For investors looking to find opportunities where the market price may not fully show a company's actual worth, a systematic screening process can be a useful tool. One such method is the "Decent Value" screen, which tries to find stocks that seem basically priced low by the market while still showing good operational condition. This approach selects for companies with a good valuation rating, suggesting their shares are priced well compared to earnings, cash flow, or assets, but which are not low-priced for bad reasons. Importantly, these stocks must also show acceptable scores in profitability, financial condition, and growth, making sure the low price comes with a workable and well-managed business, not one failing. This matches the main ideas of value investing, which stress a safety buffer by buying assets for less than their true worth, if the core company is stable.

AUTOLIV INC (NYSE:ALV), a world leader in automotive safety systems like airbags and seatbelts, comes up as a candidate from this screening method. The company's fundamental analysis report suggests it presents an interesting profile for investors searching for value combined with basic strength.

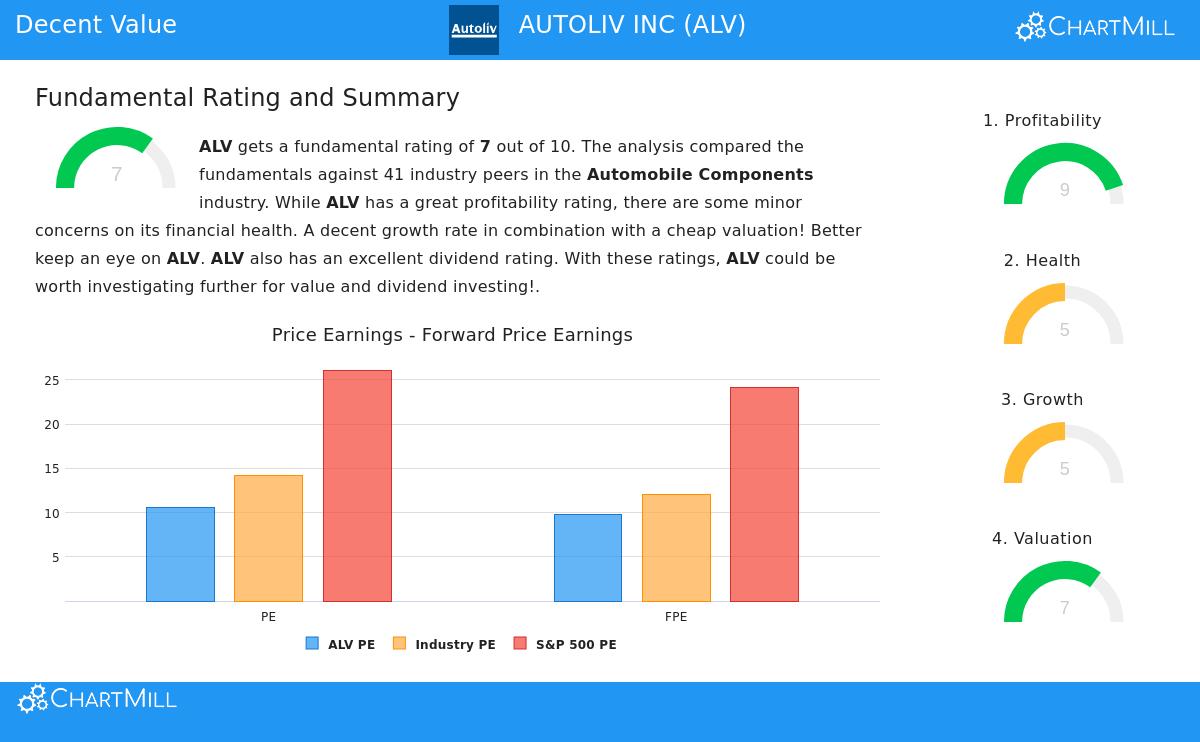

Valuation: An Interesting Entry Point

The foundation of the value investment case for Autoliv is its appealing valuation numbers. The company's shares trade at levels that are noticeably lower than both the wider market and its industry group, pointing to a possible gap between price and business results.

