Investors looking to balance the search for growth with fiscal care often consider strategies like Growth at a Reasonable Price (GARP) or "affordable growth." The central idea is to find companies that are increasing their sales and profits at an appealing rate and are also available at prices that do not assume flawless execution. This method tries to reduce risk by steering clear of the most speculative stocks while still taking part in business growth. One way to locate these opportunities is by using a systematic filter for basic financial soundness, profit generation, expansion, and price measures.

A recent filter for affordable growth stocks, which looks for good expansion, acceptable profit generation and financial soundness, and a sensible price, identified medical device leader BOSTON SCIENTIFIC CORP (NYSE:BSX). The company, a top firm in creating and producing devices for interventional cardiology, endoscopy, urology, and neuromodulation, seems to fit this investment thinking well. An examination of its basic financial profile indicates it may present an attractive combination of operational performance and fair market pricing.

Growth Path: Strong and Continued

For a growth-at-a-reasonable-price method, solid expansion is the essential first step. Boston Scientific's past and expected growth meets this requirement. The company has shown it can grow significantly even from a substantial size.

- Past Performance: In the last year, revenue increased by a notable 19.88%, while earnings per share (EPS) rose by 21.51%. The longer-term view is also positive, with a 5-year average annual revenue growth rate of 15.16% and EPS growth averaging 26.01%.

- Future Outlook: Analysts expect this progress to persist, though at a somewhat slower rate. Forward projections estimate average yearly revenue growth of 10.46% and EPS growth of 13.13% in the next few years. This expected slowdown from higher pandemic-period growth is normal but stays firmly in "quite strong" range, offering a good base for future price support.

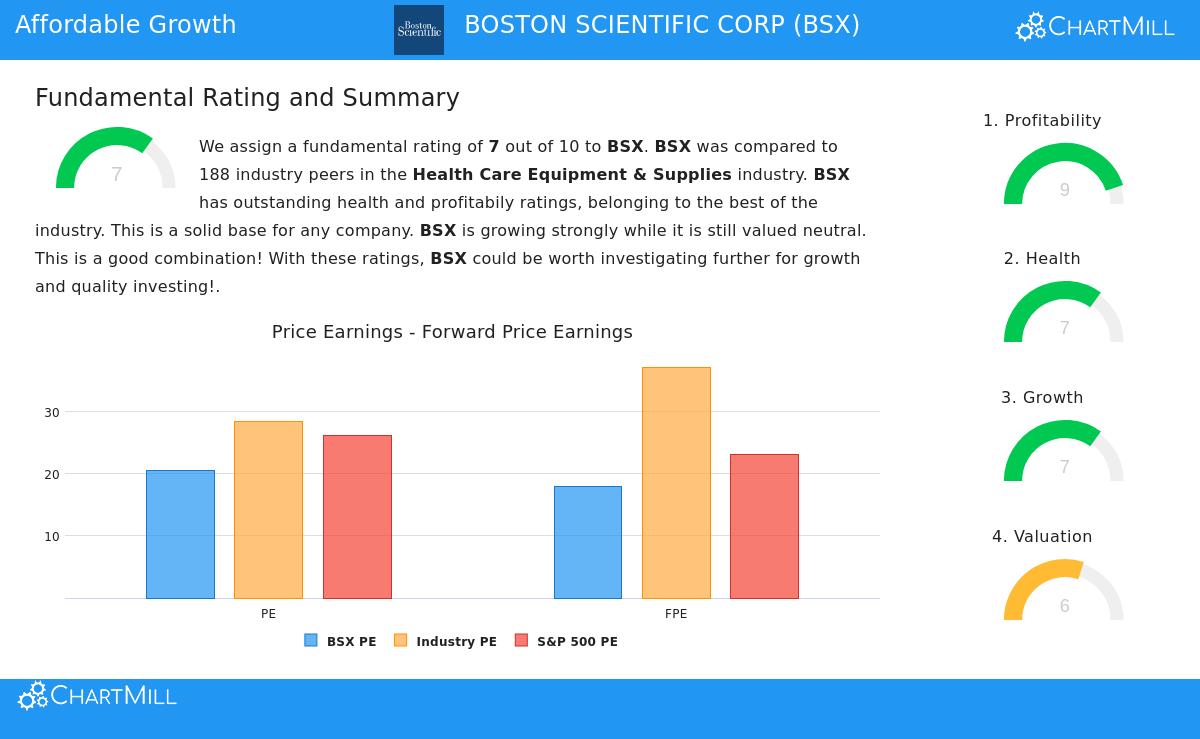

Price: Sensible Given Circumstances

The "reasonable price" part is what distinguishes GARP from pure growth investing. Boston Scientific's price measures imply it is not valued for extreme, speculative expansion, which can be a benefit for risk-conscious investors.

- Industry Comparison: With a Price/Earnings (P/E) ratio of 20.52, BSX is valued lower than nearly 80% of similar companies in the Health Care Equipment & Supplies industry, where the average P/E is above 28. Its forward P/E of 17.90 is also appealing compared to both the industry and the wider S&P 500.

- Cash Flow and EBITDA: The price view gets better when examining cash-based measures. The company's Price/Free Cash Flow and Enterprise Value/EBITDA ratios are lower than about 80% and 74% of industry rivals, in order.

- Growth Adjustment: The PEG ratio, which modifies the P/E for anticipated earnings growth, shows a fair price. This implies the market is not paying too much for the company's forecasted growth, a central idea of the affordable growth method.

Profit Generation and Financial Soundness: A Good Base

A filter for affordable growth needs "acceptable" profit generation and soundness because these elements support lasting expansion. A company losing money or carrying heavy debt cannot maintain growth over time. Here, Boston Scientific performs very well, providing a stable base for its growth plans.

- High-Level Profit Generation: The company receives a top ChartMill Profitability Rating of 9 out of 10. Important margins are industry-best, with an Operating Margin of 19.92% (higher than 92% of peers) and a Return on Invested Capital (ROIC) of 8.70% (higher than 85% of peers). These numbers point to very efficient operations and solid competitive positions.

- Good Financial Soundness: With a sound Health Rating of 7, the company's balance sheet is in good order. The Altman-Z score of 3.90 shows a very small near-term bankruptcy risk, and an acceptable Debt/Equity ratio of 0.46 indicates it is not too dependent on loans. While current and quick ratios are lower than some peers, the report states this is less worrying given the company's very good solvency and profit generation, and the type of its business.

Summary and Next Steps

Boston Scientific Corp illustrates how a large, mature company can still display the traits wanted by affordable growth investors. It combines good, double-digit growth in sales and earnings with a price that seems logical compared to both its industry and its own growth outlook. Importantly, this growth is backed by high-quality profit generation and a financially sound balance sheet, lowering the risk linked to its expansion.

This mix of features is exactly what the affordable growth filter tries to find: companies where growth is not a costly bet but a fairly priced chance backed by basic financial strength. For investors wanting to review other companies that match this careful growth outline, the affordable growth screen can be used to find more options. A more complete look at Boston Scientific's basic ratings is provided in its full fundamental analysis report.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for any investment decision. Investors should conduct their own thorough research and consult with a qualified financial advisor before making any investment decisions.