Vertex Pharmaceuticals Inc (NASDAQ:VRTX) presents an interesting case study for value investors looking for companies trading below their intrinsic worth. The selection process uses a disciplined method that favors stocks with good valuation numbers while keeping acceptable scores across other basic dimensions. This plan finds companies where the market price may not completely show the quality of the underlying business, possibly creating chances for investors who think prices will eventually align with basic business value.

Valuation Assessment

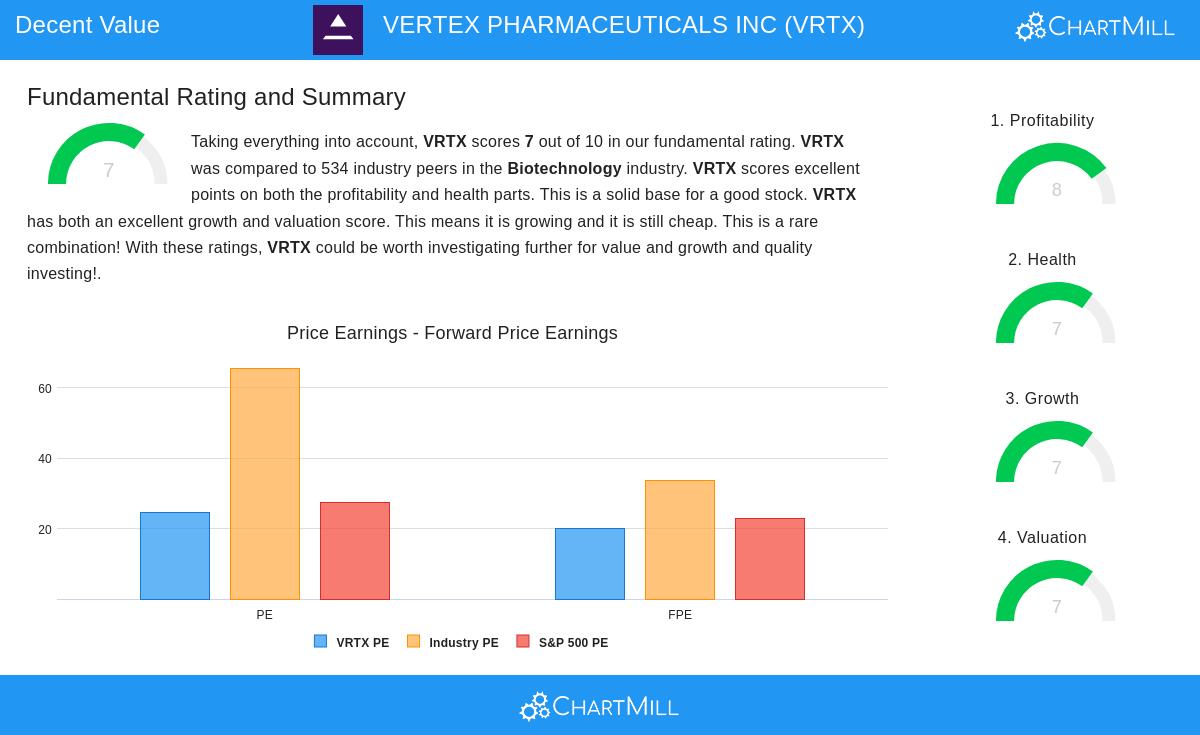

The valuation numbers for Vertex Pharmaceuticals show several interesting points that fit with value investing ideas:

- The company's Price/Earnings ratio of 24.61 seems high by itself but looks better when measured against industry peers, with 94.57% of biotechnology companies trading at higher multiples

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios both point to relative undervaluation, ranking better than 93% of industry competitors

- The PEG ratio, which changes P/E for growth forecasts, indicates the stock may be fairly priced considering its growth path

- Forward P/E of 20.05 sits a little under the S&P 500 average while doing better than 93% of industry counterparts

These valuation features are important for value investors because they show possible differences between market pricing and basic value. The method focuses on finding companies where several valuation methods regularly indicate undervaluation compared to both the wider market and industry peers.

Financial Health and Stability

Vertex shows solid financial health with several notable strengths:

- The company works with no outstanding debt, removing interest expense worries and offering financial room to maneuver

- Good liquidity ratios show enough ability to meet short-term responsibilities, with current and quick ratios of 2.52 and 2.16 respectively

- Steady share count decrease over one and five-year periods points to careful capital allocation

- Return on invested capital is much higher than the cost of capital, confirming value creation for shareholders

For value investors, financial health offers the safety buffer Benjamin Graham highlighted. Companies with good balance sheets can survive economic declines and industry problems while still putting money into future growth, lowering the chance of permanent capital loss.

Profitability Metrics

The company's profitability picture shows outstanding operational efficiency:

- Profit margin of 31.86% ranks in the top 4% of the biotechnology industry

- Operating margin of 38.77% is higher than 98% of industry competitors

- Return on equity of 21.18% and return on assets of 15.13% both place in the top 5% of the sector

- Gross margin of 86.11% points to good pricing power and cost management

High profitability is key for value investors because it indicates lasting competitive benefits and the ability to create cash flows that support basic value estimates. Companies with better margins often have business advantages that protect them from competition.

Growth Trajectory

Vertex displays a mixed but mostly positive growth picture:

- Revenue growth of 10.46% over the past year joins with a notable 21.50% average yearly growth over recent years

- Remarkable EPS growth of 7,966.67% in the past year shows margin improvement and operational effects

- Future EPS growth estimates of 150.50% each year indicate strong analyst belief

- Revenue growth forecasts of 9.58% each year suggest continued expansion

Growth thoughts add to traditional value investing by helping investors steer clear of value traps. Companies with good growth outlooks are more likely to see their basic business value rise over time, offering double returns from both valuation multiple improvement and basic business growth.

Investment Considerations

The mix of fair valuation, outstanding profitability, debt-free balance sheet, and good growth prospects makes Vertex Pharmaceuticals an interesting option for value-focused investors. The company's focus on creating treatments for serious diseases, especially in cystic fibrosis and other specialty areas, gives some view into future revenue streams. However, investors should think about the built-in risks in biotechnology, including pipeline problems, regulatory tests, and competitive forces that could affect future performance.

For investors wanting to find similar chances, our Decent Value Stocks screen regularly finds companies meeting these basic criteria. More basic analysis details for Vertex Pharmaceuticals are available in the detailed fundamental report.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results.