The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, focuses on finding high-quality, growing companies trading at sensible prices, a strategy often called Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, concentrating on businesses with lasting earnings growth, sound financial condition, and prices that do not overvalue future potential. His process uses particular quantitative filters to find candidates, which investors can then study more to assemble a varied, long-term portfolio.

One company that recently appeared from a filter using Lynch's main standards is Cavco Industries Inc. (NASDAQ:CVCO), a designer and builder of factory-built homes. For investors looking for GARP possibilities, Cavco offers an interesting case study of how a company can fit the Lynch model.

Alignment with Peter Lynch Criteria

Peter Lynch’s strategy stresses several important financial measures to balance growth, earnings, and risk. Cavco Industries shows good alignment with these filters:

- Sustainable Earnings Growth: Lynch looked for companies with steady, but not overly rapid, growth. Cavco’s earnings per share (EPS) have increased at an average yearly rate of 21.77% over the past five years. This passes Lynch's usual minimum of 15% and sits in a area that implies the growth is possibly lasting, not short-term.

- Sensible Price Relative to Growth: A key part of the Lynch method is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that might be priced low given their growth path. Lynch preferred a PEG ratio of 1 or lower. Cavco’s PEG ratio, using its past five-year growth, is 0.93, suggesting the market may not completely reflect its historical growth.

- Sound Financial Condition: Lynch avoided high debt. Cavco displays very good balance sheet strength with a Debt-to-Equity ratio of only 0.0066, much lower than Lynch's preferred top limit of 0.6 and even his tighter goal of 0.25. This small debt level gives important financial room and lowers risk in weak economic times.

- Strong Profitability: Return on Equity (ROE) shows how well a company creates profits from shareholder equity. Lynch wanted an ROE above 15%. Cavco’s ROE of 16.93% meets this mark, showing capable management and a good business model.

- Sufficient Short-Term Liquidity: The Current Ratio shows a company's ability to pay its near-term bills. Lynch wanted a ratio of at least 1. Cavco’s Current Ratio of 2.49 indicates a safe liquidity position, above the need.

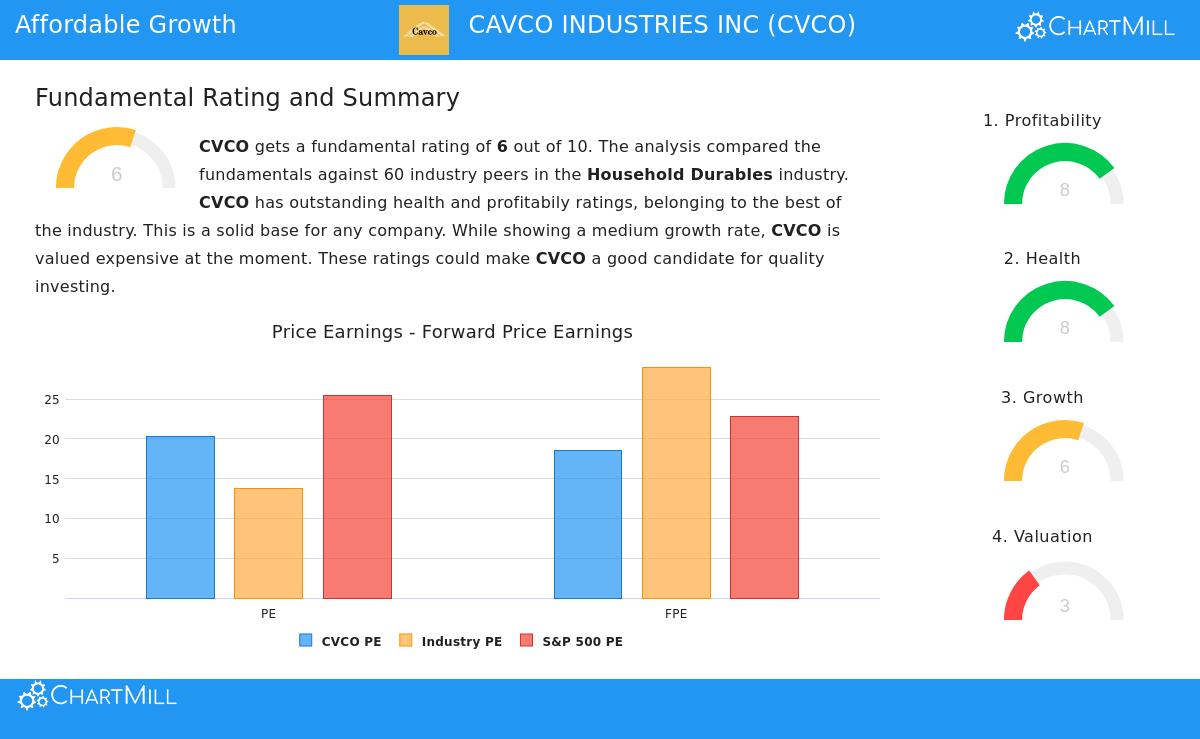

Fundamental Profile Summary

A look at Cavco’s wider fundamental analysis report supports the view from the Lynch filter. The company gets a good total fundamental rating, with specific high points in financial condition and profitability.

- Profitability Strength: Cavco rates well on profitability measures. Its Return on Assets (12.53%) and Return on Invested Capital (16.03%) place in the top group of its Household Durables industry group. Also, both its Profit Margin and Operating Margin have shown upward movement in recent years.

- Very Good Financial Condition: The company’s health score is high. Its clean balance sheet, shown by the very small debt, leads to an excellent Altman-Z score of 9.59, pointing to a minimal risk of financial trouble. The company has also been lowering its number of shares outstanding, which can help per-share measures over time.

- Price and Growth Points: The report states that Cavco’s price, based on common P/E measures, seems quite high next to its close industry group. However, this is weighed against its better profitability and growth. While future sales and earnings growth are predicted to stay positive, analysts forecast a slowdown from the high past rates, a point long-term investors should watch.

You can review the complete details of this fundamental analysis here.

A GARP Candidate for More Study

For investors using a Peter Lynch-type GARP strategy, Cavco Industries meets many of the important conditions. It is a profitable company with a clear past of good earnings growth, a very strong balance sheet, and a price that looks sensible when its growth rate is considered through the PEG ratio. The business, providing factory-built housing, works in a needed, clear field, which fits Lynch’s idea of investing in what you understand.

It is key to remember that passing a quantitative filter is just the start. Lynch stressed thorough non-quantitative study to learn the business model, competitive edges, and possible challenges. Investors should think about elements like the cycles of the housing market, raw material cost increases, and the company's capacity to keep its profit margins and growth path.

Interested in finding other companies that fit the Peter Lynch investment model? You can locate and adjust the stock filter used for this study here.

Disclaimer: This article is for information only and is not financial advice, an endorsement, or a suggestion to buy, sell, or hold any security. Investing has risk, including the possible loss of principal. You should do your own complete research and talk with a qualified financial advisor before making any investment choices.