The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, centers on finding well-run, growing companies trading at reasonable prices. This "Growth at a Reasonable Price" (GARP) method avoids speculative, high-flying stocks in favor of businesses with sustainable expansion, solid financial health, and valuations that don't overpay for future prospects. A key tool for spotting such opportunities is the Peter Lynch stock screen, which filters for companies with strong but not excessive earnings growth, high profitability, manageable debt, and an attractive valuation when growth is factored in. One current name that passes this screen is DICK'S SPORTING GOODS INC (NYSE:DKS).

Meeting the Lynch Criteria

A closer look at DICK'S Sporting Goods reveals how its financial profile matches the core parts of the Lynch strategy. The screen's filters are made to isolate companies with a specific mix of growth, value, and stability.

- Sustainable Earnings Growth: Lynch favored companies growing steadily, not explosively. The screen requires a 5-year earnings per share (EPS) growth rate between 15% and 30%. DKS reports a 5-year EPS growth rate of 16.89%, comfortably within this target range. This indicates a history of consistent, manageable expansion rather than unsustainable hyper-growth.

- Attractive Valuation Relative to Growth: Perhaps the most important Lynch metric is the Price/Earnings to Growth (PEG) ratio, which aims to find stocks where the price is justified by the growth rate. A PEG ratio at or below 1 is considered attractive. DKS has a PEG ratio (based on past 5-year growth) of 0.91, suggesting the stock may be reasonably priced given its historical earnings path.

- Strong Profitability: Return on Equity (ROE) measures how efficiently a company generates profits from shareholder equity. Lynch looked for high profitability, with the screen setting a minimum ROE of 15%. DKS's ROE of 15.33% meets this level, indicating effective management and a strong competitive position within the specialty retail sector.

- Solid Financial Health: To avoid over-leveraged companies, the screen filters for a Debt-to-Equity ratio below 0.6, with Lynch himself preferring a ratio under 0.25. DKS's ratio of 0.34 shows a conservative balance sheet, funded more by equity than debt. Furthermore, its Current Ratio of 1.53 exceeds the screen's requirement of 1, showing ample liquidity to cover short-term obligations.

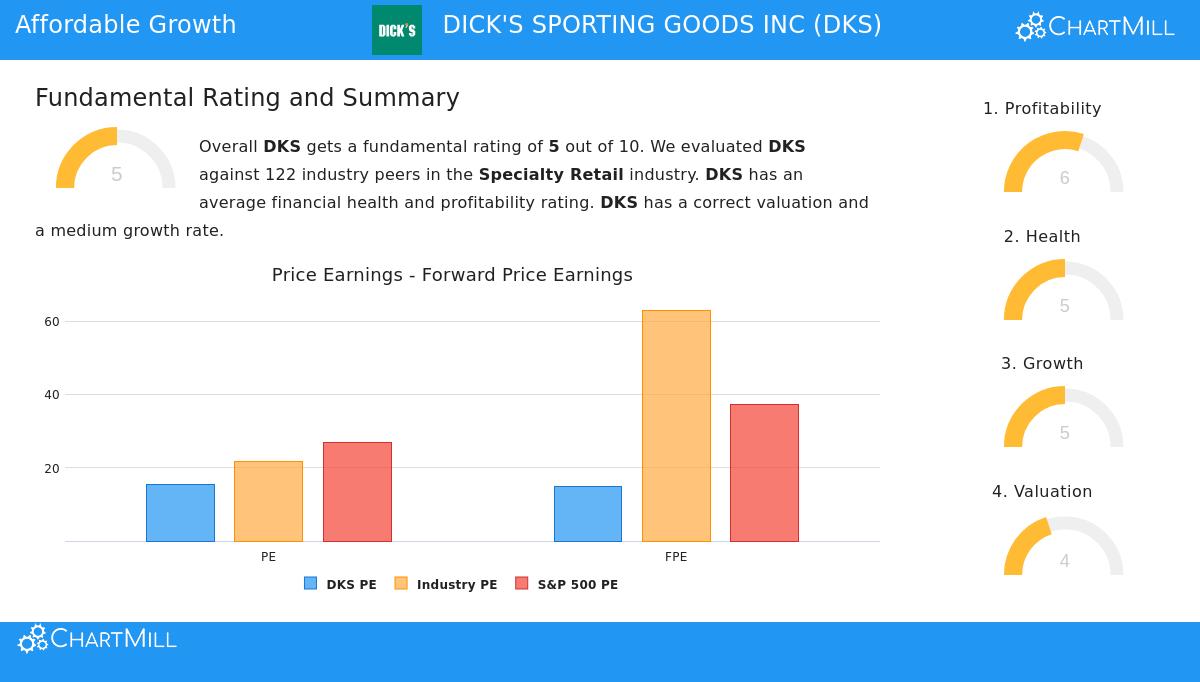

Fundamental Health Check

Beyond the specific screen criteria, a wider fundamental analysis provides context for DKS's investment profile. The company's overall fundamental rating is average, scoring 5 out of 10 compared to its specialty retail peers. This score reflects a mixed but generally stable picture.

The company's profitability is a relative strength, with margins and returns that often do better than industry averages. However, recent metrics show some pressure, with a noted drop in the latest Return on Invested Capital. Financially, DKS maintains a solvent position with an acceptable debt load, though liquidity measures are mixed. From a valuation perspective, its standard Price-to-Earnings ratios appear attractive compared to both the industry and the broader S&P 500. The main concern highlighted in the valuation assessment is the forward-looking PEG ratio, which suggests future growth expectations may not fully support the current earnings multiple. A detailed breakdown of these strengths and weaknesses is available in the full fundamental report.

A GARP Candidate in Focus

For investors aligned with Peter Lynch's philosophy, DICK'S Sporting Goods presents a notable case study. It is not a speculative story stock but an established retailer that has shown a capacity for steady, double-digit earnings growth over a long period. This growth comes packaged with the qualities Lynch valued: high profitability, a clean balance sheet with low debt, and a valuation that, based on its historical performance, does not seem excessive. The stock represents the "growth at a reasonable price" ideal, where an investor pays a fair multiple for a business that is fundamentally healthy and expanding.

While the broader market shows a positive long-term trend with neutral short-term momentum, Lynch's strategy stresses looking beyond such cycles to the underlying business. The analysis indicates DKS's core operations are sound, though investors should watch whether the company can maintain its historical growth rates to justify its valuation moving forward.

Interested in finding other companies that fit this disciplined approach? You can explore the current results of the Peter Lynch screen here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, an endorsement, or a recommendation to buy, sell, or hold any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.