For investors looking for dependable income, a methodical screening process can help find companies that provide more than a high stated yield. The aim is to locate businesses with lasting payouts, backed by good basic financials. A typical method uses filters for stocks with a high ChartMill Dividend Rating, which looks at dividend yield, growth, history, and safety. To confirm these dividends rest on a firm base, this screen is usually combined with minimum levels for the ChartMill Profitability and Health Ratings. This process focuses on companies that can not only pay their present dividend but are also financially sound enough to keep and possibly raise it later.

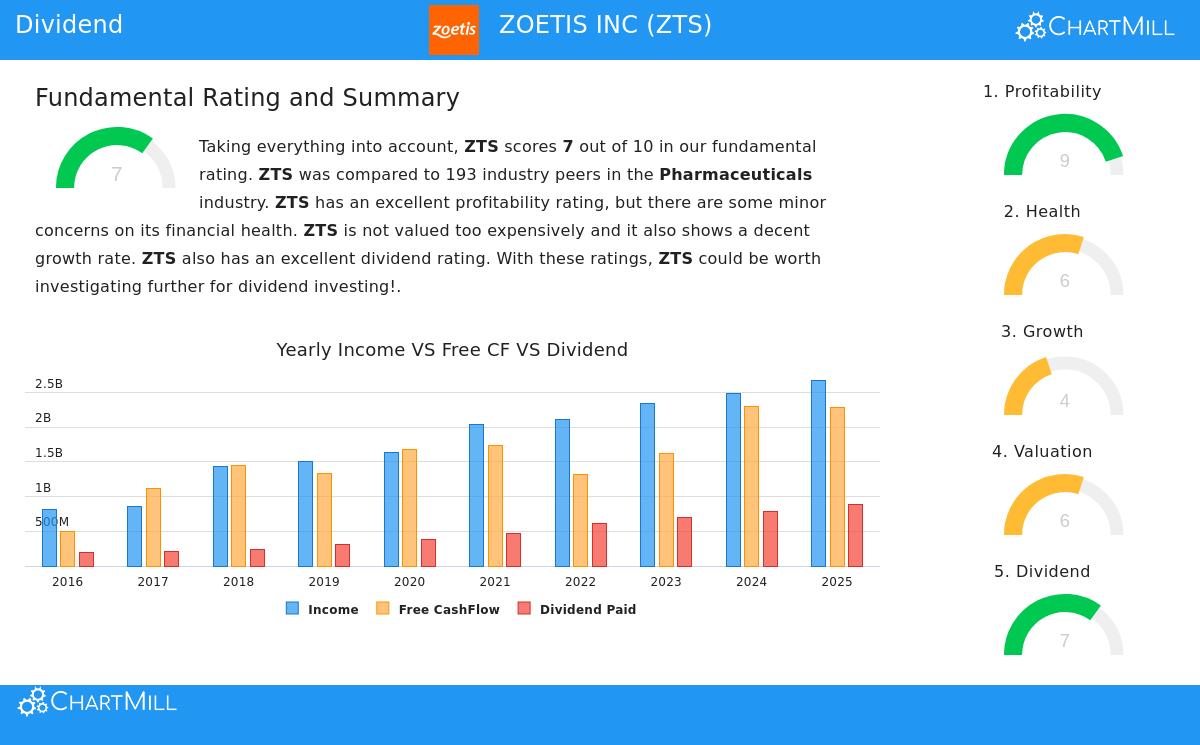

One company that appears from this methodical screen is Zoetis Inc. (NYSE:ZTS), the top animal health company globally. With a ChartMill Dividend Rating of 7, a Profitability Rating of 9, and a Health Rating of 6, ZTS shows an interesting profile for dividend-focused investors who prefer quality and safety over seeking the absolute highest yield.

A Dividend Profile Made for Dependability

The main attraction for income investors is found in Zoetis's dividend traits, which rate well on important measures of dependability and growth possibility.

- History and Growth: Zoetis has built a dependable history, having paid and, notably, raised its dividend for at least ten straight years. This steadiness is a sign of established dividend payers. Also, the company has raised its dividend at a notable average yearly rate of over 20% during this time, easily exceeding inflation and delivering real income growth for shareholders.

- Safe Payout: Safety is important, and here Zoetis also does well. The company pays about 33% of its earnings as dividends. This careful payout ratio leaves a good buffer, making sure the dividend is secure even if earnings see short-term challenges. It also allows good space for future dividend raises and money put back into the business.

- Good Yield: With a present dividend yield of 1.64%, Zoetis gives a yield that is more than twice the average for its pharmaceuticals industry group. While not an extremely high yield, it is a noticeable income payment that, when joined with good growth and safety measures, creates an interesting total return picture.

The Base: Outstanding Profitability

A lasting dividend needs to be paid for by a profitable business, and this is where Zoetis does very well, as seen in its almost perfect Profitability Rating of 9. The company's financial results supply the source for its shareholder payments.

- High Margins and Returns: Zoetis works with excellent efficiency. Its profit margin of 28.2% and operating margin of 38.5% place in the best group of its industry. More significantly, its Return on Invested Capital (ROIC) of nearly 22% shows it is very good at creating profits from its capital spending. This high profitability is the basic reason the company can manage to give cash to shareholders while still paying for future growth.

Financial Health: A Small Point to Consider

While the total Health Rating of 6 is seen as acceptable and fits the screening requirements, it is the part where Zoetis shows some small points for investors to note. The company has a large amount of debt, with a Debt-to-Equity ratio of 2.71. However, this is offset by several good points:

- The company creates strong and steady cash flow, with a Debt-to-Free-Cash-Flow ratio below 4, which is seen as good.

- Its Altman-Z score of 5.39 shows a very small short-term chance of financial trouble.

- Liquidity is good, with a Current Ratio above 3, meaning it can readily cover near-term bills.

In short, the company uses debt with purpose to improve returns, and its powerful cash creation gives a clear way to handle this debt without trouble. For dividend safety, the strong cash flow is the more important measure, and Zoetis performs well there.

Valuation and Growth Setting

From a valuation view, Zoetis trades at a P/E ratio near 18, which is low compared to both its own past averages and the wider pharmaceuticals industry. When thinking about its high profitability and dependable growth profile, the valuation seems fair. Growth is predicted to continue at a moderate speed, with analysts forecasting mid-single-digit revenue and high-single-digit EPS growth in the next few years. This stable, expected growth backs the argument for future dividend raises.

For investors wanting to examine other companies that fit similar standards of good dividends, firm profitability, and acceptable financial health, you can see the full screen results here.

To conclude, Zoetis Inc. shows the kind of company a quality dividend screen tries to find. It provides a reasonable and increasing yield supported by a very strong profitability profile and a safe payout ratio. While its debt level is high, it is handled well through excellent cash creation. For dividend investors focusing on dependability, growth possibility, and business quality over pure yield, ZTS deserves more study. A more complete look at its basic ratings is in its full ChartMill Fundamental Analysis Report.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer to buy or sell any security. Investors should do their own study and think about their personal money situation before making any investment choices.