For investors looking to build a portfolio of durable, well-run companies able to provide steady returns over time, the principles of quality investing offer a useful framework. This method centers on finding businesses with lasting competitive strengths, sound financials, and a clear history of producing high returns on capital. The "Caviar Cruise" stock screen, based on this method, uses a set of strict quantitative filters to find such companies. It focuses on past revenue and profit growth, high returns on invested capital, reasonable debt, and earnings quality shown by solid free cash flow conversion. A company that passes this screen is not only doing well; it is showing the basic traits that let it build value for shareholders through different economic periods.

One prominent company that results from this strict screening process is WALMART INC (NASDAQ:WMT). The large retailer's place on the list calls for a detailed look at how its financial picture fits with the central ideas of quality investing.

Matching the Main Financial Standards

The Caviar Cruise screen establishes high standards across a number of key financial measures, and Walmart's present numbers display a good fit with these goals.

- Return on Invested Capital (ROIC): A key part of quality investing, ROIC calculates how well a company produces profits from its capital. The screen asks for a ROIC (leaving out cash, goodwill, and intangibles) over 15%. Walmart's ROICexgc of 15.41% meets this mark, showing it earns a solid return on the capital actually used in its main operations. This implies management is good at using resources for profitable growth.

- Debt Management: Careful use of debt is important for long-term strength. The screen uses the Debt-to-Free Cash Flow ratio, with a number under 5 seen as good. Walmart's ratio of 3.48 means that, using its present yearly free cash flow, it could pay off all its debt in less than three and a half years. This shows a firm balance sheet and a good ability to manage its financial duties.

- Profit Quality: This measure contrasts free cash flow with net income, showing how much accounting profit becomes real, usable cash. A five-year average over 75% is needed. Walmart does very well here with a number of 110.16%, meaning it has in the past created more free cash flow than its reported net income. This high-grade earnings profile gives the company great financial room for dividends, share repurchases, debt paydown, or new investment.

- Growth Steadiness: Quality companies should show stable expansion. The screen searches for a 5-year compound annual growth rate (CAGR) in EBIT (earnings before interest and taxes) above 5%. Walmart's EBIT growth of 6.45% meets this standard, displaying a steady rise in its core operating profits over the medium term.

A Broad Look at Walmart's Basic Profile

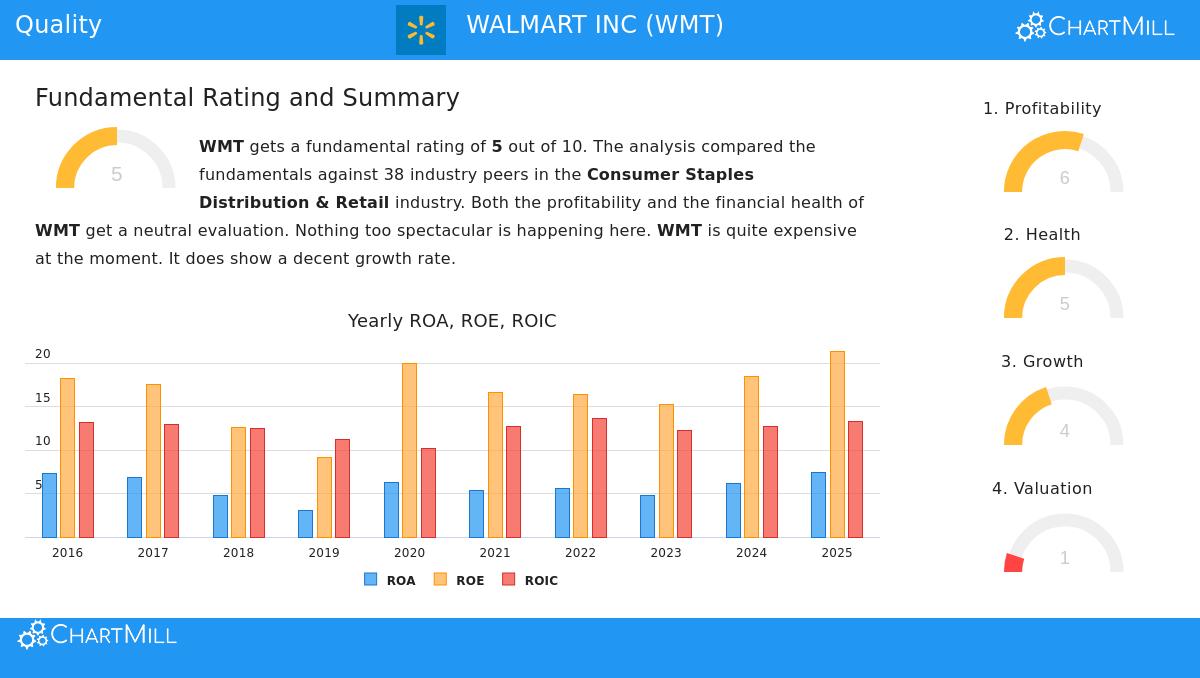

An examination of Walmart's wider fundamental analysis report gives background for the screen's findings. The company gets an overall fundamental rating of 5 out of 10, putting it in the middle range compared to others in the Consumer Staples Distribution & Retail industry.

- Profitability and Health: Walmart gets fairly good scores in profitability (6/10) and financial health (5/10). Its positive points include a strong return on equity (23.84%) and a very safe Altman-Z score, pointing to low bankruptcy risk. The main weakness noted is in liquidity, with low current and quick ratios. However, for a company of Walmart's huge size, predictable cash flows, and top access to capital markets, this is often viewed as a controlled operational efficiency more than a major solvency risk.

- Valuation Consideration: The most clear warning in the report is on valuation, which scores a 1 out of 10. With a Price-to-Earnings ratio above 52, Walmart is priced at a large premium to both its industry average and the wider S&P 500. This high multiple shows the market's view of Walmart as a stable, defensive holding, particularly in unsure economic climates.

- Growth Path: The growth rating is neutral at 4 out of 10. The company displays steady, single-digit growth in both revenue and earnings per share in the past, and analysts expect this modest but consistent growth to keep going forward.

You can review the complete, itemized summary of these measures in Walmart's fundamental analysis report.

What This Means for Quality Investors

For an investor using a quality-focused, long-term strategy, Walmart's screening results are meaningful. The high ROIC and outstanding profit quality point to a business with a strong operational model and pricing ability that turns profits into actual cash. The firm debt-to-FCF ratio shows financial durability and the ability to fund its projects or give capital back to shareholders without taking on too much debt. While the price is high, quality investors often state that excellent businesses with wide economic advantages, like Walmart's unmatched distribution network, brand name, and large scale, can merit and support premium prices over a very long time. The company's reliable, predictable growth in revenue and EBIT fits with the quality investing choice for dependability over fast, but possibly unstable, expansion.

Finding Other Quality Investment Options

Walmart's success with the Caviar Cruise filters points to its status as a company with many quality traits. Investors curious about finding other companies that match these strict financial standards can run the screen on their own. You can find the full Caviar Cruise screen and its present results here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The data shown is from sources thought to be dependable, but its correctness is not guaranteed. Investors should do their own complete research and think about their personal financial situation and risk tolerance before making any investment choices.