In the world of long-term investing, few strategies are as respected as the one made famous by Peter Lynch. The famous manager of the Fidelity Magellan Fund supported a disciplined, fundamental-based method that looks for companies with solid, lasting growth, very good financial condition, and a key point, a fair price. This "Growth at a Reasonable Price" (GARP) idea steers clear of the limits of speculative growth seeking and deep-value recoveries, concentrating instead on profitable businesses that an investor can grasp and keep for many years. A stock screener made using Lynch's rules sorts for important measures like earnings growth, profitability, debt amounts, and price to find possible choices for a varied, long-term portfolio.

One company that recently appeared from such a search is Black Stone Minerals LP (NYSE:BSM), a Houston-based master limited partnership (MLP) that owns and manages a large collection of oil and gas mineral and royalty interests across the United States. For investors following Lynch's rules, BSM offers an interesting example of a business that works in a familiar industry while showing the particular financial traits Lynch valued.

Fit with Peter Lynch's Main Rules

The Peter Lynch search uses several number-based filters to find companies with a balanced mix of growth, condition, and price. Black Stone Minerals matches these main rules, which are made to find lasting compounders.

- Lasting Earnings Growth: Lynch preferred companies increasing earnings per share (EPS) between 15% and 30% each year over a five-year span, quick enough to be a growth story, but not so fast that it is probably not lasting. BSM's five-year EPS growth rate of 28.47% fits well within this goal area, showing a solid past record of profit growth.

- Good Price via PEG Ratio: Maybe the central part of Lynch's price method is the Price/Earnings to Growth (PEG) ratio. A PEG of 1 or less hints the stock's price is fair compared to its earnings growth. BSM's PEG ratio, based on its past five-year growth, is a very low 0.42. This shows the market might be pricing its past growth path too low, a main sign for price-aware growth investors.

- Very Good Profitability (ROE): Lynch searched for companies that effectively create profits from shareholder equity. A Return on Equity (ROE) above 15% is seen as very good. BSM's ROE of 23.97% is much higher than this mark, putting it in the top group of its industry and showing high-quality profitability.

- Careful Financial Condition: To stay away from high risk, Lynch required companies with solid balance sheets. His search needs a Debt-to-Equity ratio below 0.6 and a Current Ratio above 1. BSM does very well here, with a very small Debt/Equity ratio of 0.14 and a strong Current Ratio of 3.88. This shows the company is mainly funded by equity and has plenty of cash to meet near-term needs, giving a big safety buffer.

Fundamental Condition and Quality View

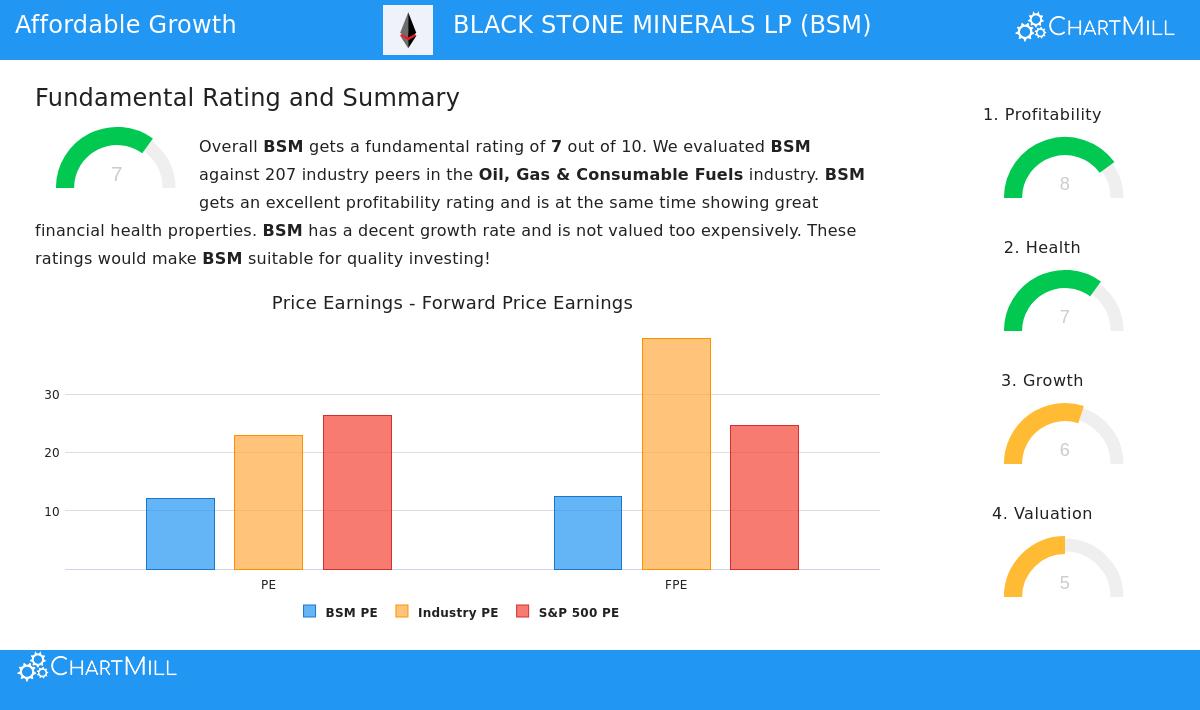

A closer check of the company's fundamental report supports the first search findings. Black Stone Minerals gets a total fundamental score of 7 out of 10, with special force in two areas Lynch would like: profitability and financial condition.

The company's profitability measures are notable. It has industry-best margins, including a Profit Margin of 57.56% and an Operating Margin of 65.63%, doing better than over 90% of similar companies in the Oil, Gas & Consumable Fuels industry. Its returns on capital (ROE and ROIC) are also very good. On the condition side, the outstanding liquidity ratios are confirmed, and the company's ability to pay debt is shown by a very low Debt-to-Free-Cash-Flow ratio of 0.81.

The price is called "correct" with a P/E ratio of 12.06, which is less expensive than both the wider market and most industry peers. The main point of care in the report is about the dividend, which, while giving a high 7.88% yield, has a payout ratio above 100% of earnings, bringing up questions about its long-term future if earnings growth reduces. You can see the full, detailed fundamental study for BSM here.

A "Simple" Business with Clear Economics

Lynch famously told investors to "invest in what you know" and often found big chances in "simple" businesses with clear, understandable models. Black Stone Minerals matches this description. The company does not run rigs or carry the high capital costs and working risks of exploration and production. Instead, it owns mineral rights and gets royalty payments from producers working on its land. This makes a business model with high-margin, fee-like income, limited direct working costs, and connection to commodity prices. It is a clear idea: as long as oil and gas are produced from its large acreage, it creates cash flow. This clarity and staying power match Lynch's liking for understandable companies that are not relying on the next technology trend.

Summary and Next Steps

For investors using a Peter Lynch-style GARP method, Black Stone Minerals LP offers a notable candidate. It meets the number-based search very well, showing solid past earnings growth within a lasting area, top-level profitability, a very strong balance sheet, and a price that seems quite fair when growth is considered. Its business model is standard and easy to understand, working in a field known to many.

However, as Lynch himself would state, a search is only the first step for study. Investors must think about the company's future outlook, the cyclical way of the energy field, and the details of its dividend policy. The search gives a focused list of companies that meet a strict set of first rules, from which more careful checking can start.

Interested in looking at other companies that meet the Peter Lynch search? You can find the present list of passing stocks and run the search yourself here.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of principal. You should do your own study and talk with a qualified financial advisor before making any investment choices.