For investors aiming to assemble a portfolio of lasting, high-performing businesses, the quality investing approach provides a structured method. This process centers on finding companies with durable competitive strengths, sound financial condition, and a clear record of producing steady, high-returns on capital. The "Caviar Cruise" stock screen puts this thinking into practice by selecting for firms with a track record of solid revenue and profit increase, high profitability measures, strong cash flow production, and a prudent balance sheet. The aim is not to locate temporary discounts, but to discover companies deserving of long-term holding.

Watts Water Technologies Inc (NYSE:WTS) surfaces as a result from this strict screening process. The North Andover-based maker of water safety, conservation, and flow control products shows a number of features that match the central principles of quality investing.

A Base of Increase and Improving Profitability

A key part of the quality screen is a shown history of increase. The screen asks for a minimum 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. It also requires that EBIT increase exceeds revenue increase, a signal of gaining operational efficiency and possible pricing ability.

- Revenue Increase (5Y CAGR): 7.27%

- EBIT Increase (5Y CAGR): 19.57%

Watts Water easily meets the basic requirements. Its mid-single-digit revenue increase shows steady business growth. The notable number is the EBIT increase, which is almost three times the revenue increase rate. This shows the company has effectively turned higher sales into even larger profits, probably through scale benefits, expense control, or a positive product mix, signs of a well-managed business with competitive edges.

High Returns and Financial Strength

For quality investors, profitability is not only about earnings, it is about the effectiveness of capital use. The screen requires a high Return on Invested Capital (ROIC), specifically measured on core operating assets (leaving out cash and intangibles). A high ROIC indicates a company's capacity to produce sizable profits from its operational investments, building shareholder value.

- ROIC (Excl. Cash, Goodwill & Intangibles): 44.25%

Watts Water’s ROICexgc of over 44% is outstanding. This means that for every dollar put into the core business, the company creates a large return, putting it with the leading performers. This measure is important to the quality view, as companies that regularly earn high returns on capital often have lasting competitive advantages.

Financial condition is also very important. The screen uses the Debt-to-Free Cash Flow (FCF) ratio to evaluate balance sheet risk, favoring companies that could in theory pay off all debt in five years or less using their present cash flow.

- Debt / Free Cash Flow: 0.55

With a ratio of 0.55, Watts Water’s financial standing is solid. This means the company’s yearly free cash flow is almost double its total debt, showing very low financial risk and great ability to finance growth, pay dividends, or buy back shares without stressing its balance sheet.

Trustworthy Earnings

The screen also judges the reliability of reported profits by looking at the conversion of net income into free cash flow. A "Profit Quality" ratio above 75% over five years is needed, making sure earnings are supported by actual cash and are not only accounting results.

- Profit Quality (5Y Avg.): 98.91%

Watts Water’s almost perfect 98.9% average shows excellent earnings quality. Nearly all of its net income over the past five years has been turned into free cash flow. This gives high certainty in the durability of its profits and shows capable working capital management.

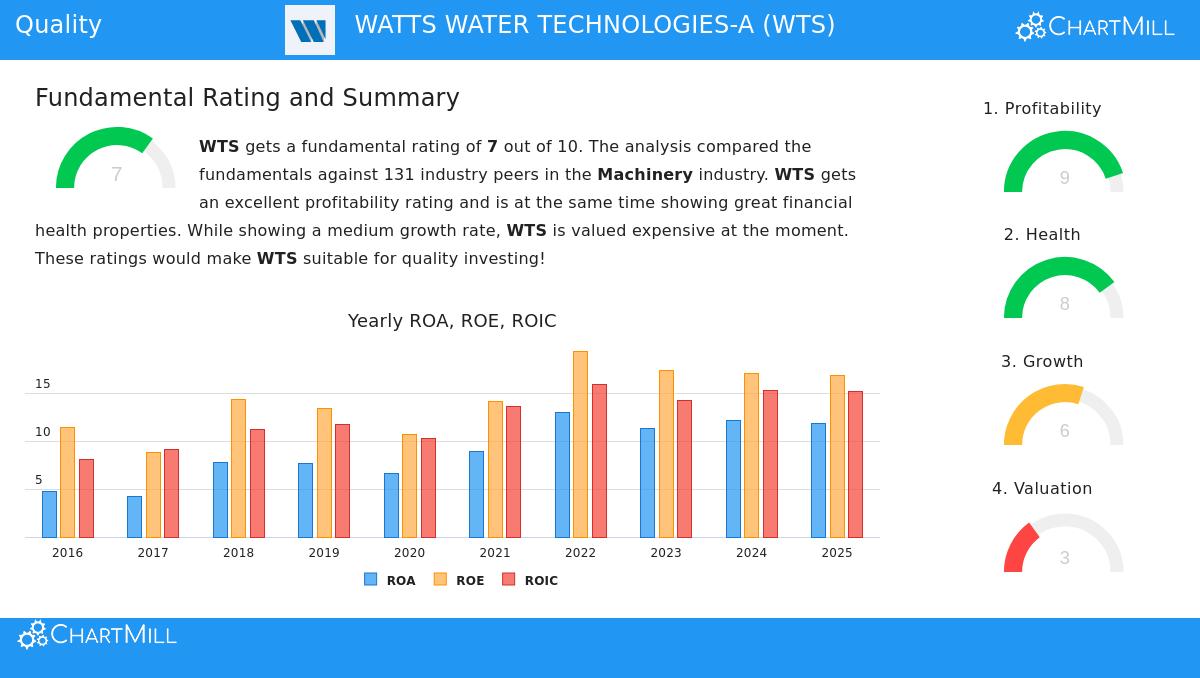

Fundamental Analysis Summary

A review of Watts Water's detailed fundamental report supports the screening results. The company receives high marks for Profitability (9/10) and Financial Health (8/10), with leading industry positions for measures like Gross Margin (~49.5%), Operating Margin (~19.4%), and Return on Assets. Its solvency is excellent, as shown by a very high Altman-Z score.

The main point of care is in Valuation (3/10), where the stock seems costly on traditional Price-to-Earnings measures. This is a typical aspect of high-quality companies and highlights the quality investor's challenge: superior businesses seldom trade at large discounts. The Growth (6/10) rating is good, indicating strong past performance, although analysts expect a slowing in future increase rates.

Is WTS a Quality Investment Candidate?

According to the numerical filters of the Caviar Cruise screen, Watts Water Technologies displays a strong profile for quality investors. It shows:

- Steady Increase: Consistent revenue growth paired with quickly improving profits.

- Outstanding Capital Effectiveness: A very high return on invested capital.

- Strong Financials: Very little debt compared to its ample cash flow.

- Reliable Earnings: Nearly complete conversion of profits into cash.

These characteristics point to a business with operational skill and a firm market place in the necessary water infrastructure and conservation industry. While its present valuation may cause value-focused investors to hesitate, the quality investing method focuses on business excellence over price by itself, acknowledging that lasting strengths often come at a higher cost.

For investors wanting to examine other companies that meet similar strict quality filters, you can see the present Caviar Cruise screen results here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.