For investors aiming to construct a portfolio on value investing principles, the central task is finding companies priced below their inherent value. This method, established by Benjamin Graham and notably used by Warren Buffett, requires a systematic hunt for stocks where the market price seems to underestimate the actual worth of the enterprise. A crucial element of this process is not only locating inexpensive stocks, but steering clear of "value traps", companies that are low-priced for a cause, frequently because of worsening fundamentals. Consequently, a sound screening technique looks past basic valuation measures like the Price-to-Earnings (P/E) ratio. It also evaluates the fundamental condition and earnings power of the business to confirm it is a good company temporarily out of market favor, not one in long-term trouble.

A "Decent Value" screen uses this reasoning by selecting for stocks that rank well on valuation (implying they are low-priced) while also holding fair-to-good ranks in financial condition, earnings power, and expansion. This multi-measure method helps find possible prospects where a low price could be a irregularity instead of an accurate judgment of a failing company. One stock that recently appeared from this type of screen is Yelp Inc (NYSE:YELP), the local business review and advertising platform.

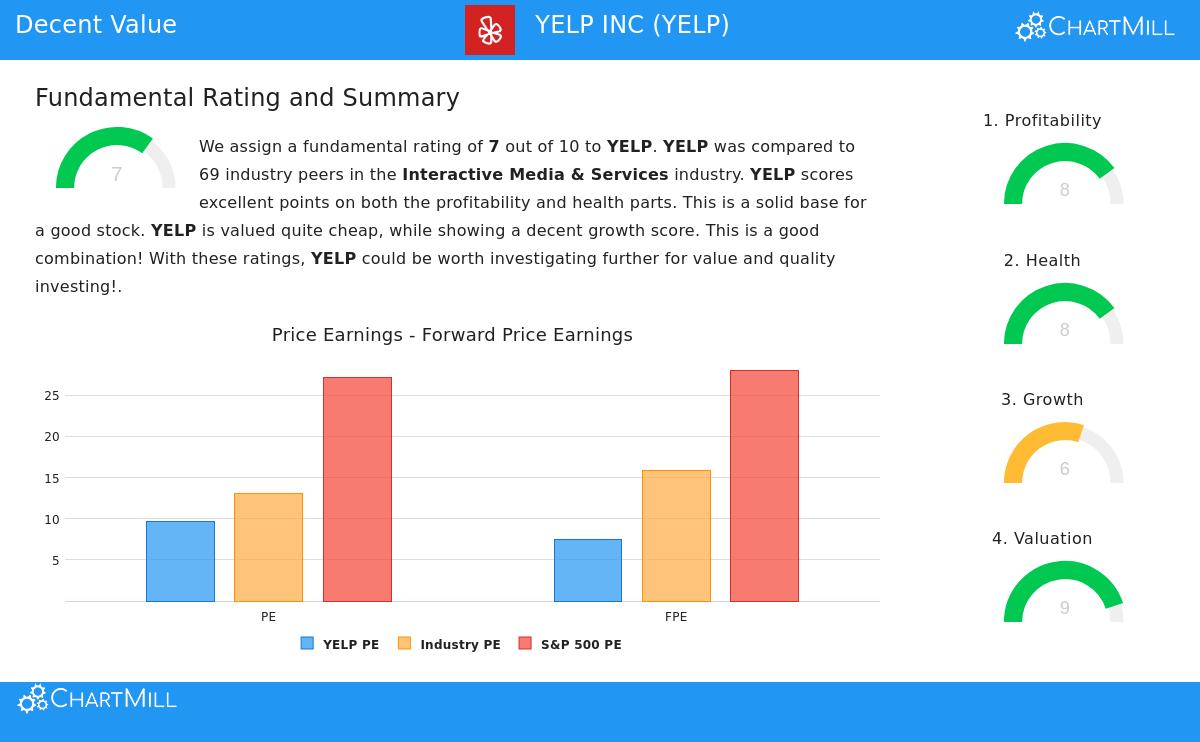

Valuation: The Foundation of the Idea

The main attraction of Yelp from a value viewpoint is its strong valuation measures, which create the foundation of the screening rules. According to ChartMill's fundamental analysis, Yelp receives a top-level Valuation Rating of 9 out of 10. The figures supporting this rank show a stock priced at a notable markdown compared to both its industry and the wider market.

