Investors looking for growth chances often face a problem: high-growth companies often trade at high prices, leaving little room for error if growth weakens. A method to manage this is to seek "Affordable Growth" or "Growth at a Reasonable Price" (GARP). This method focuses on companies that show good and lasting growth paths but are not overly expensive according to the market. By joining steady growth with fair pricing, together with acceptable financial condition and earnings, investors try to find stocks with possible gains while reducing some of the dangers linked to risky, high-priced choices.

CBRE Group Inc. (NYSE:CBRE), the world's biggest commercial real estate services and investment firm, recently appeared as a pick from such a filtering method. The filter specifically searched for stocks with a high growth score, joined with at least acceptable scores in earnings, financial condition, and pricing. CBRE's basic profile, explained in its detailed analysis report, indicates it matches this GARP model, justifying a more detailed review from investors focused on growth.

Growth Path: A Main Asset

The main attraction of CBRE here is its solid growth score of 7 out of 10. The company is showing good speed both in its recent results and its anticipated future direction.

- Past Results: Over the last year, CBRE's Earnings Per Share (EPS) rose by a notable 25.05%, while Revenue went up by 13.38%. This is not a single event; the company has maintained an average yearly EPS increase of 14.27% and revenue increase of 11.22% over recent years.

- Future Predictions: Experts estimate this growth will persist, though at a somewhat slower speed. EPS is predicted to grow at an average yearly rate of 16.85%, with revenue growth estimated at 9.11%. This steadiness in the growth rate, from past to predicted future, points to a business model with lasting demand sources rather than temporary surges.

For the Affordable Growth method, this steady and above-normal growth is the necessary driver. It gives the basic reason to hold the stock, as rising earnings are a main force for long-term share price gains.

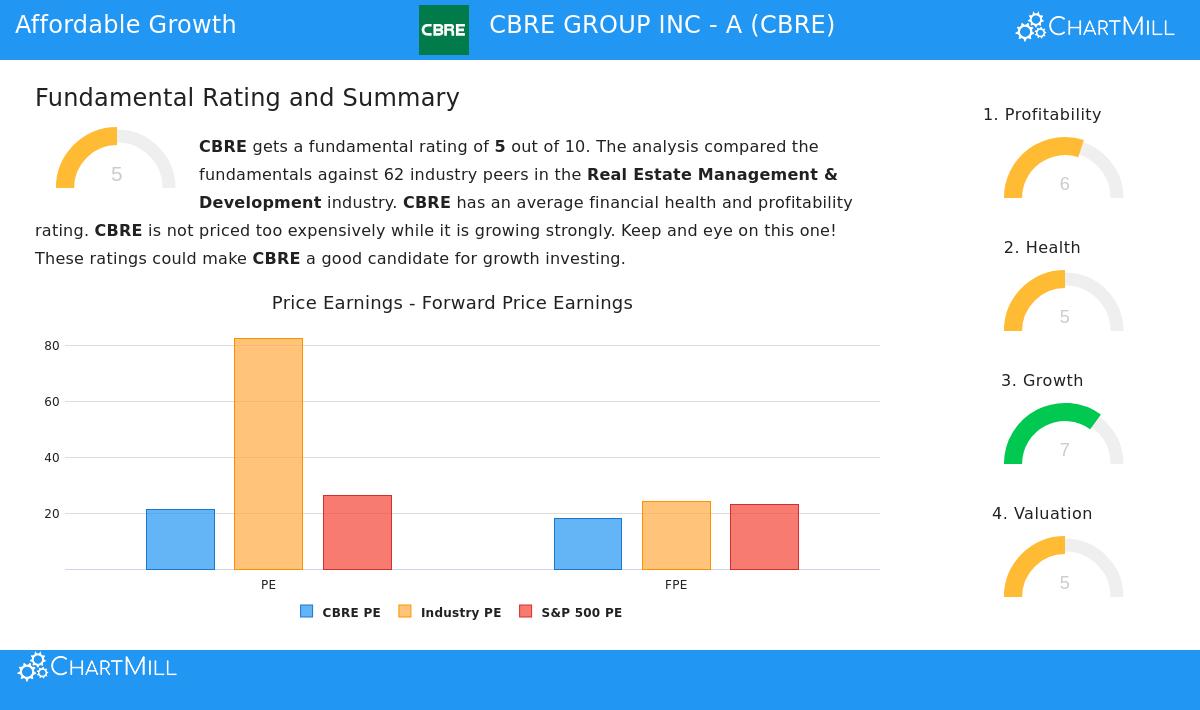

Pricing: Fair in Perspective

A stock with good growth can still be a bad investment if the cost is too great. CBRE's pricing score of 5 shows a neutral or fair position, which is exactly what the GARP filter looks for—growth that is not overpriced.

- P/E Ratios: CBRE trades with a trailing P/E ratio of 21.31 and a forward P/E of 17.96. While these numbers might appear high alone, perspective is key.

- Comparative Cost:

- vs. Industry: CBRE's P/E is less expensive than about 74-82% of similar companies in the Real Estate Management & Development field, which includes many firms with much lower growth histories or unsteady earnings.

- vs. Wider Market: Its forward P/E of 17.96 is also lower than the current S&P 500 average, suggesting the market is not accounting for extreme hope relative to the wider economy.

- Other Measures: The company's Enterprise Value to EBITDA and Price to Free Cash Flow ratios also show a pricing that is somewhat inexpensive compared to most of its industry rivals.

This pricing view is key for the method. It means that investors are not paying extra for CBRE's growth, possibly giving a more attractive risk/reward position than a stock where outstanding growth is already completely accounted for in the price.

Supporting Basics: Condition and Earnings

While growth and pricing are the main standards, the filter's need for acceptable scores in financial condition (score of 5) and earnings (score of 6) works as a quality screen. These elements help confirm the growth is backed by a stable business.

- Earnings: CBRE receives an earnings score of 6. Its returns on assets (3.75%) and equity (13.03%) are some of the top in its field, showing effective use of money. However, attention is drawn to falling profit and operating margins in recent years, a detail for investors to watch. Overall, the company has been regularly profitable with positive cash flow.

- Financial Condition: The condition score of 5 shows a varied but workable picture. Good points involve a safe Altman-Z score (3.04) showing low short-term bankruptcy danger and a record of reducing share count. Worries focus on liquidity, with current and quick ratios (both 1.09) on the lower side of the industry range, and a debt-to-free-cash-flow ratio that is somewhat elevated. The company keeps a moderate debt-to-equity ratio of 0.87.

These "acceptable" scores matter because they indicate the company has the financial strength to handle economic changes and put money back into its growth, making the growth story more believable and lasting over the long run.

Summary and Next Steps

CBRE Group offers a strong example for the Affordable Growth investment method. It joins a shown and expected good growth history—the main reason for investment—with a pricing that seems fair compared to both its field and the wider market. This central mix is supported by adequate, though not outstanding, scores in earnings and financial condition, which help confirm the quality of the main business.

Investors using this method are basically looking for companies where the market may not have completely acknowledged the lasting nature of growth, or where that growth is obtainable at a just price. CBRE's basic report indicates it fits these standards. Naturally, as a worldwide real estate services company, its results are connected to economic and property market changes, which investors must think about.

For those wanting to examine other companies that match this Affordable Growth description, you can see the full filter results using this pre-set stock filter.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal money situation and risk comfort before making any investment choices.