For investors looking to balance the search for growth with fiscal care, the "Growth at a Reasonable Price" (GARP) or "affordable growth" strategy offers a sensible middle path. This method looks for companies that are increasing at an above-average pace but are not trading at extreme prices that assume far-off future success. It avoids the high swings of speculative growth stocks while steering clear of the slow progress that can come with deep-value choices. By using a systematic filter that looks for good growth, steady profitability, acceptable financial condition, and a fair price, investors can create a list of companies that mix forward motion with a safety buffer.

One company that recently appeared through this method is AUTODESK INC (NASDAQ:ADSK), a global leader in design software for architecture, engineering, construction, and manufacturing. The company's set of products, including industry standards like AutoCAD, Revit, and Maya, places it at the heart of digital change across several important industries. According to a fundamental analysis report on ChartMill, Autodesk receives an overall fundamental rating of 7 out of 10, reflecting a strong profile with specific advantages that fit well with the affordable growth idea.

Growth Path: Strong Past and Future Momentum

The center of any growth investment is, expectedly, growth. Autodesk’s rating in this area is a solid 7, backed by steady increase in both revenue and earnings. This is important for the GARP strategy, as lasting growth supports a premium price and is the driver for future investor gains.

- Past Performance: The company has shown good historical growth. Over the last year, Revenue increased by 15.55% and Earnings Per Share (EPS) rose by 19.20%. More notably, the average yearly EPS growth over recent years is 24.81%.

- Future Expectations: Analyst estimates suggest this forward motion is likely to persist, though at a somewhat slower speed. Forecasts point to average yearly EPS growth of 17.29% and Revenue growth of 12.68% in the next years. This future stability is essential, as the strategy looks for growth that is lasting, not just a temporary spike.

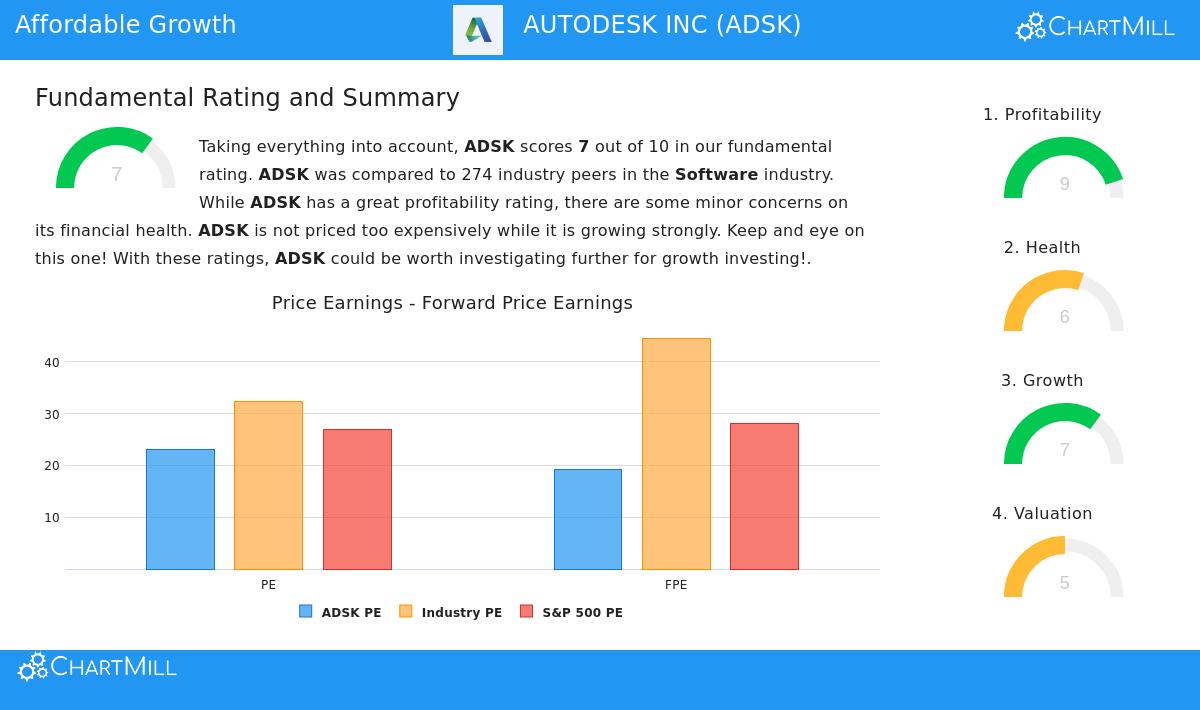

Valuation: A Sensible Price for Quality

A valuation rating of 5 shows Autodesk is neither obviously cheap nor overly costly on an absolute basis. For a GARP investor, this "neutral" or "sensible" valuation is exactly the goal, it means the market has not become overexcited. The report points out a detailed view:

- Relative Value: While Autodesk's Price/Earnings (P/E) ratio of 23.0 might appear high alone, it is actually lower than 64% of its software industry competitors. Its Forward P/E of 19.16 shows a similar pattern, being more appealing than 66% of the industry.

- Growth Adjustment: The PEG ratio, which modifies the P/E for expected growth, is noted as low, suggesting the stock's price may be quite sensible when its growth outlook is considered. The report states that Autodesk's excellent profitability and expected earnings growth could support its current multiple.

Supporting Fundamentals: Profitability and Condition

An affordable growth stock must be more than just a fast-increasing company at a fair price, it needs a solid base. Autodesk’s high profitability score of 9 provides that base, showing the growth is high-quality and efficient.

- Profitability Strength: The company performs very well with a Return on Invested Capital (ROIC) of 20.36%, better than 94% of its industry. Its operating margin of 23.87% and gross margin above 90% are near the top in the sector, showing strong pricing ability and operational effectiveness.

- Financial Condition Points: With a condition rating of 6, there are varied signals. Solvency is strong, with an Altman-Z score showing no bankruptcy danger and a very good debt-to-free-cash-flow ratio. However, liquidity ratios like the Current and Quick ratios are below 1.0, which usually causes concern. The analysis usefully explains this, stating that given the company's very good profitability and solvency, these low ratios may not point to immediate liquidity problems but should be watched against the details of its subscription-based business model.

Conclusion and Further Research

Autodesk presents a strong case for investors using an affordable growth strategy. It pairs a good, clear growth history with encouraging future estimates, all while trading at a price that is sensible compared to its high-quality software peers. Its top-tier profitability measures suggest this growth is lasting and efficient, a key distinction. While investors should note the comments on liquidity within the financial condition review, the overall fundamental view supports the idea of a company increasing at a sensible price.

This review of Autodesk came from a systematic filter for affordable growth stocks. If you are interested in examining other companies that meet similar standards of good growth, acceptable fundamentals, and sensible valuation, you can see the full filter results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.