For investors looking for chances in the current market, a methodical process is frequently central to finding possibility. One approach uses filters to find companies that seem basically strong but are priced below their estimated true worth. This tactic, based on the ideas of value investing, ignores temporary market feeling to find businesses with good core condition and earnings that are priced well. The aim is to locate stocks where the market price might not completely show the company's lasting earnings ability and money strength, possibly giving a buffer for the patient investor.

A recent filter using these measures has pointed to AMDOCS LTD (NASDAQ:DOX), a worldwide supplier of software and services to communications and media companies. The filter aimed at stocks with a high valuation score, meaning they are inexpensive compared to their financial numbers, while also keeping acceptable scores in earnings, money condition, and expansion. For an investor focused on value, this mix points to a company that is not just a numerically low "value trap," but one that is operationally sound and selling at a price that might be too low for its future.

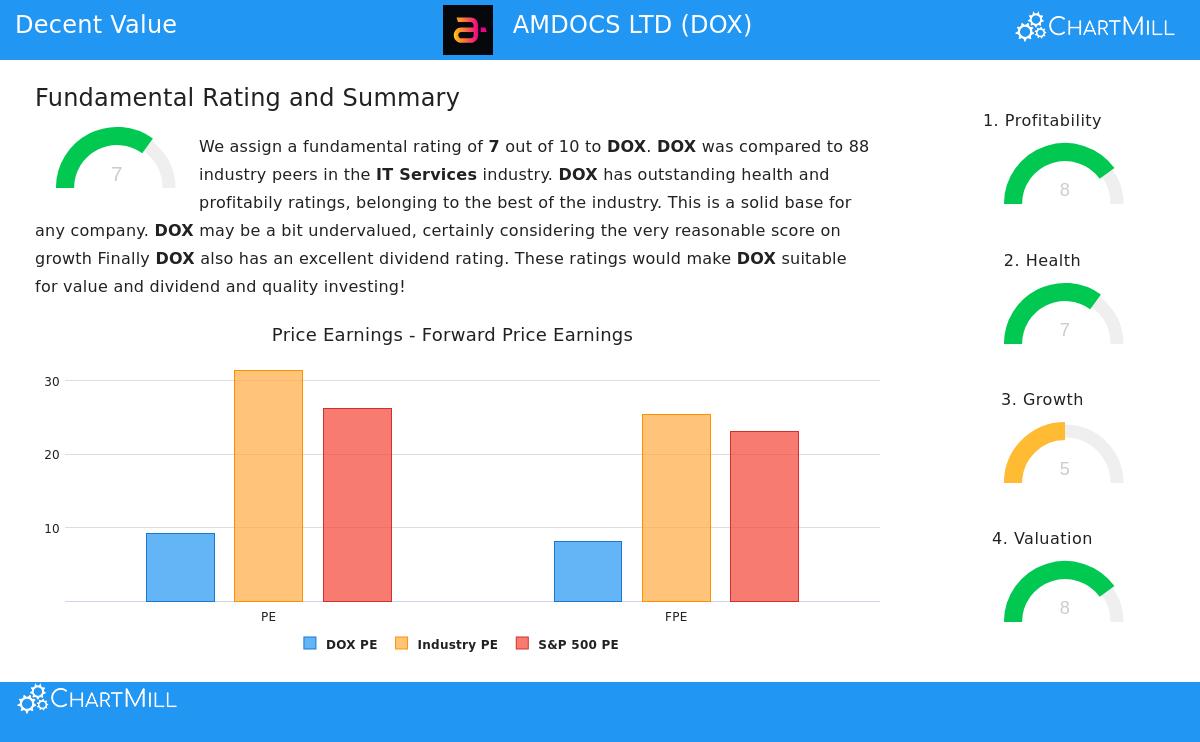

Valuation: An Interesting Starting Price

The most noticeable aspect of Amdocs is its valuation, which gets an 8 out of 10 in ChartMill's basic review. In a market where many technology and service stocks have high multiples, DOX is notable for its low price. This is key for value investing, as a low buy price compared to basics is the main origin of possible gain and gives that important cushion against mistakes.

- Price-to-Earnings (P/E) Ratio: At 9.25, DOX's P/E ratio is sensible alone and is much less expensive than 85% of similar companies in the IT Services field. It is also far under the present S&P 500 average of 26.2.

- Forward P/E Ratio: The view stays good looking forward, with a forward P/E of 8.07, showing experts think earnings will justify its current price.

- Other Multiples: The company also seems inexpensive using other standard valuation measures like Enterprise Value to EBITDA and Price to Free Cash Flow, doing better than over 80% of its field in both.

This group of valuation information implies the market is putting a large discount on Amdocs, maybe because of its established field or seen limits to expansion, in spite of its good operational results.

Money Condition and Earnings: A Good Base

An inexpensive stock is only a wise investment if the company is financially stable. This is where the "buffer" idea is checked. Amdocs gets a 7 for Money Condition and an 8 for Earnings, pointing to a strong core business. Good earnings make sure the company can produce returns, while good condition means it can survive economic drops and spend for what comes next.

Earnings Points:

- The company has very good margins, with an Earnings Margin of 12.24% and an Operating Margin of 18.01%, doing better than over 86% and 90% of its field, in order.

- Returns on capital are strong, with a Return on Invested Capital (ROIC) of 14.00%, putting it in the best group of its area. This shows management is very good at using capital to create profits.

Money Condition Points:

- Ability to pay debts is a main positive. The company has a very small Debt-to-Equity ratio of 0.19 and could clear all its debt with just over one year of free cash flow (Debt/FCF ratio of 1.03), indicating a very strong balance sheet.

- While its current and quick ratios are smaller than some similar companies, the report states this must be viewed with its very good overall ability to pay debts and earnings, and is not always a sign of cash problems for this kind of business.

Expansion: Consistent and Maintainable

For a value stock to reach its possibility, it cannot be still. Amdocs' Expansion score of 5 shows a steady, if not fast, path. This is important because it confirms the company is not shrinking; it is an ongoing business with a workable future, making the low valuation more unusual.

- The company has increased its Earnings Per Share (EPS) at a typical rate of 9.5% over recent years and is predicted to continue close to this speed.

- While sales expansion has been small, future guesses point to a rise, with an expected typical yearly growth of almost 4%.

- This steady, mid-single-digit earnings growth, when joined with its high earnings and dividend (talked about below), adds to an interesting total return idea.

The Full View for a Value Investor

Amdocs shows a united case for an investor thinking of value. It is an earning, financially stable company with a history of steady profit growth. Still, it sells at valuation multiples much lower compared to both the wider market and its own field. Also, it gives a dividend yield of 3.54%, which is above the field and S&P 500 averages, and has a 10-year history of dependable and rising payments. This dividend adds an income part and can help the share price during market swings.

In short, DOX seems to be a standard case of a company whose present market price might not fully hold its true business worth, the central idea of value investing. Investors can see the complete, thorough basic review for DOX here.

This review of Amdocs came from a methodical filter for "acceptable value" stocks. For investors wanting to find other companies that fit similar measures of good valuation joined with good basics, you can see the filter and its present results here.

Disclaimer: This article is for information and learning only and is not a suggestion to buy, sell, or keep any security. The review is based on given information and basic reports. Investing has risk, including the possible loss of original money. You should do your own complete study and think about talking with a skilled money advisor before making any investment choices.