The investment philosophy of legendary fund manager Peter Lynch, as detailed in his book One Up on Wall Street, centers on finding well-run, growing companies trading at reasonable prices, a strategy often categorized as Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, focusing on companies with sustainable earnings growth, strong financial health, and manageable debt. His process stresses knowing the business you invest in, often beginning from everyday observations, and then using strict fundamental filters to find candidates with lasting competitive strengths. One company that recently appeared from a filter using Lynch's standards is Boot Barn Holdings Inc (NYSE:BOOT).

A Lynch-Style Business Profile

Boot Barn works in a niche Lynch might like: it is a clear, understandable business. As the country's top seller of western and work-related footwear, apparel, and accessories, its performance is linked to real consumer demand instead of temporary technological shifts. With close to 475 stores in 49 states and an increasing e-commerce operation, the company has created a known brand in a specific market. This business simplicity fits Lynch's idea of investing in what you know and can easily grasp.

Meeting the Lynch Investment Standards

A filter constructed on Peter Lynch's main rules points out several important positives in Boot Barn's financial picture. The standards are made to find companies with lasting growth, good profitability, and a strong balance sheet, all signs of a possible long-term success.

- Sustainable Earnings Growth: Lynch looked for companies increasing earnings per share (EPS) between 15% and 30% each year, thinking growth outside this range was often not lasting. Boot Barn's five-year EPS growth rate of 28.7% fits well within this target range, showing a good and steady history of profit growth.

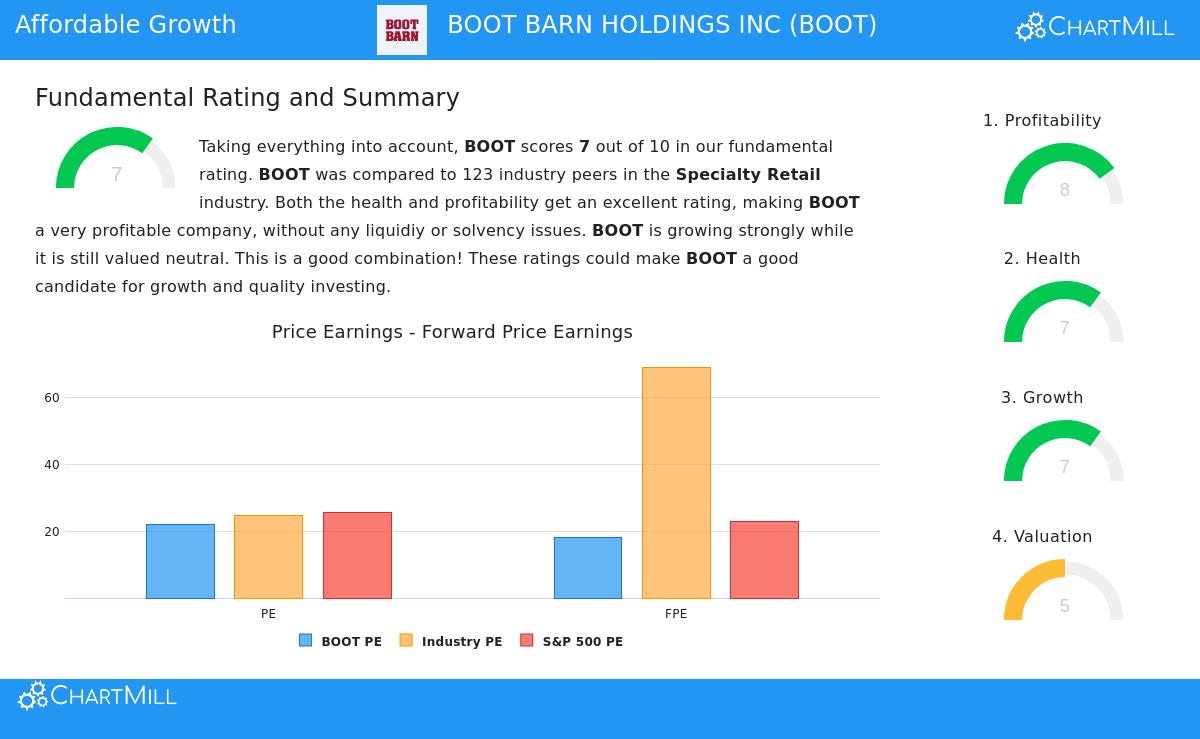

- Reasonable Valuation (PEG Ratio): Maybe the most important Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that could be priced low compared to their growth rate. Lynch preferred a PEG of 1 or lower. Boot Barn's PEG ratio, based on its past five-year growth, is about 0.77, indicating the market may not be completely valuing its historical growth path.

- Strong Financial Health: Lynch was cautious about high debt. Boot Barn shows very good balance sheet strength with a Debt-to-Equity ratio of only 0.01, much lower than the filter's limit of 0.6 and even Lynch's stricter liking for a ratio under 0.25. Also, its Current Ratio of 2.40 shows more than enough cash to handle short-term needs.

- High Profitability (ROE): Return on Equity (ROE) shows how well a company creates profits from shareholder equity. Lynch wanted ROE above 15%. Boot Barn's ROE of 17.07% meets this mark, showing capable management and a profitable way of operating.

Fundamental Analysis Summary

A wider fundamental analysis of Boot Barn supports the image shown by the Lynch filter. The company gets a good total rating, with specific positives in profitability and financial health.

- Profitability is a Key Positive: Boot Barn rates well on profitability measures. Its profit margin of 10.10% and operating margin of 13.45% are in the top tenth of its specialty retail group. The company has also shown steady year-over-year gain in these margins.

- Very Good Balance Sheet: The health score confirms the company's sound financial state. Its very small debt is emphasized by a good Debt-to-Free-Cash-Flow ratio of 0.15 and a strong Altman-Z score of 4.82, meaning very little near-term bankruptcy danger.

- Growth Path: While past growth has been notable, analysts forecast a slowdown to still-good levels. Expected future EPS growth is near 13.5% each year, which, while lower than the past, stays solid. The valuation part notes that Boot Barn's current P/E ratio is about the same as the wider S&P 500, and its good PEG ratio helps make up for what could otherwise seem a high earnings multiple.

For a complete look at these measures, you can see the full fundamental analysis report for BOOT.

Suitability for GARP Investors

For investors looking for growth at a reasonable price, Boot Barn offers a strong example. It joins the features Lynch valued: a clear business model, a history of good and sustainable earnings growth, and a price that seems fair when that growth is considered through the PEG ratio. The company's clean balance sheet gives a safety buffer, lowering risk in economic declines, while its high profitability and return measures indicate a lasting competitive edge in its niche retail area.

While the wider market direction is currently down, Lynch's method is intentionally separate from short-term market timing. The attention stays on the company's fundamental positives and its ability to build value over years, not quarters.

Finding Similar Opportunities

Boot Barn is one of a few companies that currently pass a filter designed on Peter Lynch's investment ideas. Investors curious about finding other possible GARP choices can view the full list of results using the Peter Lynch Strategy stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.