts can be a strong candidate for more study.

Brinker International Inc (NYSE:EAT), the parent company of the Chili’s Grill & Bar and Maggiano’s Little Italy restaurant chains, recently appeared from such a search process. The company, which runs and franchises over 1,600 locations worldwide, offers an interesting example when examined through fundamental measures. A full fundamental analysis report gives an organized view of its financial position.

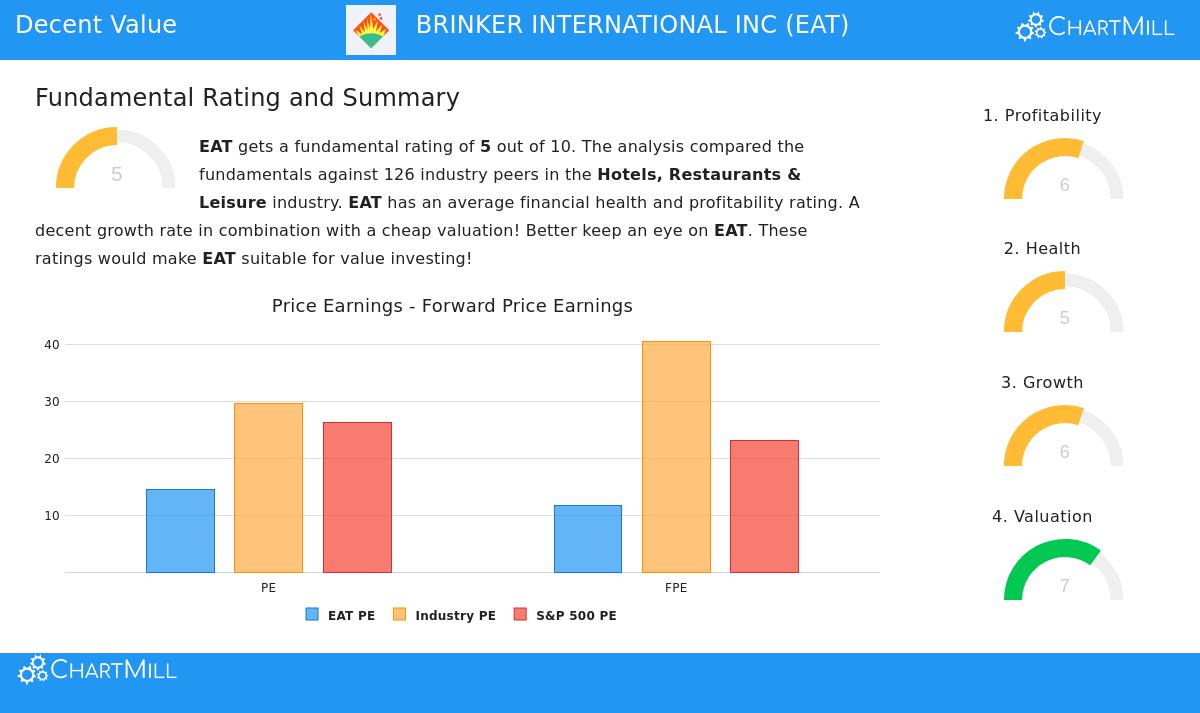

Valuation: The Heart of the Chance

The main draw for a value investor is a good valuation, and EAT gets a 7 out of 10 in this group. The numbers indicate the stock is trading at a lower price compared to both its industry and the wider market.

- Price-to-Earnings (P/E) Ratio: At 14.54, EAT's P/E ratio is seen as reasonable. More significantly, it is less expensive than almost 80% of similar companies in the Hotels, Restaurants & Leisure industry, which has an average P/E of 29.57. It also trades at a notable discount to the S&P 500's current average of 26.17.

- Forward P/E Ratio: The view becomes even stronger looking forward. With a forward P/E of 11.63, EAT is priced lower than over 82% of its industry rivals and much below the S&P 500's forward average of 23.05.

- Price-to-Free Cash Flow: This ratio, which compares the share price to the company's free cash flow production, is also positive. EAT is less expensive on this measure than about 84% of its industry peers.

For a value plan, a low valuation is the starting place. It means the market is pricing the company cautiously, possibly because of near-term worries or industry-wide challenges, creating a possible opening if the core business stays healthy.

Financial Health: A Varied but Acceptable View

Financial condition is vital for value investors, as a good balance sheet offers stability during economic slowdowns and makes sure the company can pay for its activities. EAT gets a middle-of-the-road health rating of 5. The report points out both clear positives and clear negatives.

- Solvency Positives:

- The company's Altman-Z score of 3.71 shows a low short-term chance of failure and puts it in the better group of its industry.

- Its Debt-to-Free Cash Flow ratio is a very good 1.05, meaning it could in theory pay off all its debt with just over a year's worth of free cash flow, a sign of high solvency that is better than nearly 90% of the industry.

- Liquidity Points to Watch:

- The main area for care is liquidity. EAT's Current Ratio of 0.36 and Quick Ratio of 0.31 are poor, suggesting it may have issues meeting immediate bills without depending on operational cash flow or new financing. These ratios are some of the lowest in its field.

While the liquidity numbers deserve notice, the good solvency scores and notable ability to produce cash compared to its debt offer a balance. For a value investor, the point is deciding if the strong cash production can reliably handle the tighter liquidity situation.

Profitability: Producing Good Earnings

A company must earn money to finally support a higher valuation. EAT receives a profitability rating of 6, with several notable numbers that show effective use of money.

- Return Measures: The company has very good returns on capital. Its Return on Equity (ROE) of 88.25% and Return on Invested Capital (ROIC) of 16.80% are in the better group of the industry, beating 95% and 86% of peers, in order. An ROIC that is higher than its cost of capital confirms the company is building real value for shareholders.

- Margin Results: The Profit Margin of 7.83% is better than many rivals. However, the Gross Margin of 18.43% is fairly low for the industry, showing the high-cost reality of the restaurant business. It is worth noting that the Gross Margin has been getting better lately.

Strong profitability is a required part of a lasting value investment. High returns on capital suggest a capable management team and a business model with a lasting edge, which supports the idea that current low pricing may be short-term.

Growth: A Account of Comeback and Forecast

Growth supplies the reason for a value stock's price change. EAT's growth rating is a 6, marked by a strong recent comeback and average future forecasts.

- Past Growth: The last year shows fast growth, with Earnings Per Share (EPS) up 50.8% and Revenue up 65.3%. It is key to remember this comes after a time of major pandemic-related trouble, representing a good recovery.

- Future View: Experts think this speed will continue at a more usual, yet steady, rate. EPS is predicted to grow almost 15% each year in the next few years, with Revenue expected to grow about 6%.

For the value investor, believable future growth is necessary. It connects a low-priced stock now and a fairly priced stock later. EAT's expected mid-teens EPS growth, when paired with its low valuation multiples, leads to a good PEG ratio, further highlighting the possible value case.

Conclusion

Brinker International Inc presents a picture that matches several key value investing ideas. It trades at a clear discount to its industry and the market, has strong profitability and solvency numbers that show a basically healthy business, and is expected to deliver good earnings growth. While investors must thoughtfully review the company's liquidity position and the changing nature of the restaurant industry, the mix of low valuation and acceptable fundamentals makes EAT a stock deserving of more careful review for those using a value-focused plan.

This study of EAT was found using a search method centered on valuation and fundamental soundness. If you are curious about finding other stocks that match a similar "Decent Value" description, you can review the pre-set search here.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and talk with a qualified financial advisor before making any investment choices.