For investors looking to balance the search for growth with a degree of caution, the Growth at a Reasonable Price (GARP) method presents a practical middle path. This method tries to find companies that are not only increasing their operations and earnings at a good pace but are also trading at prices that do not require extreme optimism. An "Affordable Growth" screen puts this method into practice by selecting for stocks with good growth basics, firm profit and financial condition, and a price that is not too high. The aim is to locate businesses where the market may not have completely accounted for the future growth path, possibly presenting a good balance of risk and reward.

One stock that recently appeared through such a screening process is Corcept Therapeutics Inc (NASDAQ:CORT), a commercial-stage pharmaceutical company that works on creating treatments for serious disorders by adjusting the hormone cortisol. Its main product, Korlym, is approved for Cushing’s syndrome, and the company has a group of newer cortisol adjusters in development.

Growth Path: A Story of Two Parts

The growth story for Corcept is marked by a firm past revenue trend combined with very positive future earnings estimates. This situation is central to its interest as an affordable growth pick.

- Past Revenue Performance: The company has shown firm top-line increase, with revenue growing by 12.79% over the last year and at an average yearly rate of 16.56% over recent years. This steady growth gives a real base.

- Future Expectations: Analysts predict a notable speed-up. Revenue is expected to grow at an average rate of 22.39% each year in the coming years. More notably, earnings per share (EPS) are estimated to rise by about 60% per year. This expected turning point, where earnings growth is predicted to greatly exceed recent past trends, is a main reason for growth-focused investors.

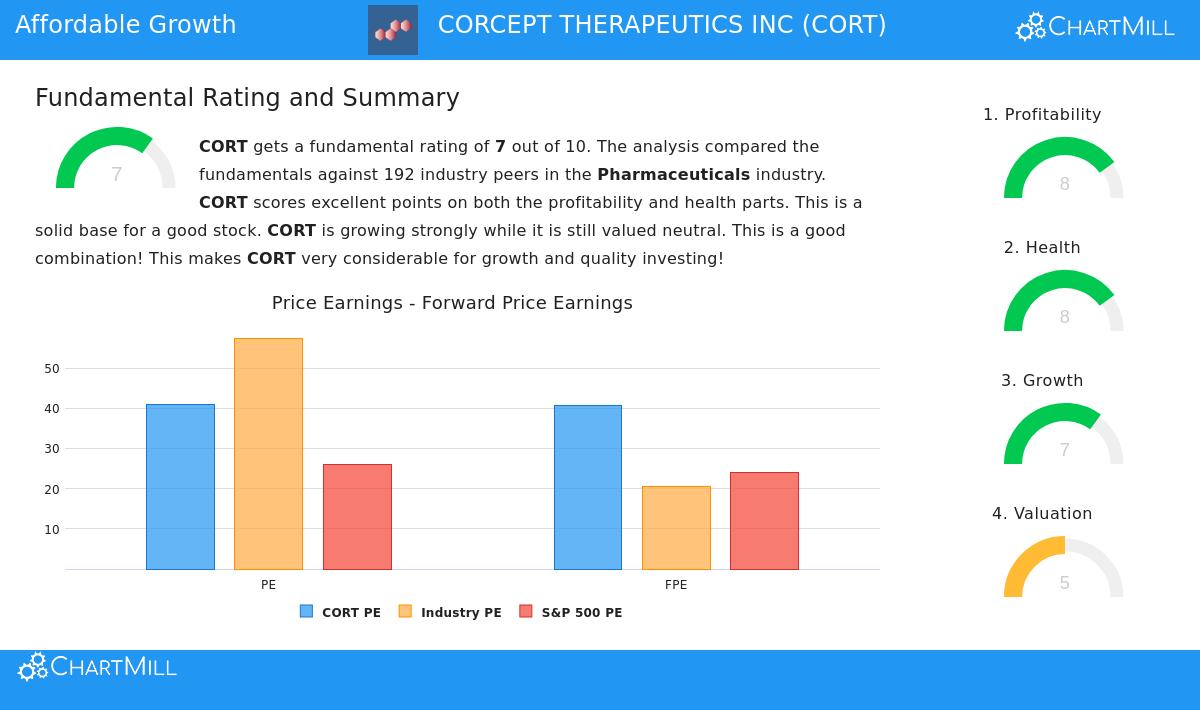

Price: Acceptable Within Setting

With a forward P/E ratio above 40, Corcept does not seem inexpensive on first look, especially next to the wider S&P 500. However, the "reasonable" in GARP is often relative. The price score of 5 out of 10 in the basic analysis indicates a varied but situationally acceptable view.

- Industry Comparison: While the absolute P/E is high, it is notably less expensive than most of its peers in the pharmaceuticals industry. This relative price is an important factor for sector-specific investors.

- Growth Consideration: The high predicted growth rates are a main reason for the current earnings multiple. The screen specifically looks for stocks that are "not overvalued," meaning the market sees the growth but may not have completely accounted for the possible speed-up. Other price measures, such as the Price/Free Cash Flow and Enterprise Value/EBITDA ratios, are seen more positively, ranking better than most industry rivals.

- Profitability Reason: As mentioned in the basic report, the company's firm profit rating may also help explain a higher price.

Foundational Firmness: Profit and Financial Condition

A central idea of the affordable growth method is making sure that growth is built on a stable base. Following high-growth companies with weak finances or low margins can lead to major risk. Corcept scores well here, with profit and condition ratings of 8 each.

- Profit Supports: The company has very good return measures (ROA, ROE, ROIC) that do better than most of the industry. It keeps an excellent gross margin above 98% and has been regularly profitable with positive operating cash flow for years.

- Financial Condition: Corcept’s finances are a specific strong point. The company has no debt, which is unusual and removes interest rate and refinancing risks. Its Altman-Z score shows very low bankruptcy risk, and it holds enough cash to meet short-term needs and pay for its development pipeline.

Summary and Additional Study

Corcept Therapeutics presents an example in the affordable growth screening idea. It mixes interesting, sped-up future growth predictions with a price that, while high in absolute terms, is acceptable compared to its industry and explained by its high profit. Importantly, this growth story is backed by a very firm financial base of no debt and steady cash production, reducing the operational risks often linked with high-growth biopharma stocks.

For investors using a GARP method, CORT represents the kind of pick the screen is made to find: a company where the growth engine is speeding up, but the entry price still includes a buffer provided by its basic condition.

You can view the detailed basic analysis report for Corcept Therapeutics here.

Interested in finding other stocks that fit this profile? Our set "Affordable Growth" screen is updated regularly and can be used to find more investment ideas that balance growth, price, and basic firmness. Click here to see the current screen results.

,

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer or request to buy or sell any securities. The information given is based on supplied data and should not be the only base for any investment choice. Investors should do their own complete study and talk with a qualified financial advisor before making any investment choices.