For investors aiming to construct a portfolio using the ideas of value investing, the central task is finding companies selling for less than their intrinsic worth. This established method, created by Benjamin Graham and notably used by Warren Buffett, requires a systematic hunt for stocks where the market price is below a calculated guess of the company's true value. The aim is to buy these underrated assets and keep them, permitting the market to in time see and fix the difference. A vital piece of this work is making sure a low price is not a signal of basic problems, but instead a market mistake. This requires examining a company's financial condition, earnings ability, and growth possibilities to verify its fundamental soundness.

CROCS INC (NASDAQ:CROX), the company known for its famous comfort shoes, recently appeared from a screening method made to find such chances. The screen looked for stocks with good valuation ratings while also keeping acceptable scores in earnings ability, financial condition, and growth. This method fits with the value investing rule of looking for a "margin of safety", buying at a price low enough below intrinsic value to permit mistakes in calculation or unexpected market swings. CROX seems to offer a situation where its present market price may not completely show its operational good points.

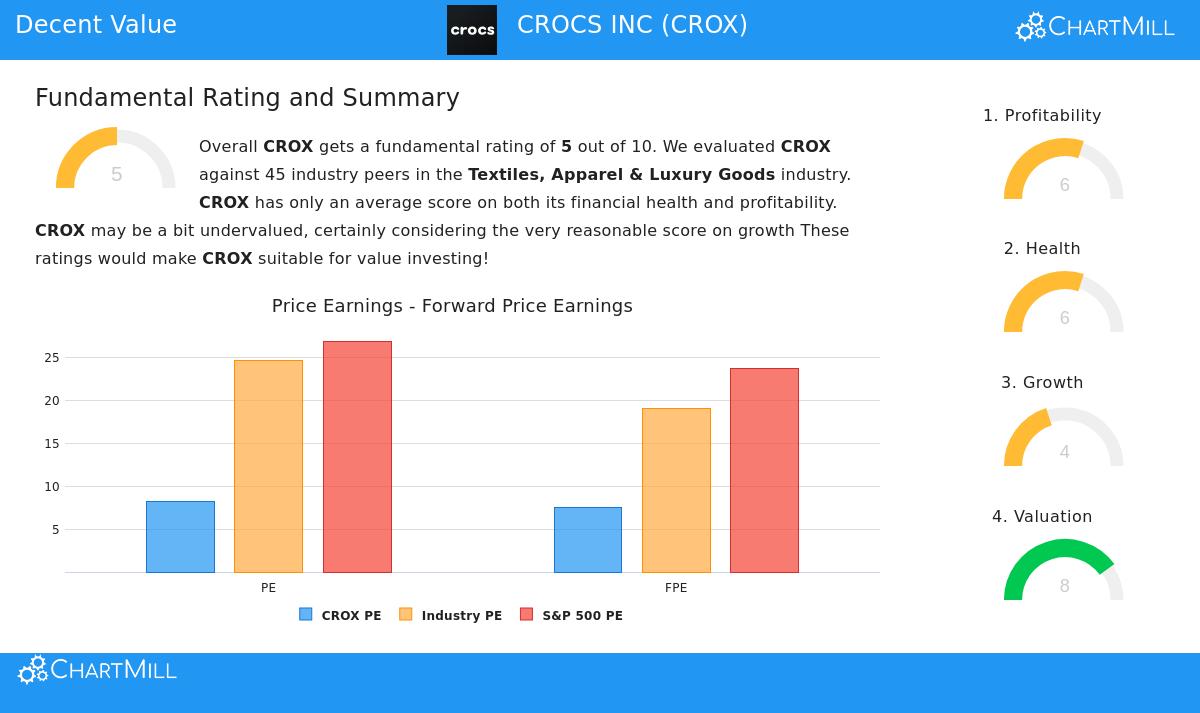

Valuation: The Foundation of the Chance

The strongest point for CROX as a value possibility is in its valuation numbers. The company's basic analysis report gives it a high valuation rating of 8 out of 10, showing it is priced low compared to both its industry and the wider market.

