For investors looking for chances where a company's market price may not show its full business strength, a disciplined value investing method can be a helpful structure. This plan, made famous by Benjamin Graham and later Warren Buffett, means finding stocks selling for less than their calculated true worth while still showing good fundamental health. One way to find these candidates is by looking for companies with good valuation ratings along with acceptable scores in profitability, financial soundness, and expansion. This mix points to a business that is both fundamentally healthy and possibly priced wrong by the market, giving what value investors name a "margin of safety."

COTERRA ENERGY INC (NYSE:CTRA), an independent oil and gas producer working in important U.S. basins, comes up as a stock that matches this description from a fundamental review. The company's total rating implies it may deserve more attention from investors using a value-focused plan.

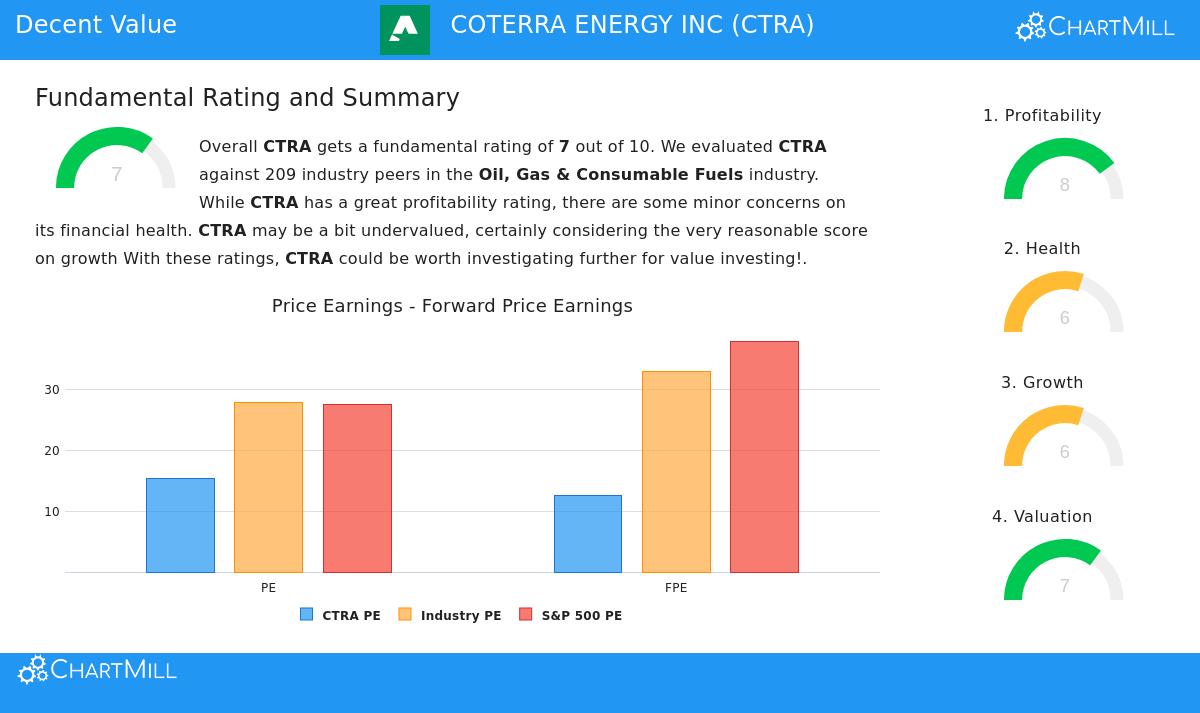

Valuation: A Main Part of Value Investing

The central idea of value investing is buying a dollar's worth of assets for fifty cents. So, a stock's valuation measures are the first screen. Coterra Energy seems to trade at a price lower than both its industry and the wider market, which is a good beginning for value hunters.

- Good Earnings Multiples: CTRA's Price-to-Earnings (P/E) ratio of 15.37 is clearly lower than the S&P 500 average of 27.53. More significantly, it is less expensive than about 66% of similar companies in the Oil, Gas & Consumable Fuels industry.

- Less Expensive Forward View: The view stays positive looking forward. The company's Price-to-Forward Earnings ratio of 12.62 is much below the S&P 500 average and is better than almost 70% of industry rivals.