- Price-to-Earnings (P/E) Ratio: At 9.65, Yelp's P/E ratio is much lower than the S&P 500 average of 27.10. In its Interactive Media & Services industry, 74% of firms have a higher price based on this measure.

- Forward P/E Ratio: The pricing seems even more appealing when looking at future profits. With a Forward P/E of 7.46, Yelp costs less than 83% of its industry counterparts and is priced at a steep discount to the S&P 500's forward P/E of 28.06.

- Cash Flow and EBITDA: The value argument is supported by other ratios. Judged by its Price-to-Free Cash Flow ratio, Yelp is priced lower than 96% of the industry. Likewise, its Enterprise Value-to-EBITDA ratio is below 91% of rivals.

For a value investor, these measures are the first sign of a possible find. A low P/E ratio can mean the market is too negative about a company's prospects, possibly creating a margin of safety, a cushion between the price paid and the investor's calculation of inherent value.

Financial Condition: A Solid Base

An inexpensive stock is only a sound investment if the company is financially stable. This is where the idea of avoiding value traps is key. A company with weak financial condition might be low-priced because it is facing debt or cash problems. Yelp's fundamental report indicates no such worries, giving it a good Health Rating of 8.

- Zero Debt: Yelp functions with no interest-bearing debt on its balance sheet. This provides it with notable financial adaptability and eliminates bankruptcy risk from the investment consideration.

- Strong Cash Position: The company's Current Ratio and Quick Ratio are both a solid 2.99, showing more than sufficient short-term assets to meet its liabilities. This cash position beats over 76% of its industry counterparts.

- Altman-Z Score: A score of 4.00 indicates a very low short-term chance of financial trouble, putting Yelp in the top group of its industry for financial strength.

This clean balance sheet is essential for the value argument. It means the company's low pricing is not due to financial danger. Instead, it can direct its resources on operations and shareholder benefits without the burden of debt payments.

Earnings Power: Good Business at a Low Price

Value investing is not about purchasing bad businesses; it is about purchasing good businesses at an attractive price. Yelp shows it is a highly profitable company, receiving a Profitability Rating of 8. Its capacity to produce returns on capital is a main sign of business quality.

- High Returns: The company's Return on Assets (15.16%), Return on Equity (20.46%), and Return on Invested Capital (17.49%) all place in the top 15% of its industry. This indicates management is very efficient at using capital to create profits.

- Improving Margins: Both Yelp's Profit Margin (10.23%) and Operating Margin (13.35%) have increased well in recent years and are above industry averages. Its Gross Margin of over 90% is very high, a trait of software platforms with low physical assets.

These measures are important because they verify Yelp is not a failing company. Its core advertising platform is profitable and effective. The value investor's theory is that the market is mispricing this profitable, cash-producing business.

Expansion: The Driver for Price Change

While pure value stocks sometimes have little expansion, a mix of value and expansion can be effective. Yelp's Growth Rating of 6 shows a varied but hopeful situation, supplying a possible reason for the stock to be revalued upward.

- Strong Profit Expansion: The company's Earnings Per Share (EPS) increased over 20% in the last year and has accumulated at a notable average rate of 65.46% over the past several years.

- Good Past Sales: While recent quarterly sales expansion has been low, the company's long-term sales expansion rate stays good at nearly 11% per year.

- Future Projections: Analysts project good forward EPS expansion of about 29% each year. While sales expansion projections are more moderate, the expected profit increase is meaningful.

For the value investor, this expansion picture is significant. It suggests the company is not static. If Yelp can continue to grow profits while keeping its high earnings power, the market may in time acknowledge its value, leading to a rise of its currently low valuation ratios.

Summary and Additional Study

Based on a methodical "Decent Value" screen, Yelp Inc presents a strong case for investors using a value-focused model. It trades at a steep discount to the market and its peers, has a very strong, debt-free balance sheet, functions with high earnings power and high returns on capital, and is still producing meaningful profit expansion. This mix speaks to the central ideas of value investing: looking for a margin of safety through price while making sure the fundamental business is of good quality and not a value trap.

Naturally, no screen replaces complete individual study. Investors should think about competitive forces in the local advertising field, customer concentration, and the company's ability to maintain its margin structure.

Interested in locating other stocks that match this systematic value method? You can execute the "Decent Value" screen yourself to see the current outcomes here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented on Yelp Inc (YELP) is based on data provided and should not be the sole basis for an investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.