- Price-to-Earnings (P/E): With a trailing P/E ratio of 10.56 and a forward P/E of 9.79, Autoliv is valued much below the S&P 500 averages (26.11 and 24.12, respectively). It is also less expensive than about 75-78% of its group in the Automobile Components industry.

- Cash Flow and EBITDA: The valuation appeal continues to cash-based numbers. The company's Enterprise Value to EBITDA and Price to Free Cash Flow ratios are better than a large number of its competitors, showing the market is pricing its cash-producing ability cautiously.

For a value investor, these numbers are the first filter. A low P/E ratio can indicate a low-priced stock, but it is only a beginning. The important question is whether the low price is explained by poor basics or if it shows a market mistake. Autoliv's ratings in other areas point to the latter.

Profitability: A High-Performing Business

A low-cost stock is only a good investment if the company is profitable and uses its money well. This is where Autoliv stands out, getting a high ChartMill Profitability Rating of 9 out of 10. The company shows very good returns on capital, which is a main sign of a good-quality business.

- Better Returns: Autoliv's Return on Invested Capital (ROIC) of 16.98% and Return on Equity (ROE) of 28.58% are notable figures, doing better than over 97% of its industry group. A steadily high ROIC is a mark of a company with a lasting competitive edge and good management.

- Good and Increasing Margins: The company keeps a solid Operating Margin of 10.0% and a Profit Margin of 6.8%, both of which are in the top group of its industry. Significantly, these margins have shown gain in recent years, a signal of positive operational movement.

This strong profitability picture is necessary for the value argument. It shows that Autoliv's low price is not a sign of poor earnings power. Instead, it suggests the market may be setting too low a value on a company that creates good profits from its operations.

Financial Condition and Growth: A Steady Base

While the price is low and profitability is high, a value investor must also check the company's stability and future outlook. Autoliv's financial condition rating is acceptable, though it shows a varied picture that needs notice.

- Financial Condition (Rating: 5): The company's ability to pay debts is generally good, with a workable Debt-to-Free Cash Flow ratio of 3.01, showing it could pay off debt fairly fast. However, liquidity numbers like the Current and Quick ratios are lower than many industry peers, suggesting a closer working capital situation that investors should watch.

- Growth (Rating: 5): Autoliv shows a reasonable growth path. Past Earnings Per Share (EPS) growth has been strong at over 25% on average each year, and analysts think future EPS growth will continue at a good rate above 11%. Revenue growth is more moderate but steady.

This mix is key for the "Decent Value" plan. The screen needs not just low price, but also "acceptable" condition and growth. Autoliv meets this by showing a way for future earnings increase (supporting true worth growth) and a financial setup that, while not perfect, is not in trouble, giving that needed safety buffer against unexpected drops.

Conclusion: A Value Case in an Important Industry

Autoliv presents a situation where traditional value investing numbers line up with good business basics. The stock trades at a clear lower price than the market and its sector, yet the company behind it is highly profitable, gets very good returns on capital, and is expected to keep growing. The screen found it not as a failing company selling at a low cost, but as a basically stable operator that the market may be pricing too cautiously.

For investors using a value-focused plan, Autoliv represents the kind of opportunity screens are made to find: a possible difference between market price and true worth, supported by number-based proof of business quality. As with any investment, careful study is needed, especially about its liquidity numbers and the up-and-down nature of the automotive industry. However, for those making a watchlist of low-priced stocks with good basics, Autoliv deserves more study.

You can view the full, detailed fundamental analysis report for Autoliv here: Autoliv Inc. Fundamental Analysis.

If you are interested in finding more companies that fit this "Decent Value" profile, you can explore the predefined screen directly: Discover More Decent Value Stocks.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion to buy or sell any security, or a support of any investment plan. The analysis is based on data and ratings given by ChartMill, and investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices. Past results are not a guide for future results.