For investors looking for dependable income, a methodical selection process is needed to separate reliable dividend payers from those with uncertain yields. One useful method involves selecting for companies that have both a good dividend score and show firm basic earnings and sound finances. This method tries to find businesses able to maintain and possibly increase their payments over the long term, rather than those with high yields because of a falling stock price. Using a tool set with these conditions, Domino's Pizza Inc (NASDAQ:DPZ) appears as a stock deserving more study for a portfolio focused on dividends.

A Good Dividend Picture

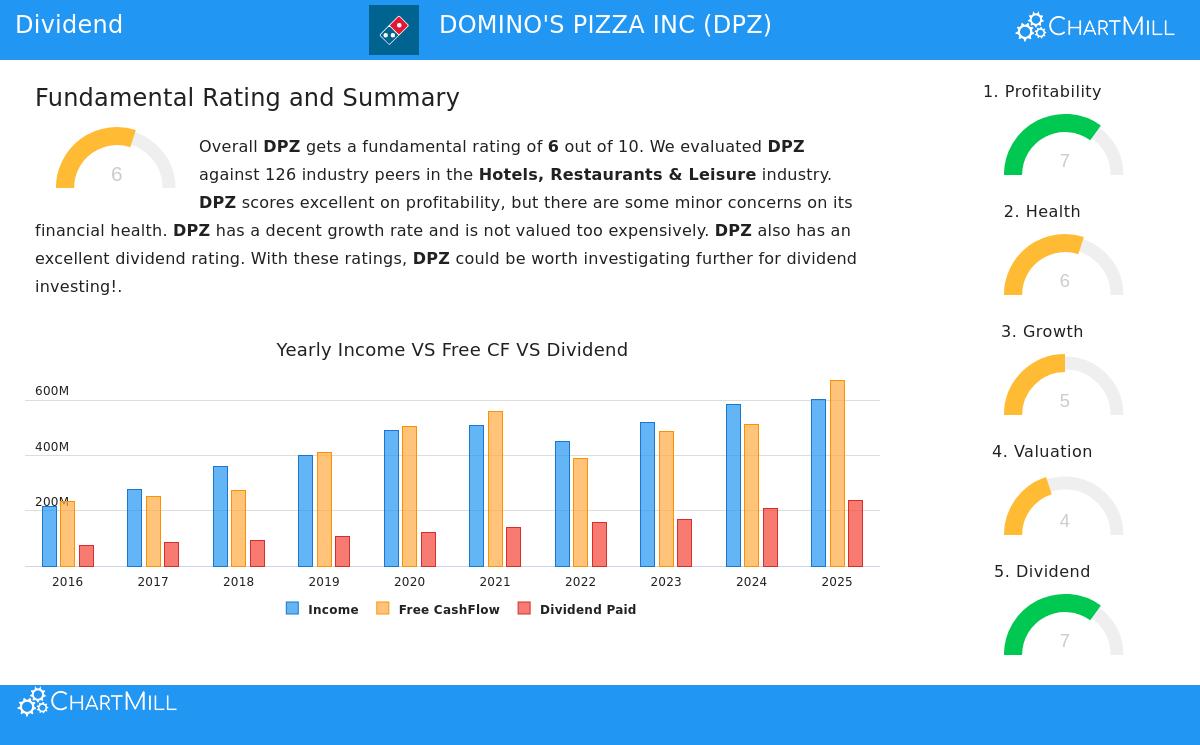

The main attraction of Domino's for an income investor is its long-running and increasing dividend. The company's ChartMill Dividend Rating of 7 out of 10 shows a positive overall view of its payment policy. A more detailed look at the fundamental analysis report shows the main positives behind this rating:

- Dependable History: Domino's has paid a dividend for at least ten years and has not cut it in that time. This record of consistency is a key sign of management's focus on giving capital back to shareholders.

- Notable Increase: The dividend has been rising at a high average yearly rate of about 26% over the last five years. For investors, this means the income received could grow, helping to counter inflation.

- Attractive and Maintainable Yield: With a present yield of 2.12%, Domino's provides a payment that is almost twice the average for its sector (1.09%) and matches well with the wider S&P 500. Significantly, this yield is backed by a comfortable payout ratio of 39.37%, meaning the company spends less than 40% of its net profit on the dividend. This leaves plenty of earnings to put back into the business and keep up the payment during weaker times.

Backed by Firm Earnings

A high dividend rating only matters if the company can pay for it. This is where the "decent profitability" condition is important, and Domino's performs well with a Profitability Rating of 7. The company's franchise-based model produces high returns on capital, which is the source funding shareholder returns.

- The Return on Invested Capital (ROIC) of 64.28% and Return on Assets (ROA) of 35.05% are some of the highest in the Hotels, Restaurants & Leisure sector, doing better than over 99% of similar companies.

- Firm and steady net (12.18%) and operating (19.23%) margins point to a business with control over its prices and effective management.

For a dividend plan, this degree of earnings is essential. It supplies the cash needed to regularly pay the dividend without stressing the company's accounts, making sure the payment rests on a base of profit, not borrowing.

Reviewing Financial Soundness

The last part of the selection plan is financial soundness, where Domino's gets a firm rating of 6. Sound accounts ensure a company can handle economic slowdowns without putting its dividend at risk. The report shows a varied but generally okay situation:

- Stability Positives: The company's Altman-Z score of 3.06 shows a small short-term chance of financial trouble and is more favorable than most sector rivals. Importantly, Domino's has been lowering its debt-to-assets ratio and regularly repurchasing shares, both steps that can signal careful capital stewardship.

- Points to Watch: The report mentions that the Debt to Free Cash Flow ratio is somewhat elevated at 7.17, implying it would take a number of years of cash flow to settle all debts. Still, this measure is more favorable than many in its sector. Cash availability measures like the Current and Quick Ratios are sufficient and compare well within the industry.

For dividend continuity, this health review is positive. The company is generating value (ROIC is above its cost of capital) and shows no serious warnings that would risk its capacity to keep making shareholder payments.

Price and Growth Setting

While the main aim is income, price and growth outlook give useful background. Domino's receives an average Growth Rating of 5, with previous sales and EPS growth in the low-to-mid single digits. However, analysts predict a pickup, with EPS growth projected close to 11% each year. The Valuation Rating of 4 implies the stock is not low-priced, trading at a P/E ratio a bit under the sector average but similar to the wider market. For a dividend investor, the higher price may be reasonable given the company's strong earnings, dependable payment history, and the stable quality of its operations.

A Stock for More Study

Domino's Pizza makes a strong argument for dividend investors applying a quality-oriented selection framework. It joins an increasing, well-backed dividend with top-tier earnings and a fundamentally stable financial position. The stock shows why conditions for dividend quality, earnings, and health are linked: the strong profits allow the dividend, and the firm health helps protect its future.

This review of Domino's is a single finding from an organized search for quality dividend payers. If you want to examine other stocks that fit comparable standards of good dividend quality, firm earnings, and acceptable financial health, you can see the complete selection findings here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or a proposal to buy or sell any investment. Investing holds risk, including the possible loss of the original amount invested. You should do your own complete study and think about talking with a registered financial consultant before taking any investment actions.