For investors looking to balance the search for high-growth companies with some caution, the "Growth at a Reasonable Price" (GARP) method provides a practical middle path. This method tries to find companies with strong and steady earnings growth, but whose stock prices are not too high. It avoids the high risks of speculative, unprofitable growth stocks and also steers clear of potentially stagnant companies. One useful way to apply this method is through systematic filtering, like an "Affordable Growth" filter that looks for stocks with good growth scores, firm financial health and profitability, and a valuation that is not extreme. This process helps find companies where the growth story is backed by fundamentals and the price is sensible.

Credo Technology Group Holding Ltd (NASDAQ:CRDO), a company that creates high-speed connectivity solutions for data infrastructure, recently appeared from such a filter. Its fundamental picture presents a case for the affordable growth idea, mixing very high growth numbers with a sensible valuation and a very strong balance sheet.

Notable Growth Path

The main appeal for a growth investor is a company's capacity to increase its revenue and profits quickly. Credo's recent results and future estimates are particularly strong here. The company is not just growing, it is speeding up at a notable rate.

- Very High Recent Growth: In the last year, Credo reported very high year-over-year growth. Revenue jumped by 226.1%, while Earnings Per Share (EPS) increased by 507%. This shows the company is scaling its business well and turning sales into profits effectively.

- Firm Historical Pattern: This is not a single event. On average, Credo's revenue has increased by more than 52% each year recently, showing a pattern of good performance.

- Firm Future Estimates: Analysts think this pace will keep going. The company's EPS is estimated to grow by an average of 57.5% each year in the near future, with revenue predicted to rise by more than 50% per year. This match between past results and future estimates indicates the growth is built on lasting demand for its connectivity products in data centers and AI infrastructure.

A Valuation with Perspective

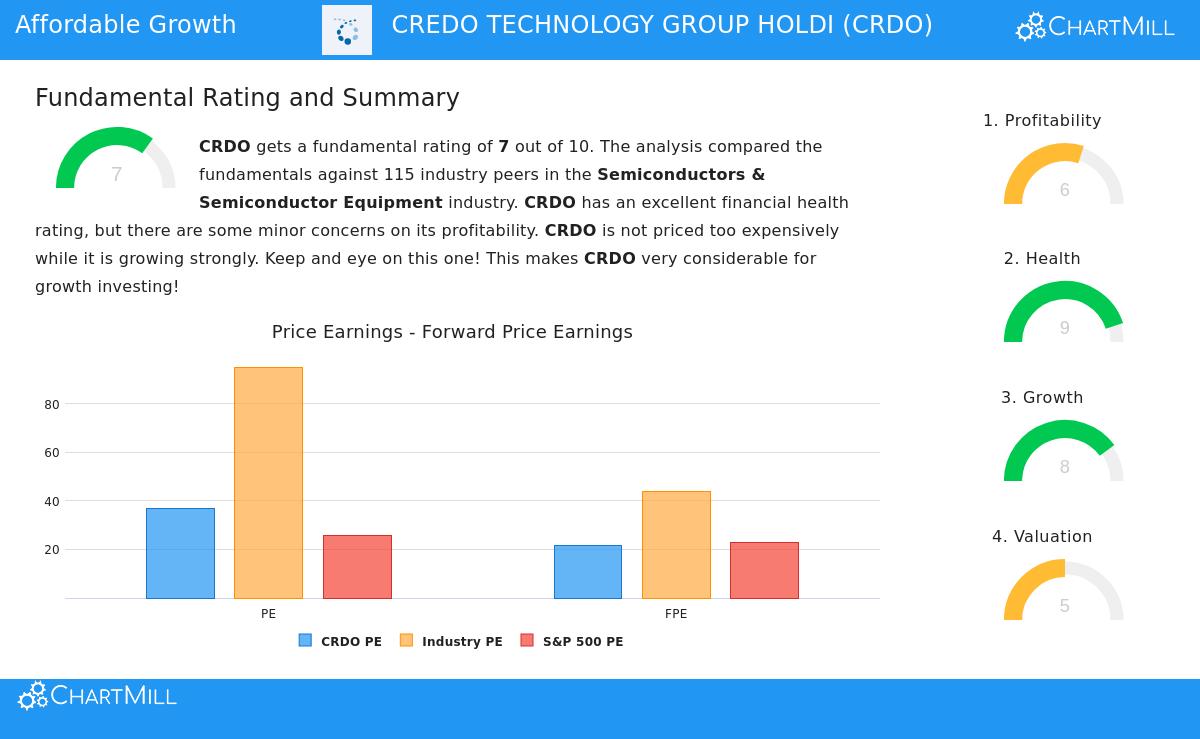

While the growth figures are striking, the GARP method requires they be judged against the stock's cost. Credo's valuation shows a detailed picture. By itself, a Price-to-Earnings (P/E) ratio of 36.75 seems high next to the wider S&P 500 average. However, valuation is relative, and two important points make Credo's situation more interesting.

- Sector Comparison: Credo works in the active Semiconductors & Semiconductor Equipment sector, where high valuations for growth are normal. Compared to others in its sector, Credo's P/E ratio is actually lower than about 76% of the industry. Its Forward P/E ratio of 21.51 is lower than 78% of the industry and is close to the S&P 500 average.

- Growth Adjustment: The most useful measure for a GARP review is the Price/Earnings-to-Growth (PEG) ratio, which changes the P/E for estimated earnings growth. Credo's low PEG ratio shows the market may not be completely accounting for its very high growth path, suggesting the stock could be sensibly valued, or even inexpensive, when its growth speed is considered.

Supporting Fundamentals: Health and Earnings

Lasting growth needs a solid financial base and the capacity to produce earnings. This is where Credo's picture supports the investment idea beyond just growth and price.

Financial Health is a Major Plus Credo receives a high Health score of 9 out of 10. The most notable part is its balance sheet: the company has no debt. This gives great operational freedom and takes away the risk and cost of interest payments. Also, its liquidity is very good, with a Current Ratio of 10.82 and a Quick Ratio of 9.56, showing more than enough short-term assets to cover any needs many times. This very strong balance sheet offers a good safety buffer, letting the company spend on new ideas and handle possible sector slowdowns.

Firm, Getting Better Earnings With an Earnings score of 6, Credo shows it can effectively make money from its growth. Important margins are strong:

- A Profit Margin of 31.81% and an Operating Margin of 30.32% each do better than over 90% of sector rivals.

- Its Return on Invested Capital (ROIC) of 13.66% is very good, showing efficient use of capital to create profits.

While the company has a shorter record of steady yearly profits, the direction of its operating margin has been upward, and its current earnings numbers are clearly firm.

Summary

Credo Technology Group presents a picture that fits well with the ideas of affordable growth investing. The company is experiencing a strong, fast growth period supported by firm future estimates. Importantly, this growth is not matched with a speculative, very high valuation when seen within its sector and through its growth speed (PEG). The idea is further supported by an extremely healthy, debt-free balance sheet and firm earnings numbers. This mix points to a company performing well on a major growth chance while keeping financial care.

For investors curious about other companies that match this balanced picture of firm growth, sensible valuation, and sound fundamentals, more results can be seen by checking the Affordable Growth filter on ChartMill. A detailed look at Credo's fundamental scores is in its full fundamental analysis report.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of your investment. You should do your own research and talk with a qualified financial advisor before making any investment choices.