- Price-to-Earnings (P/E) Ratio: At 8.20, CROX's P/E ratio is much lower than the industry average of 24.60 and the S&P 500 average of 26.91. This means investors pay less for each dollar of CROX's earnings compared to most similar companies.

- Forward P/E Ratio: A still more appealing number is the forward P/E of 7.51, which uses future earnings guesses. This is lower priced than 93% of its industry rivals.

- Price-to-Free-Cash-Flow: The company also sells at a low multiple of its free cash flow, a number value investors often value as it shows the real cash a company produces that can be used for dividends, debt payment, or new investment.

For a value investor, these numbers are the first sign. A low valuation makes the chance for price increase as the market re-evaluates the company, if the business itself is solid.

Checking Financial Condition and Earnings Ability

A low-priced stock is only a good buy if the company is financially steady and run profitably, otherwise, it could be a "value trap." CROX's report shows a varied but generally okay picture, with a health rating of 6 and an earnings ability rating of 6.

Financial Condition Key Points:

- Solvency is Good: The company has a sound Altman-Z score of 3.96, pointing to a low short-term chance of financial trouble. Its Debt-to-Free-Cash-Flow ratio is a very good 1.87, meaning it could in theory pay all its debt with less than two years of cash flow.

- Liquidity is a Note: While not in trouble, the company's current and quick ratios are under industry averages, showing it may have less room with immediate bills than some similar companies. However, its good cash production and workable total debt level lessen this worry.

Earnings Ability Good Points:

- Good Operational Margins: CROX does very well in operational effectiveness. Its operating margin of almost 22% is in the top 5% of its industry, and its gross margin of over 58% is also good. These high margins suggest price strength and successful cost management.

- Effective Capital Use: The company's Return on Invested Capital (ROIC) of 20.18% is better than over 90% of its industry, showing that management is creating strong returns from the money put into the business.

These parts are key for the value idea. A sound balance sheet lowers bankruptcy chance, while high earnings ability and effective capital use are signs of a good business that is likely to last and build value over time.

Growth Setting and the Value Idea

CROX's growth rating is a neutral 4, which gives needed setting. The company is not a fast-growth story, but it shows a solid past record with slowing future guesses.

- Past Results: Over the last few years, CROX has provided very strong growth in both Revenue (average 23.86% each year) and Earnings Per Share (30.96% each year).

- Present Change: The last year showed a small drop in both revenue and EPS, a detail the market may be punishing.

- Future Guesses: Analysts guess small forward growth in the mid-single digits for both sales and earnings.

For a value investor, this growth picture is not a reason to reject. In fact, it can be part of the chance. The market may be too fixed on a recent slowdown, underrating the company's shown skill to produce large profits and cash flow from its known brands. The value method proposes that if the company can steady and go back to even small growth, the present low valuation gives a good entry point.

Conclusion: A Possibility for the Value Watchlist

CROCS INC presents a situation that fits several value investing rules. It is priced at a clear markdown to the market and its industry based on normal earnings and cash flow multiples. This markdown exists next to basic good points, including very good operational margins, effective use of capital, and a generally sound financial setup with workable debt. While its growth has slowed, its earnings ability stays good.

The mix of low valuation and acceptable basics suggests the stock may be underrated instead of basically flawed. As with any investment, chances remain, including consumer spending patterns and brand management. However, for investors using a systematic value plan, CROX deserves more study as a possible candidate where the market's present price may not fully show the intrinsic value of its profitable, cash-making business.

Interested in finding more stocks that fit this "Decent Value" profile? You can run the same screen used to find CROX and find other possible chances here.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer to buy or sell any security. The analysis uses data and ratings from ChartMill. Investors should do their own full study and think about their personal money situation and risk comfort before making any investment choices.