For investors using a classic value strategy, the aim is simple: find companies trading below their inherent value. This requires a methodical hunt for stocks where the market price does not match the basic business facts, offering a possible "margin of safety." A useful first step is to look for companies with good financial condition and earnings, along with good expansion possibilities, all while being priced at a moderate level. One stock that recently appeared from such a "Decent Value" screen is Brinker International Inc (NYSE:EAT), the owner of the Chili’s Grill & Bar and Maggiano’s Little Italy restaurant chains.

A Look at Valuation

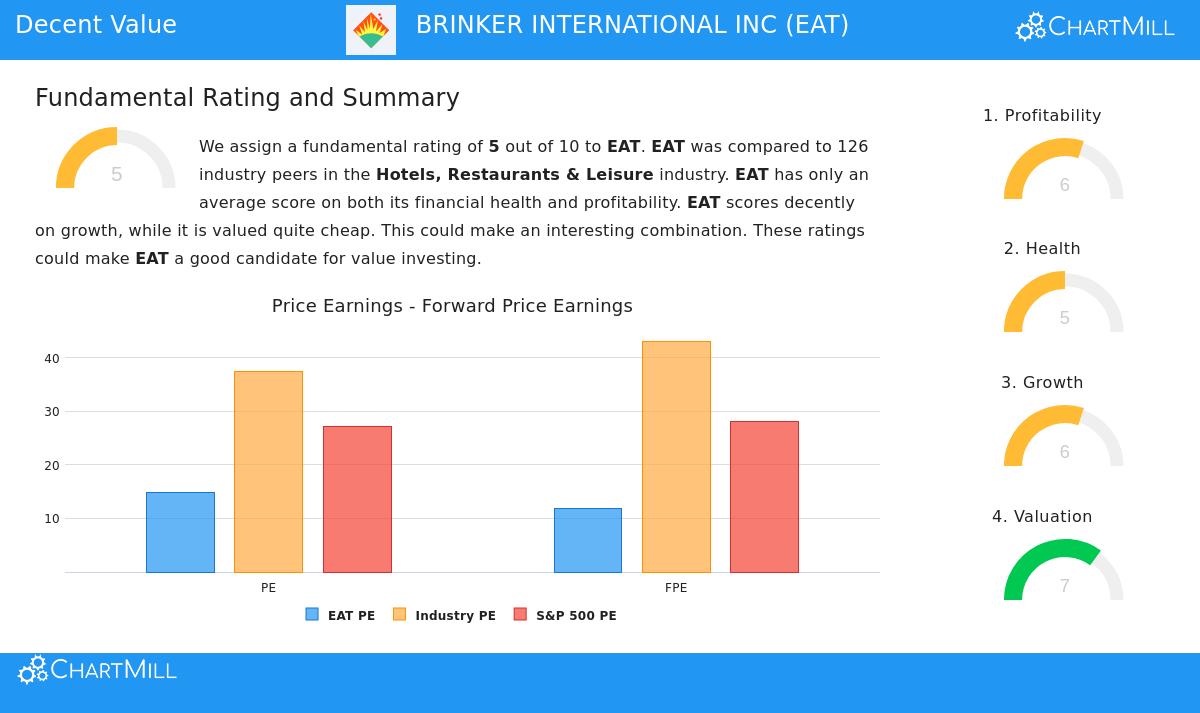

The central idea of value investing is buying assets for less than their value. Brinker International’s present valuation numbers imply the market may be setting a cautious price for the company. Based on ChartMill’s basic analysis, EAT receives a Valuation Rating of 7 out of 10, showing it is placed well next to similar companies.

- Good Earnings Multiples: The stock sells at a Price-to-Earnings (P/E) ratio of 14.89, which is lower than the wider S&P 500 average of 27.10. Significantly, its forward P/E ratio of 11.94 is below about 83% of companies in the Hotels, Restaurants & Leisure industry.

- Good Free Cash Flow Valuation: The Price-to-Free Cash Flow ratio is especially notable, with EAT being priced lower than around 85% of its industry rivals. This number is important for value investors because it points out the real cash-producing capacity of the business compared to its share price.

- Growth Consideration: The low PEG ratio, which changes the P/E for anticipated earnings expansion, adds to the idea that the stock’s price does not completely include its future possibility.

For a value-focused investor, these numbers are the first check, suggesting that the company’s market price may not correspond with its basic earning ability.

Reviewing Financial Condition and Earnings

A low-priced stock is only a worthwhile opportunity if the company is financially stable and able to maintain earnings. A low price can sometimes be a "value trap" if the business is declining. Brinker International’s basic report displays a varied but generally steady situation, with both Health and Profitability Ratings at 5 and 6 out of 10, in that order.

Financial Condition (Rating: 5/10): The company shows clear positives in long-term stability but has short-term cash flow questions.

- Stability Strength: EAT has a very good Altman-Z score of 3.78, showing low near-term bankruptcy danger and doing better than over 83% of the industry. Its Debt-to-Free Cash Flow ratio of 1.05 is very good, meaning it could pay off all its debt with just more than a year of cash flow.

- Cash Flow Note: The main warning is a low Current Ratio and Quick Ratio (both at 0.36), hinting at possible difficulties in meeting immediate debts without depending on operational cash flow. This is a typical feature in the restaurant business because of inventory handling but needs watching.

Earnings (Rating: 6/10): Even with margin pressures usual in the field, Brinker produces good returns on capital.

- Effective Use of Capital: The company has notable returns, with a Return on Equity of 88.25% and a Return on Invested Capital of 16.80%, each performing better than a large majority of industry counterparts. This shows management is efficiently using investor money to produce profits.

- Margin Patterns: While its Profit Margin of 7.83% is higher than the industry middle point, both it and the Operating Margin have fallen in recent years. A good sign is a rising Gross Margin, which hints at some achievement in handling core cost of goods sold.

For a value investor, the good stability and high returns on capital give trust in the business model’s strength, which is necessary when investing with a long-term view.

Looking at the Expansion Path

Value investing does not mean overlooking expansion; lasting expansion is what pushes inherent value up over time. Brinker’s Growth Rating of 6 out of 10 shows a company in a changing stage with good movement.

- Good Recent Results: Over the last year, the company has recorded notable expansion, with Earnings Per Share (EPS) rising 50.76% and Revenue going up 65.25%.

- Future Predictions: Analysts think this good pattern will keep going, with EPS predicted to grow almost 15% each year in the next few years. Revenue expansion is also expected to become positive, with guesses near 6% each year, a clear change from the negative pattern of past years.

- The Overall View: This anticipated return to steady top-line expansion, joined with good bottom-line increase, is key. It implies the company is getting past earlier problems and creating a base for future cash flows, which directly adds to any estimate of inherent value.

Final Points

Brinker International Inc presents a situation that matches several value investing rules. It trades at valuation multiples that are low compared to both the market and its industry, especially on a cash flow basis. The company shows good long-term financial condition and better returns on capital, offsetting short-term cash flow measures. Most significantly, it is not a still business; it is displaying strong recent earnings expansion and is predicted to keep a sound expansion path. This mix of a moderate price, financial steadiness, and expansion chance is exactly what screens like the "Decent Value" filter are made to find.

Investors curious about examining other stocks that fit similar standards of sound valuation, condition, earnings, and expansion can see the complete "Decent Value" screen results here.

,

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer or request to buy or sell any securities. The review is based on given data and shows the author's understanding. Investing includes risk, including the possible loss of original money. You should do your own study and talk with a certified financial consultant before making any investment choices.