For investors looking to balance the search for growth with fiscal care, the "Affordable Growth" or "Growth at a Reasonable Price" (GARP) method presents a viable middle path. This method tries to find companies that are not only growing quickly but are doing so from a place of financial soundness and at a price that does not assume flawless execution. It avoids the high speculation of unprofitable growth stocks while steering clear of the slow progress that can come with deep-value choices. By looking for stocks with good growth scores, firm profitability and financial condition, and a fair price, investors can assemble a portfolio of companies set to increase value over time.

DexCom Inc (NASDAQ:DXCM), a top company in continuous glucose monitoring (CGM) systems, recently appeared from such a search. The company's fundamental picture indicates it represents several main ideas of the affordable growth view.

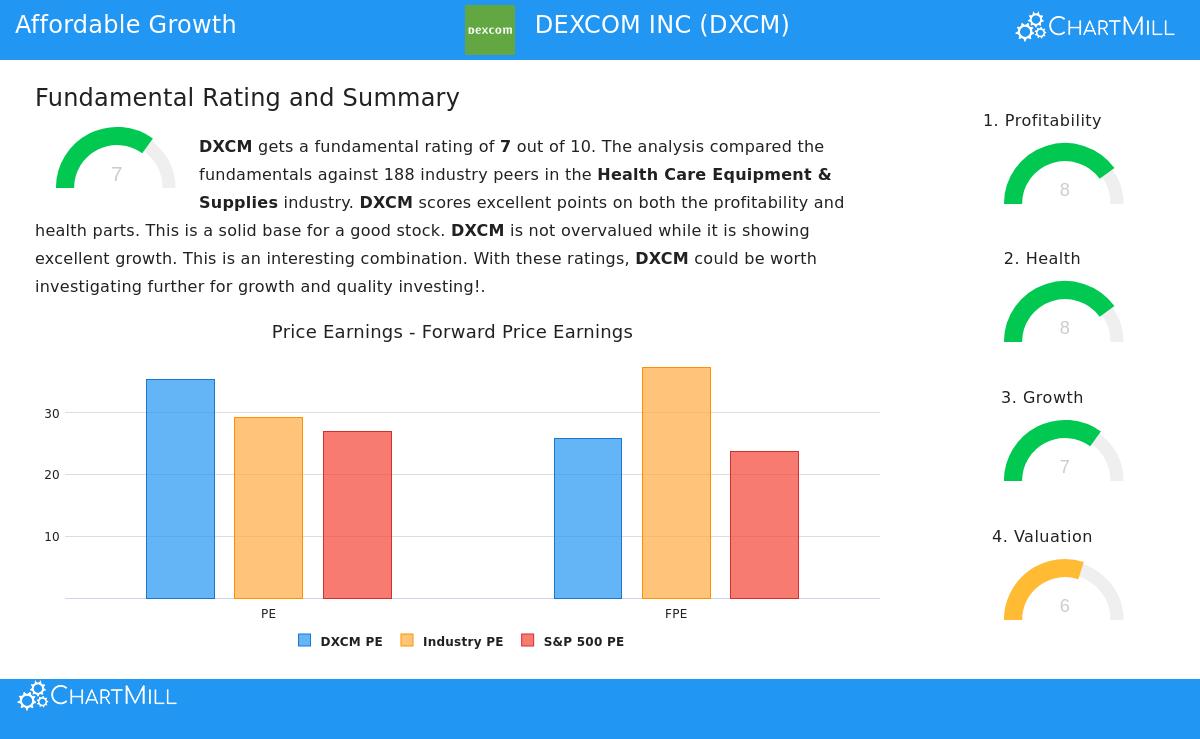

A Base of Strong Growth

The center of any growth investment is, expectedly, growth. DexCom’s past and estimated expansion makes a solid argument. The company has shown a consistent ability to raise both its revenue and profits, a mark of good management in its core diabetes care market.

- Revenue Growth: Over the last year, revenue rose by 15.6%, while the longer-term yearly growth rate is a notable 19.33%. Future estimates project revenue to keep increasing at a rate of almost 12% per year.

- Earnings Growth: This growth is becoming profits. Earnings per share (EPS) increased by 12.73% last year and has a yearly growth rate of 19.29% over recent years. Future EPS growth is estimated to rise to about 21.7% per year.

This steady history and positive forward view are important for the GARP method, as they show the company's growth is lasting and not a temporary event. It is this shown and expected growth that creates the main draw for investors.

Price Consideration

Where DexCom becomes especially notable for the affordable growth investor is in its price setting. On its own, a Price-to-Earnings (P/E) ratio of 35.31 seems high, particularly next to the wider S&P 500 average. However, the GARP process needs looking past simple multiples.

- Industry Comparison: Compared to similar companies in the Health Care Equipment & Supplies industry, DexCom’s price seems more acceptable. Its P/E ratio is below about 71% of its industry rivals.

- Growth Adjustment: Also important, the company’s low PEG ratio—which changes the P/E for estimated earnings growth—hints that the market may not be completely valuing its future growth possibility. This is a central measure for GARP investors.

- Cash Flow View: The price seems even more interesting through other measures. Judged by its Price-to-Free Cash Flow ratio, DexCom is priced lower than around 85% of its industry, showing good cash production relative to its market cost.

This detailed price view—high in simple terms but acceptable or even appealing relative to its growth path and industry—is exactly what the affordable growth search is made to find. It implies the market sees the quality but may not be paying too much for it.

Supported by Soundness and Earnings

Lasting growth cannot stand alone; it must be held up by a good balance sheet and profitable activity. This is where DexCom’s picture makes the investment case stronger. The company receives high scores for both financial condition and earnings, which lowers the risk of the growth narrative.

- Notable Profitability: DexCom’s return figures are excellent. It has a Return on Equity of 30.46% and a Return on Invested Capital of 18.92%, each beating over 95% of its industry peers. Its operating margin of 21.55% is also in the top group of the sector.

- Firm Financial Condition: The company keeps a sound balance sheet. With an Altman-Z score showing no bankruptcy danger and a low debt-to-free-cash-flow ratio of 1.2, DexCom has good financial room. Its debt/equity ratio of 0.47 shows a careful use of borrowing.

These points are not minor for the GARP method; they are necessary. High earnings pay for future growth from within, and a firm financial state ensures the company can manage economic shifts and spend in chances without too much need for outside money. It changes a growth story into a lasting business plan.

Summary

DexCom Inc shows a picture that matches closely with the goals of an affordable growth investor. It combines a good growth path in an important healthcare area with a price that, while not low, seems warranted—and even relatively appealing—when considered next to its industry position and future earnings capacity. Importantly, this growth is supported by a base of notable earnings and a financially good balance sheet, lessening the normal risks of investing in growing companies.

For investors wanting to review other companies that fit similar standards of acceptable growth, fair price, and firm basics, more findings from the "Affordable Growth" search can be seen here. A complete look at DexCom’s fundamental scores is in its full fundamental analysis report.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investors should do their own study and talk with a qualified financial advisor before making any investment choices.