For investors looking for chances where a company's market price may not completely show its basic business condition, a systematic screening method can be a helpful first step. One such method is to look for companies that seem basically priced below their worth by the market while still showing good operational condition, earnings, and possibility for expansion. This approach fits with main value investing ideas, which concentrate on finding differences between a stock's price and its real worth, if the company's basic conditions are strong enough to support a possible new assessment.

Coeur Mining Inc (NYSE:CDE), a varied precious metals producer with activities in North America, recently came up from such a screening process. The company's basic profile indicates it may deserve more attention from investors focused on the metals and mining industry.

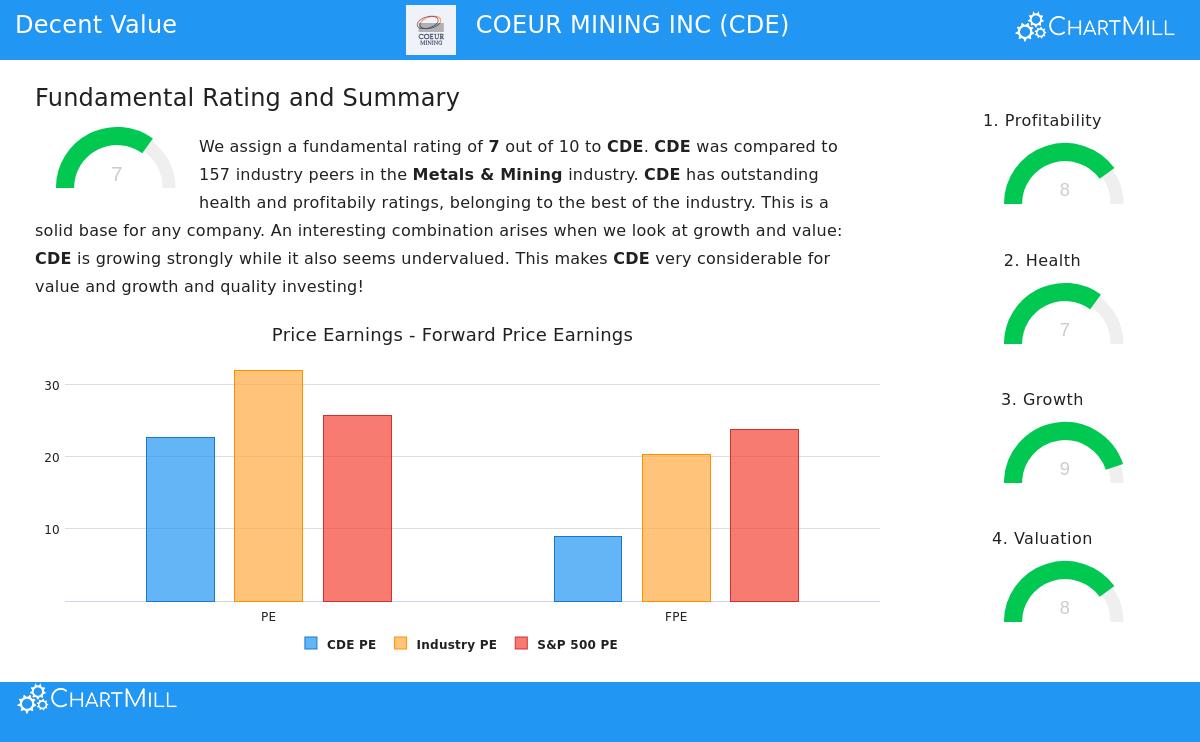

A Closer Look at Valuation

The main draw for a value-focused screen is a good price. Coeur Mining's basic report shows a Valuation Rating of 8 out of 10, indicating the stock is priced low compared to important financial measures.

- Forward-Looking Measures Are Notable: While the usual Price-to-Earnings (P/E) ratio seems high, the more forward-looking Price/Forward Earnings ratio of 8.98 is good. This is much lower than the average S&P 500 company and shows a more fair price based on expected future earnings.

- Good Value Compared to Others: Compared to other companies in metals and mining, Coeur seems priced low in several areas. For example, based on the Price/Forward Earnings ratio, 82.8% of companies in the same industry are priced higher. Also, its Enterprise Value to EBITDA and Price/Free Cash Flow ratios also point to a lower price relative to the industry.

- Growth Consideration: The low PEG ratio, which changes the P/E ratio for expected earnings expansion, shows the market may not be fully paying investors for the company's expansion path. This is a clear signal of a possible value chance.

For a value investor, these measures are key. They look for a "margin of safety"—buying at a price low enough below calculated real value to allow for mistakes in estimates or unexpected problems. Coeur's price profile, especially against its own industry, suggests such a buffer may exist.

Checking Financial Condition and Earnings

A low-priced stock is only a good investment if the company is financially steady and earning money. A big discount on a failing business is a "value trap," not a chance. Coeur's report shows good scores here, with a Health Rating of 7 and a Profitability Rating of 8.

Financial Condition Points:

- The company shows a strong balance sheet with a good Debt-to-Equity ratio of 0.10 and an Altman-Z score of 6.42, showing low near-term risk of failure.

- Cash availability is good, with Current and Quick Ratios above 2.0, showing a strong ability to meet near-term needs.

- Importantly, the Debt to Free Cash Flow ratio is a very good 0.51, meaning it would take the company only about six months of its current free cash flow to pay all its debt.

Earnings Strengths:

- Coeur has moved to strong earnings, with a Profit Margin of 28.30% and an Operating Margin of 36.31%, both placed in the high group of its industry.

- Returns on capital are high, with a Return on Invested Capital (ROIC) of 11.57% and a Return on Equity of 17.68%, each doing better than most industry competitors.

- Critically, these margins have shown gain in recent years, signaling positive operational performance.

These factors are needed for the value argument. Strong condition means the company can handle commodity price changes and put money into its activities without high risk. High earnings suggest the business model works and that the earnings ability supporting the price is real and can continue.

Checking the Expansion Driver

A simple value chance can sometimes involve companies that are not growing. However, mixing value with expansion can be a strong driver for share price gain. Coeur Mining has a high Growth Rating of 9, pushed by very good recent performance.

- High Past Expansion: The company has reported very high year-over-year expansion, with Revenue up 96.41% and Earnings Per Share rising by over 423%. Even on a longer, yearly average, revenue expansion is above 21%.

- Positive Future Path: Experts expect this movement to continue, though at a more steady speed, with forward EPS expansion estimated at 23.68% and revenue expansion at 16.05% each year.

For an investor, this expansion part is important. It provides a possible way for the market to look at the stock again. If Coeur can keep delivering on these expansion expectations while maintaining its earnings, the current price measures may increase, leading to possible price gain beyond just earnings expansion.

Conclusion

Coeur Mining Inc. shows a profile that fits with a "expansion at a fair price" type of value investing. The stock screens as priced low relative to its industry, especially on forward-looking measures, offering a possible margin of safety. This price case is supported not by a weak business, but by one showing very good earnings, a financially sound balance sheet, and a good recent expansion path. The mix suggests the market may be not fully valuing the company's better basic performance and future earnings possibility.

Investors interested in finding similar chances located through basic screening can see the full basic analysis report for CDE or use the set Decent Value Stocks screen to find other choices.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer or request to buy or sell any securities. The information given is based on data supplied and should not be the only base for any investment choice. Investing includes risk, including the possible loss of the main amount. Readers should do their own complete research and talk with a qualified financial advisor before making any investment choices.