- Cash Flow and EBITDA Valuation: The stock also seems fairly priced based on cash creation. Review shows CTRA is valued as less costly than more than three-quarters of its industry based on Enterprise Value to EBITDA and less costly than about 69% based on its Price-to-Free Cash Flow ratio.

These valuation measures are important because they give the first sign of a possible difference between market price and true worth. A low P/E ratio, for example, can mean the market is pricing the company's current earnings power too low.

Financial Health: Providing Steadiness

Value investing is not only about buying inexpensive stocks; it's about buying quality companies at low prices. A good financial health rating lowers the danger of a "value trap"—a case where a stock is cheap for a basic reason, like too much debt or weak cash availability. Coterra's financial health picture shows strength.

- Controlled Debt Levels: The company keeps a careful Debt-to-Equity ratio of 0.24, which is stronger than almost 70% of its industry peers. This small use of debt funding gives steadiness and options.

- Strong Ability to Pay Debt: A main point is the Debt-to-Free Cash Flow ratio of 2.34, meaning the company could pay all its debt in just over two years using its present cash flow. This ratio is better than over 83% of the industry, showing a very good ability to meet its debts.

- Sufficient Cash Availability: With Current and Quick Ratios above 1.0, Coterra seems to have enough short-term assets to pay its near-term debts, suggesting no urgent cash concerns.

This financial strength is needed for the value investor's margin of safety. A sound balance sheet means the company is in a better place to handle economic drops or industry changes without harming its work, allowing time for the market to see its true worth.

Profitability: The Driver of True Worth

A company's skill to create profits steadily is what finally pushes its true worth over the long term. Coterra gets high marks on profitability, showing it is not only a steady business but a very productive one in its field.

- Top Industry Margins: The company has notable profit margins. Its Gross Margin of 83.19% puts it in the top 7% of its industry, while its Operating Margin of 32.20% and Profit Margin of 22.45% are better than over 77% and 81% of peers, in order.

- Good Returns on Capital: Coterra's Return on Invested Capital (ROIC) of 8.64% is above its cost of capital and higher than that of over 76% of industry rivals. This points to productive use of capital to create profits.

- Steady History: The review states the company has been profitable with positive operating cash flow in every one of the last five years, adding a level of dependability to its earnings power.

For a value investor, good and rising profitability is a main sign of a high-quality business. It suggests that the company's competitive strengths—whether operational effectiveness, asset quality, or size—are present, supporting the idea that current earnings can continue and are likely to rise.

Growth: The Reason for Price Change

While pure value stocks can be flat, the most interesting chances often include companies that are priced low but still expanding. This expansion can be a reason for the market to price the stock higher. Coterra shows a varied but generally positive expansion picture.

- Excellent Recent Results: The company has given outstanding expansion lately, with Revenue growing over 40% in the last year and Earnings Per Share (EPS) rising by 23%. The multi-year averages for both measures are very strong.

- Moderate Future Predictions: Analyst predictions for future expansion are more measured, with EPS expected to grow about 7.4% each year. This slowing from past fast expansion is mentioned in the report.

- Growth at a Fair Price (GARP): The mix of a low P/E ratio and positive, though slower, expected expansion leads to a low PEG ratio. This "Growth at a Reasonable Price" trait can be especially interesting, as investors are not paying a high price for future expansion estimates.

This expansion picture is significant because it deals with a common problem in value investing: waiting a long time for a reason to change. Coterra's shown skill to expand revenue and earnings gives a basic reason for its true worth to rise over time, possibly closing the difference with its market price.

Conclusion

From a fundamental review, Coterra Energy Inc. presents a picture that matches several ideas of value investing. The stock is priced at a level lower than the market and its peers, it keeps a sound balance sheet with low debt, it works with top industry profitability, and it has a history of good expansion. While future expansion is predicted to slow, the present price does not seem to need fast enlargement. This mix suggests the market may be pricing too low a high-quality, cash-creating business in the energy sector.

A full look at Coterra's fundamental ratings is in its complete Fundamental Analysis Report.

Investors curious about finding other companies that share this picture of good valuation along with acceptable fundamentals can look for more possible chances using the Decent Value Stocks screen.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of original money. Readers should do their own study and talk with a qualified financial advisor before making any investment choices.